Chapter 12

Project Cost Management

12.1 Introduction

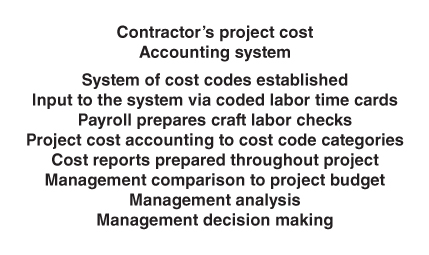

Monitoring and controlling project costs are critically important management functions on all construction projects. After construction begins, the contractor's project cost management system retrieves project costs, in accord with a system developed by the construction contracting firm for the purpose, including labor and equipment hours and production quantities, from the job site as the work progresses. This information is used in two important ways. One is to develop labor and equipment production and cost data to be stored in the company's historical information database in a form suitable for use in estimating the cost of future work.

The other application of cost and production information is to assist in keeping the construction costs of an ongoing project within the established project budget. In order that the contractor can accomplish the project objective of completing the project at or under the project budget, costs which are incurred on the project are monitored in a structured way as the project is constructed, and are compared to budgeted amounts on a regular and continuing basis. Management carefully monitors these comparisons, so that if certain activities or elements of cost exceed project budget amounts, or if they appear to be trending toward exceeding the project budget, management can take action in an effort to accomplish the objective of completing all project activities within the budget. The central elements of a contractor's project cost accounting, cost reporting, and cost control system are depicted in Figure 12.1.

Figure 12.1 Central Elements of a Project Cost Accounting, Reporting, and Control System

Regardless of the type of contract between the owner and the contractor, or the project delivery method in use, it is important that the contractor exercise the maximum control possible over field costs throughout the construction period on every project he constructs. A functional and reliable cost accounting and cost control system plays a vital role in the proper management of a construction project, as well as in the profitable operation of a construction company.

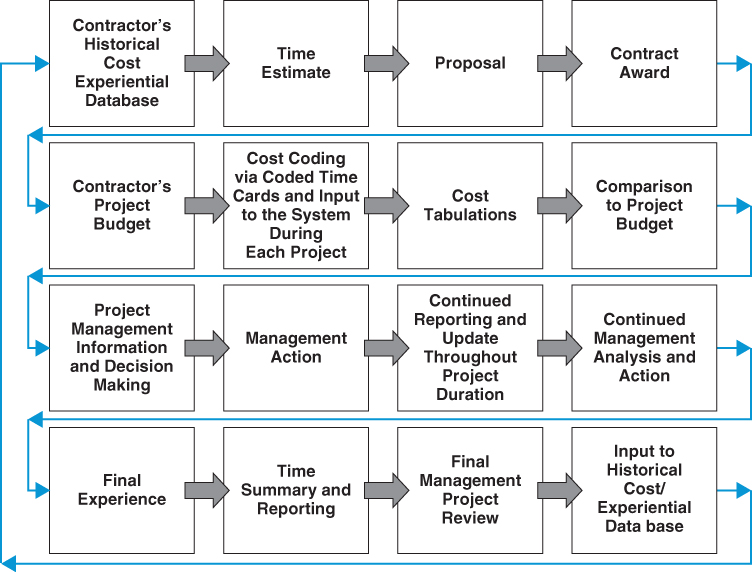

The details regarding the structure and functioning of a cost control system will vary somewhat from one contractor to another, and will vary with project size and complexity. In any event, the justification for the expense of maintaining and operating a project cost system is the value of the management information it provides. If the information produced is not accurate and timely, or if this information is not utilized to fullest advantage by management, then the system has no real value, and its cost cannot be justified. Properly designed, implemented, and utilized however, a project cost management system is an investment in the success of projects and in the success of the company. Figure 12.2 illustrates the cyclic nature of the administration of the contractor's cost accounting, cost reporting and cost control system for use in managing construction projects, and the feedback of this information into the contractor's historical cost information database for use in estimating future projects.

Figure 12.2 Cycle of Project Cost Reporting, Cost Accounting, and Cost Control System

This chapter discusses the methods employed in project cost reporting and cost control and the estimating feedback process. Although the details with regard to how these actions are actually accomplished will vary somewhat from one construction firm to another, the systematic process described here can be regarded as being typical and representative of present practice within the construction industry.

12.2 Project Cost Control

Project cost control is an information system structured by a construction company, which is designed to assist the project manager and other managers within the company, in controlling construction costs. It is a monitoring process that provides feedback concerning project expenses and how they compare to the established project budget.

Project cost control actually begins with the preparation of the original cost estimate for a project. For each project to be constructed, the contractor prepares a detailed estimate of construction costs that serves as the basis of the contractor's proposal in a competitive bid project, or as a target estimate if the contract is negotiated. When the contractor's proposal is accepted by the owner, a contract is formed for the amount of the proposal. After the contract is formed, a project budget is created, using the activities and costs as determined in the estimate. This project budget serves as the basis, and as the metric, for the cost control process throughout the construction of the project.

The cost control system identifies project costs as they are incurred and, in a structured manner, charges these expenses against the project work elements and activities to which they apply. The costs as they actually occur are continuously compared with the budget. Keeping within the budget and knowing when and where job expenses are exceeding the budget, or are trending toward exceeding the budget, and having this information available dependably and in timely fashion so that management can take appropriate action, are key components of profitable operation for a construction company.

The field costs on every project are obtained in considerable detail because this is the way projects are originally estimated, and also because cost overruns or potential overruns in the field can be corrected only if the exact causes can be determined. To learn that construction costs have exceeded the budget is not helpful if it is impossible to identify where the cause of the overruns is occurring, or if this information is not available in time for management to take corrective action.

Summary project cost reports are prepared at regular time intervals throughout the duration of a project. These reports are designed to provide information for the project manager in such a way as to make it possible for the project manager to determine the overall cost status of the project and also to identify those specific work activities or classifications where project costs are exceeding the budget. Management attention can be quickly focused on those activities in the project that are in need of attention.

Timely information is required on a regular basis while the work on the project is underway if effective action against cost overruns is to be taken. Determining that costs exceeded the budget only after the completion of the work on a project leaves the contractor with no possibility of taking corrective action. Therefore, cost reports are prepared, analysis performed, and actions taken on a regular recurring basis, usually weekly, throughout the duration of the construction project.

12.3 Data for Estimating

As noted in Chapter 5, when the cost of a project is being estimated, many elements of cost must be evaluated by the estimator. Labor and equipment expenses, in particular, are subject to so many variables, and are such an important component of the cost of a project, that they are best priced in light of the contractor's past experience. In essence, historical labor and equipment costs and production records are the only reliable source of information available for estimating these two critically important components of project cost. The historical cost database the company develops and maintains provides a reliable and systematic method for accumulating labor and equipment productivity and costs for use in estimating future projects. The information in this historical information database comes from coded cost reports prepared during the course of every project the company constructs.

Production rates, units of output per unit of input, are fundamental to the estimation of labor and equipment costs. Costs per unit of production, or “unit costs,” are widely used for estimating labor and equipment expense because of the convenience of their application. These unit costs are determined from production rates and the hourly costs of labor and equipment, as determined from the coded cost reports which have been produced on projects which the construction company performs. Unit costs can be kept up-to-date by the contractor's periodically adjusting them so as to reflect changes in hourly rates and production efficiencies. The information compiled for company estimating purposes can therefore be expressed in terms of labor and equipment production rates, or unit costs, or both. The feedback system, as illustrated in Figure 12.2 must be designed to produce information in whatever form or forms are compatible with company needs and procedures, both for cost control and for use as historical data.

12.4 Accounting Codes

It is customary that an identifying code designation be assigned to each individual account in a contractor's accounting system. The coding systems used by contractors are not standardized, but rather are structured by individual construction firms as those business entities see fit to suit their particular purposes. Standard account systems have been developed by organizations such as the Associated General Contractors of America (AGC), the Associated Builders and Contractors (ABC), the National Association of Homebuilders (NAHB), the American Road and Transportation Builders Association (ARTBA), and the Construction Specifications Institute (CSI), for use by contractors.

While a number of standard systems of accounts are in existence, contractors typically use their own individual coding systems, which they have developed and have tailored to suit their particular operations. Alphabetic, decimal, and mixed alpha-numeric cost codes are used by contractors. The code used in this text is a decimal code system, and may be considered to be representative of typical construction cost accounting practice. One advantage of a decimal system is that it is expandable so as to accommodate any level of detail that may be desired.

Appendix O contains an abbreviated list of typical ledger accounts in common use by contractors. The asset accounts as included in the general ledger are identified by whole numbers from 10 through 39; general ledger liability accounts are designated by 40 through 49; net worth by 50 through 69; income accounts by 70 through 79; and expense accounts by 80 through 99.

Subaccounts are assigned a distinctive decimal number, with the first number identifying the general ledger or control account under which the subaccount exists. For example, consider the account 14.5.35. The whole number 14 indicates a property, plant and equipment account. The first decimal number, 0.5, indicates that it is associated with tractors. The last two numbers, 0.35, identify the account as a depreciation account.

In Appendix O, project expense is designated by account number 80.000. This is where every item of expense chargeable to a particular construction project is recorded. This major category of project expense is often subdivided into two major subdivisions: project work accounts and project overhead accounts. Each of these major subdivisions, in turn, has an extensive internal breakdown into detailed items of cost.

An abridged list of typical cost accounts for each of these categories is illustrated in Figure 12.3. The project cost breakdown shown is not intended to be complete or to apply to all categories of construction. The cost accounts shown in Figure 12.3 would best apply to building construction. Once they have been established by the contractor, the cost code numbers for a given cost account typically remain the same, although they are typically updated in minor fashion to accommodate new technology, or new construction materials or processes, or new accounting methods. These cost code numbers are used consistently throughout the company, and do not vary from one project to another.

Figure 12.3 Master List of Project Cost Accounts

As noted earlier, the cost accounting and cost coding systems that are utilized by most contractors have some degree of flexibility built in, so as to accommodate new cost codes which the contractor may wish to track, as well as to accommodate changes in technology. For example, a general contracting firm may have included in the fairly recent past, a cost account code for placement and finishing of glass fiber reinforced (GFR) concrete, and an electrical firm may have incorporated codes in the recent past, for installation and terminations in fiber optic conductors.

12.5 Job Cost Accounts

The point of origin for construction project cost management is a set of cost codes in the company financial accounting system, as described in the previous section. However, a basic accounting principle for construction contractors is that project costs are recorded on a periodic recurring basis for each individual construction project. Cost accounting based in these cost codes must, of necessity, be a function of each construction project, and profit or loss is evaluated for every project at the individual job level.

Summary project cost data tabulated in the usual company ledger accounting records have only very limited value for use in managing project costs during the course of the construction of a project. Although the normal company accounting system periodically reports project costs associated with labor, materials, subcontracts, job overhead, and equipment, these are summary cost data, for a number of projects the company has performed. Details concerning the exact composition of these costs, such as the expenses associated with basic work activities such as excavation, concrete, or carpentry, are not available from these summaries. In addition, this information consists of a cost tabulation only, and includes no data concerning work quantities installed. As a result, project managers cannot determine from these summaries, where costs are or were within budget, or over budget, on any project.

What is required for project cost management on each individual project is more detail concerning the composition of project costs and the work quantities accomplished. This requires the collection of additional data not provided by the company's basic financial accounting system.

The cost breakdown required for cost control and project management is achieved by maintaining a detailed set of separate cost records for each project. A separate account is established for each cost item that pertains to a given construction project. These accounts are subsidiary to the company's general ledger accounts.

In practice, each job expense is posted to the appropriate project cost account. Expenditures such as those for labor, materials, equipment, subcontracts, and project overhead are charged to the appropriate project cost accounts throughout the life of the project, and these accounts are named and numbered, as discussed previously. Accounts that are active and relevant to the project under consideration are chosen from the chart of cost accounts as discussed earlier, or the company may maintain a set of project cost accounts and cost codes which it uses for all of its projects.

The details of the job cost accounts may vary from one project to another, depending upon the type of project being constructed. The project may be divided into only a few cost accounts, or into a larger number of line items, depending upon the size of the project and the type of work involved. Because the cost system for each project is directed toward making comparisons between actual and budgeted costs, cost accounts utilized for a project will parallel the work breakdown which was used for estimating that project. Typically, the cost accounts utilized for the project cost system are identical with those that were used in the preparation of the original cost estimate. Or, said differently, the estimator produces his estimate of project costs on a project that is being bid, by the same activity set and code numbers that are in the historical cost data file. These activity names and numerical codes will, in turn, be used to prepare the project budget after the contract is formed, as well as to tabulate the costs of the work as construction on the project is performed.

It is important to note that when cost code accounts and cost code numbers are structured for the elements of cost the contractor has decided he wishes to monitor and control on the project, a couple of practical considerations must be kept in mind. First, the activity and work item descriptions and their cost code numbers must be sufficiently detailed to provide the project management team with sufficient detailed information to be able to discern cost trends, and analyze them, and to make effective decisions based on the information. Additionally, however, it must be remembered that the project superintendent or foremen on the project will be charged with the responsibility of “coding” labor and equipment hours and costs in the field using these activity names and numbers. If the activities and cost accounts are overly detailed or complex, the all-important information that is input to the system from the field will not be accurate.

12.6 Monthly Cost Reports

After the work on a project begins, and throughout the life of the project, information contained in the job cost accounts is periodically summarized and reported in a series of cost reports. These reports are prepared regularly on a periodic basis, and are designed to inform project management in sufficient detail and in a timely manner with regard to the cost status of the work overall, as well as the status of individual activities on the project. The information conveyed and the frequency of reporting are structured to meet the specific needs of job management. It is very important that each cost report be designed to convey its particular message in the most succinct and usable form possible. Weekly cost reports are the norm in most companies, and for most projects.

While the formats used by contractors in preparing their periodic cost reports vary somewhat, the basic information to be tabulated is consistently the same: for each activity, the budgeted cost, costs or expenditures to date, percentage complete, and variance from budget are tabulated. Sometimes additional information is provided, such as “cost to complete,” or “estimated final cost,” values that are calculated based on the current trend.

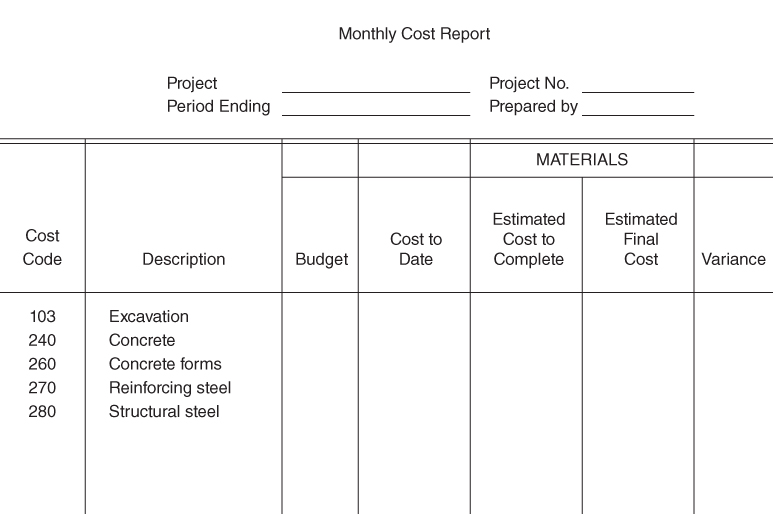

Figure 12.4 presents an example of a typical materials cost summary for a project and depicts the typical format utilized in cost reports. The report illustrated is a monthly materials cost report, such as might be used on a large engineered project. Typically, contractors prepare more detailed weekly cost reports, and these reports usually tabulate costs for labor, equipment, subcontractors, and for the total project. These will be discussed and illustrated in subsequent sections of this chapter.

Figure 12.4 Monthly Materials Cost Report

Construction company management will make a determination with regard to which items or categories of cost will be tabulated and monitored for the projects the company performs. A company that performs large engineered projects may well tabulate costs and reports for all five of the categories of project cost noted above (materials, labor, equipment, subcontractors, and total project). A company that performs building construction work may choose to monitor only labor costs during the course of the project because these costs represent a large fraction of the total cost of the project and are the most variable and present the greatest risk for the contractor.

For each of the four cost types represented by Figure 12.4, budget values (Column 3) are taken directly from the original job cost estimate, or they may be taken from the project budget document which the contractor has prepared for the project. The project budget, which is prepared by most contractors for each project they perform, is based on the original estimate for the project.

The job cost accounts in Figure 12.4 show the tabulation of materials costs to date (column 4) for each of the materials (column 2, description) and their cost code (column 1) whose cost the contractor has chosen to monitor. The estimated cost to complete (column 5) is based on the project budget, taking into account the costs incurred to date and the percentage complete at this date, and making a calculated linear projection of the projected cost to complete. The estimated final cost (column 6) is obtained as the sum of columns 4 and 5. The variance (column 7) is column 3 subtracted from column 6. Thus, the variance is the difference between the anticipated actual cost and the budget at this point in time. A convention must be established in the project cost accounting and reporting system as to whether a positive or a negative variance indicates a cost overrun. In this summary, a positive value for variance is the amount of the anticipated cost overrun.

Most project managers and company management people who review the periodic cost reports will direct their attention first to the “variance” column, and will be especially attentive to cost items for which a positive variance appears (where the project budget is being exceeded). Managers must then make a decision as to what best to do with regard to the items or activities indicating a positive variance. Sometimes it may be best to “stay the course” for another reporting period, so as to monitor trending. At other times, immediate management action may be indicated, in the form of changing the work plan, and/or crew mix, and/or the equipment being used, and so on. Experience has shown that it is good management practice for the project manager to discuss positive variances with the project superintendent or craft foreman, inasmuch as they are the management people closest to where the work is being performed, and often will have the best explanation as to the reasons for, and the meaning and impact of the variance.

The algebraic sum of the total variance values is the amount by which it now appears the actual total project cost will exceed or be less than the budgeted amount. For activities or materials relating to work that has not yet started, estimates of cost to complete will normally be taken as the budgeted amounts. For completed items of work, the actual final cost is used for the estimated final cost, or some contractors may add an additional column to the cost report, indicating “actual completed cost.”

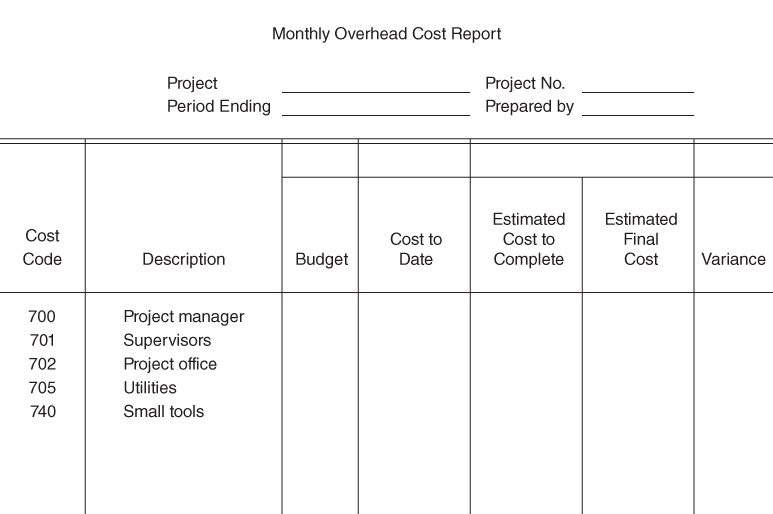

12.7 Project Overhead

The periodic project cost reports which are prepared for materials, labor, and subcontractor costs typically do not include a reporting of project overhead, because such expense is general in nature and usually cannot be associated with specific work items or activities. For this reason, project overhead, also referred to as project indirect cost, is normally reported separately. Figure 12.5 shows a typical form that might be used for monthly reporting of project overhead expense. Values for the various items in Figure 12.5 are obtained in much the same fashion as for the other monthly or weekly cost reports, except that the costs reported here pertain to job overhead cost accounts rather than to specific activities or work classifications on the project.

Figure 12.5 Monthly Overhead Cost Report

12.8 Labor and Equipment Costs

Project costs associated with materials, subcontracts, and project overhead generally are reasonably stable, and therefore are relatively easy to predict during the estimating process. In management terms, the risk of variance between estimated costs and the actual costs that will be experienced on a project is, much of the time, relatively low for these costs. Barring estimating oversight or mistake, these costs can be determined with reasonable accuracy when the project is estimated, and, except in the case of unusual circumstances, such costs typically do not vary a great deal from their budgeted amounts.

For this reason, costs of this type are maintained as project expenses but are not usually subjected to detailed cost reporting and analysis during the course of the construction of a project. The cost information available from the monthly project cost reporting is normally sufficiently detailed and timely for purposes of project cost management for these categories of cost.

Labor costs and equipment costs, however, are subject to a great deal of uncertainty. These two categories of project cost can vary substantially during the construction process, and further, they can vary as the result of a number of factors, many of which are unpredictable at the time of preparing the estimate. Moreover, these two categories of cost constitute a major fraction of the cost of performing a typical construction project. It is one of the ironies of both estimating and cost management, that the two categories of cost that comprise the greatest fraction of the cost of a project are also the most difficult to estimate and control. The inherent variability, and the uncertainty, coupled with the significance of the labor and equipment costs for a project, and therefore the risk associated with these categories of costs, explains the fact that contractors' cost management systems usually concentrate on these two items of job cost.

The monthly cost reports for materials and overhead, as we have discussed them, are certainly useful for project management; however, these reports do not provide the information needed for monitoring labor and equipment costs in suitable detail or in sufficient time to be useful for project management. Accordingly, labor and equipment costs are customarily tabulated and reported at a different level of analysis and reporting. The process of determining, at regular short intervals, how much work is being put into place in relation to the costs being incurred for the labor and equipment being supplied to the project, is described in the following sections.

12.9 Cost Accounting

In order to accumulate, report, and analyze labor and equipment cost and production information from an ongoing construction project, a contractor will establish a special system with a detailed set of cost accounts. The maintaining of these detailed project records is referred to, in the aggregate, as project cost accounting. This process of project cost accounting for labor and equipment is not independent of the contractor's job cost accounts as previously discussed, but rather, it is a more detailed cost accounting system which exists and functions within the framework of the contractor's overall company ledger accounts. Project cost accounting for labor and equipment involves the continuous determination of labor and equipment costs, together with determination of the work quantities produced, followed by the analysis of these data, and the presentation of the results in summary form for the information and action of project management.

Thus, it can be seen that project cost accounting for labor and equipment differs from the usual accounting practice inasmuch as the information that is gathered, recorded, and analyzed is not merely in terms of dollars and cents. This category of construction cost accounting is necessarily concerned not only with the costs themselves, but also with labor hours, equipment hours, and the amounts of production, or work accomplished. The systematic and regular checking of costs and production is a necessary component of obtaining reliable, time-average production, and cost information for the project. These labor and equipment costs are usually summarized and reported weekly, on a regular basis throughout the life of the project. This is the only way to generate sufficient information timely for management analysis and decision making, and to gather the information in sufficient detail to feed back into the historical information database for use in estimating future projects.

Additionally, this project cost accounting must strike a workable balance between too little and too much detail. A too-general system will not produce the detailed cost information necessary for meaningful management control and future estimating information. Excessive detail will result in the objectives of the cost system being obliterated by masses of data and paperwork, as well as needlessly increasing the time lag in making the information available. It should also be noted that an excess of detail in the cost control system, and an excess of numerical values and descriptions of cost categories which are to be reported from the field, will overwhelm the superintendents and craft labor foremen who gather and report this information. This, in turn, often results in inaccurate and incomplete reporting, which defeats the purpose of the system. The company cost system must be tailored to suit the contractor's own particular mode of operation. The detail used in this book is reasonably typical of actual practice in the construction industry.

A project cost accounting system is a summary and analysis tool for field supervision as well as for project management. In the final analysis, the best cost control system a contractor can have is skilled, trained, experienced, energetic, and effective field supervision. It is important that field supervisors realize that the project cost accounting system is intended to assist them by the early detection of troublesome areas. Superintendents and craft labor foremen are vitally important members of the project management team, and they are the people who perform the “labor and equipment cost coding” that provides the primary input to the project cost accounting system. Without the complete understanding, and support, and cooperation of these key individuals, the cost accounting system cannot and will not be effective.

In a contractor's integrated system of cost accounting, cost control, and historical information gathering, as illustrated in Figure 12.2 and as shown again in Figure 12.6 below, it is necessary that the project cost account codes be broken down into the same elementary work classifications or activities, and that they be identified by the same cost code numbers, as were used in preparing the estimate for the project. As discussed in Chapter 5, the estimator identifies each work item or activity by its code of account designation when he or she sets down the results of the quantity takeoff and when craft labor is estimated. Throughout the construction process, a continuous record is kept, of the actual costs of production for these same work items. Thus, it can be seen that from the time of preparing the estimate to the time of the completion of the project, the same work breakdown and cost code numbers apply in the contractor's integrated system. For clarity, the flow chart depicting this process is illustrated in Figure 12.6.

Figure 12.6 Cycle of Project Cost Accounting, Cost Reporting, and Cost Control System

12.10 Labor and Equipment Budget

For purposes of project cost accounting, a labor and equipment budget, which is often referred to as the project budget, is prepared by the contractor following the award of the contract, and prior to the beginning of field operations for the project. Each activity on the project is listed, along with its cost code, and the dollars or hours from the estimate are indicated. The budget information on this document may be expressed for each activity on the project in the form of dollars of cost, or labor man-hours, or crew hours, or equipment hours, or unit costs, or production rates. And frequently, all of this information is included in the budget.

As the work on the project is performed, costs will be coded in the field by the superintendent or labor foreman, and then will be summarized and reported on a periodic basis, and then will be compared to this project budget. Progress to date on each activity will also be determined, for each cost reporting period. This process will provide information for the project management team with regard to dollars expended to date for each activity, along with progress on the activity to date. This project budget then will serve as the metric, literally the budget, to which the actual costs incurred in the field are compared, throughout the progress of the work on the project.

For the discussions in this chapter, the convention to be used will be for the budget to be prepared in terms of the total estimated work quantity, the unit cost of labor and/or equipment, and the total labor and/or equipment cost for each work cost code on the project to date. As was noted previously, different units may be used (unit cost, production rate, labor man-hours, crew hours, etc.) in the project budget. At some point in the analysis the metric becomes dollars, and therefore dollars are used in the discussion in this chapter to illustrate the process.

When labor costs are tabulated, management will have made a decision with regard to whether the labor cost indicated should be direct labor costs only or whether the summary should also include indirect labor cost (see Chapter 5). Contractors vary in their opinions in this regard; however, most contractors prefer that labor cost as reported in the cost reports from the field include only direct labor. What is most important in this regard, is that the budget and field costs be expressed on exactly the same basis and, that foremen, superintendents, and project managers, as well as company office personnel, are mindful of the convention being used.

In this way, valid comparisons can be made throughout the life of the project, between the estimated costs and the actual costs of construction. In this text, the project cost budget and the labor cost reports are expressed in terms of direct labor costs only, without the inclusion of indirect labor cost.

12.11 Cost Accounting Reports

Summary labor and equipment cost reports must be compiled frequently enough during the course of the construction of a project, so that those activities or items of work where costs incurred are exceeding the project budget can be detected early enough, so that management has time to analyze the situation and to determine whether corrective action should be taken, and to make timely decisions regarding what form the corrective action should take. Cost reporting intervals are a function of project size, the nature of the work, the type of construction contract being utilized, and the style and preference of company management. Obviously, there must be a balance struck between the cost in dollars and time of generating such reports, and the value of the management information that is generated.

Daily cost reports may sometimes be prepared on very complex projects involving multiple shifts, or on a shutdown project, where the contractor and/or owner require accurate cost reports on an immediate basis. It is not the usual project, however, that can profit from such frequent cost reporting. Some very large projects that involve relatively uncomplicated work classifications may find intervals of a month, or perhaps a two-week reporting interval, to be satisfactory. It is generally agreed that for most construction companies and for most projects, weekly labor and equipment cost reports are best. Weekly labor and equipment cost reports are the basis for the discussion in this text.

The cutoff time for inputting to the system can be completion of work on any desired day of the week. It is commonplace practice for contractors to match their cost reporting system cutoff times to their usual payroll period cutoff day and time. In turn, the cutoff time for the contractor's schedule updates is also typically set to coincide with this same time.

In the sections that follow, we will first examine the procedures involved with project labor cost accounting and reporting. Following this will be a discussion of cost accounting and reporting methods for the equipment on a project.

12.12 Labor Time Cards

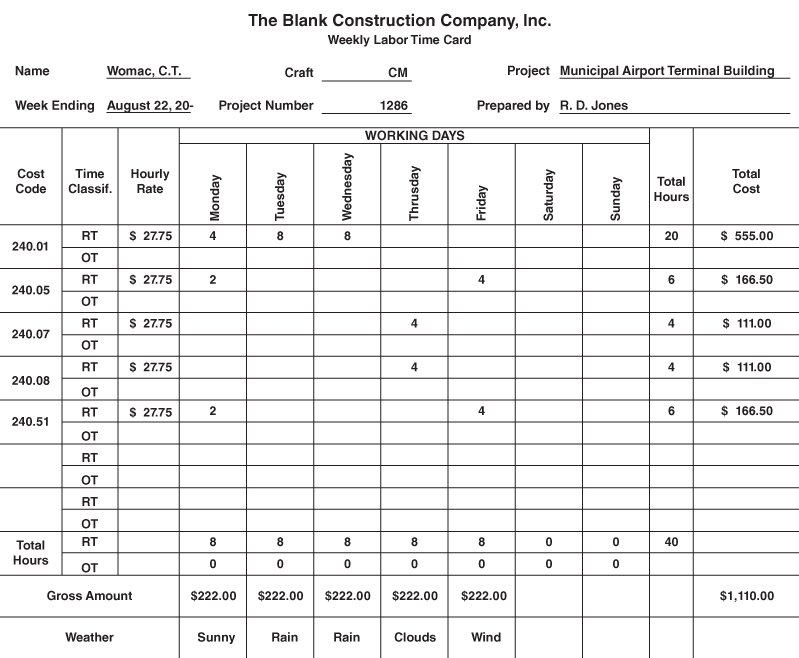

Time cards that are prepared in the field by labor craft foremen or superintendents are the source document for both payroll purposes and for the input to the project labor cost accounting system. Time cards are used to report the hours of labor time for each worker, as well as the work categories to which each worker's labor hours applied. These work categories or activities have identifying names and numbers, as we have discussed, and the activity numbers are recorded on the time card along with the number of labor hours spent working on that activity on each work day, by each person. This process is referred to as coding labor. Figure 12.7 shows a typical daily labor time card, and Figure 12.8, a typical weekly labor time card. Which of the two is used depends on the preference and policy of company management.

Figure 12.7 Daily Labor Time Card

Figure 12.8 Weekly Labor Time Card

Most managers agree that daily time card preparation is best, so that labor hours can be coded to the correct activities and cost codes on an immediate basis, while the recollections of the craft labor foreman or superintendent are still fresh. This ensures the most accurate tabulation of the labor hours to the correct activities or work categories.

While time card formats vary from one company to another, certain elements of content are typical. The head of each card usually provides for entry of the project name and number, date, weather conditions (for daily time cards), and the name of the person preparing the card. The body of the time card provides for the name, badge number or other identifying number for the worker, and oftentimes the name or identifying number of the craft of the worker. Each worker's labor hours are reported for each day as regular time (RT) or overtime (OT), as the case may be. Along with the labor hours listed, spaces are provided on the time card for the inclusion of the appropriate cost code for each of those hours of work. In this fashion, each craft worker's hours are “coded” for all of his or her hours of work each day throughout the life of the project.

Absolute perfection in time coding and distribution is not possible, nor expected. Nevertheless, the need for care and the best possible accuracy in labor coding cannot be overemphasized. Superintendents and craft foremen should be trained in this regard and should constantly bear in mind during their preparation of time cards that the accuracy of each person's payroll, as well as the accuracy of cost reporting for the current project, and also the accuracy of the estimates for future projects, are all dependent on the accuracy of his or her completion of the time cards.

Figure 12.7 depicts a typical daily time card, representative of what might be in use in a construction company, for a crew of cement masons (CM), a cement mason foreman (CF), and a group of construction laborers (L). Illustrated in the figure are the features described above. It should also be noted that in Figure 12.7, some of the hours for the concrete foreman, Mr. Jones, are coded to account number 701.03, which is an overhead account, and that other hours are coded to accounts 240.05 and 240.08, which are cement mason work activity accounts. This is illustrative of the practice sometimes employed, where a foreman's time spent on supervisory duties is charged to an overhead account, while time spent working with his tools is charged to the appropriate work cost codes. Other contractors may prefer an accounting convention wherein all field supervision time is charged to project overhead.

If weekly time cards are used, a separate card for each individual worker is prepared to record the hours worked during the week. Although the arrangement of the weekly time card is different from that of the daily time card, the card presents the same information concerning each individual worker. As was discussed in a previous section, the hourly rates shown on the time cards in Figures 12.7 and 12.8 are direct labor wage rates only and do not include any indirect labor costs, such as payroll taxes, insurance, or fringe benefits. When a weekly time card is used in the contractor's system, it is preferable that the craft labor hours and cost codes information, as discussed in the next session, be entered on a daily basis. Recording the craft labor hours and the cost codes to which the hours should properly be assigned as the work progresses, will eliminate the temptation for the foreman of letting the matter go until the end of the week and then trying to enter the information from memory.

It should also be noted that increasingly, contractors are utilizing electronic time cards. Where the contractor is using computer-based payroll and cost accounting procedures, the computer can preprint all standard information on the time cards or on a daily time sheet. The person making the time report need add only the hours and cost codes. This information may be reported on a paper form, or very commonly today, may be input in the field via laptop, or PDA, or tablet computer, to a spreadsheet, or to a specialized software utilized by the contractor, and then uploaded to the accounting system.

12.13 Time Card Preparation

Labor cost coding, that is, the distribution of each worker's time to the proper cost accounts, normally is done by the craft labor foreman or by the superintendent because he or she is in the best position to know how each worker's time was actually spent during the course of each workday. Sometimes this information is first recorded in the foreman's pocket time book, with the nature of the work performed by the individuals of his crew often described by words rather than by cost code numbers. This information is then compiled from the pocket time form to the time card at the end of the workday. As noted earlier, this process is often performed electronically by use of PDAs or laptop computers in many companies today.

The foreman identifies the craft and position of each worker by using any of a variety of simple letter or numerical codes the contractor may have developed for this purpose. For example, in Figure 12.7, CF indicates cement mason foreman, CM means cement mason, and L indicates laborer. Sometimes, the foreman will also enter the hourly rate for each worker because it is not unusual for an individual during a week, or even during a single day, to be employed on work which is compensated at different rates of pay.

As has been discussed, the numerical codes for different activities or work categories are taken by the foreman from the contractor's master cost coding system. Ideally, this system will have a balance between generating sufficient detail for proper description of activities, and thus providing management the ability to analyze and make effective decisions, while not becoming so detailed and complicated that its use is cumbersome or unduly burdensome for the craft labor foreman.

The importance of accurate and honest reporting of craft labor hours to their proper activities and numerical cost codes simply cannot be overemphasized. On the basis of the allocation of labor (and equipment) time and costs to the various work activity account numbers, cost and production information is generated. This information is used as the basis for management decision making during the course of the performance of the project and also is stored as historical performance information in the contractor's historical cost database, where it is used in estimating future projects. If this information reported from the field is inaccurate or distorted, it may lead to ineffective decision making as the project is being constructed, and also will provide inaccurate and misleading information when it is used for estimating and cost control purposes on future projects.

Especially in cases where project costs experienced are exceeding the project budget amounts, the supervisor must avoid the temptation to code hours of labor for those activities that are over budget to other work categories where costs are under the project budget amount. Loss items must be identified as such, without any attempt at covering them up by charging time to other cost accounts. Additionally, when reporting from the field is honest and accurate, where activities are completed for significantly less than the project budget amount, management can certainly use this information to advantage for estimating and managing future projects as well.

It should also be noted that project managers and company management can play an important role in assuring proper reporting from the field. Supervisors should be trained for the management work they are performing. This training should include emphasis on the critical importance of accurate and honest cost coding and reporting, and project managers should continue to reinforce this principle throughout the course of every project. It can be noted that one reason the supervisor is experiencing costs that exceed the budget on this project, despite his or her best efforts, may be that costs were improperly reported on a previous project or projects, leading to an inaccurate estimate for this project. When one understands the cyclical nature of the cost accounting and cost reporting system, and the use of this information for estimating future projects, it becomes clear that the entire process can be poisoned by poor cost coding and reporting from the field.

In some companies or on some projects, the time card may be completed by someone other than the craft labor foreman, such as a field superintendent, project engineer, or project manager. A project engineer, for example, can collect the foremen's time books at some convenient time each day and complete the individual time cards, adding the necessary information for payroll and cost accounting, such as employee number, and work cost codes, and hourly rates for different cost code items, and so on.

12.14 Measurement of Work Quantities

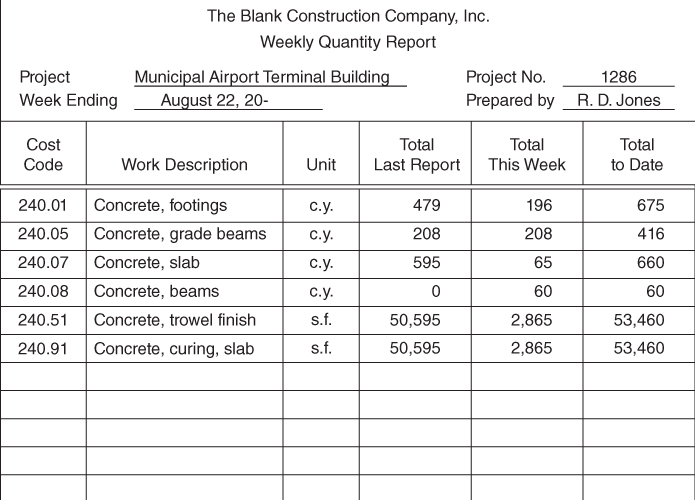

For the determination of labor production rates or unit costs and their reporting to the cost report and historical information, it is necessary to obtain not only the hours and costs involved, but also the amount of each activity or work classification that has been accomplished during the reporting period. On some types of work, it may be feasible for the foreman to include with his daily time cards the work quantities accomplished for that day. It is more common practice, however, for work measurements to be made at the end of each weekly payroll period, and this method is the basis for discussion here.

The items of work measured must be identical to the standard cost code work classifications. Although labor costs are now being discussed, the weekly measurement of work quantities includes all work items performed, whether accomplished by labor, equipment, or a combination of both. Consequently, the same weekly work quantity determination can serve for both labor and equipment cost accounting.

Determinations of work quantities can be obtained in a variety of ways depending on the nature of the work and company management methods. Direct field measurement on the job, estimation of percentages completed, computation from the drawings or from the building information model, and obtaining of quantities from the estimating sheets are included in the list of methods that are commonly used.

Direct measurement in the field is a commonplace method for determining work quantities performed. The measurement may be performed in terms of total units or quantity achieved to date, or units accomplished during the week being reported. This procedure is easily applied to projects that involve relatively few cost code classifications. Many heavy, highway, and utility contracts are of this type.

There are often instances in which quantities can be obtained with reasonable accuracy by applying estimated percentages of completion to the work amount totals. Although not as accurate as direct measurement of actual quantities, this procedure can yield useful information, so long as accurate determinations are occasionally made by actual measurement, such as for monthly pay requests by the contractor. Total work quantities of all types should also be checked against the estimating sheets on occasion, as a check on the overall accuracy of quantity reporting.

The field measurement of work quantities on projects that involve a large number of cost code classifications can become a substantial and burdensome task. Most building and industrial projects entail substantial numbers of different cost classifications. One convenient procedure in such cases is to mark off and dimension the work advancement in colored pencil on a set of project drawings that are reserved for that purpose. The extent of work put into place can be indicated at the end of each workday or each week as desired. By using different colors and by dating successive stages of progress, work quantities can be determined from the drawings or estimating sheets as of any date desired.

If the company is using a building information model for estimating, and/or for project scheduling, and/or for cost accounting and control, and/or for schedules of values and payments, the electronic model and the related softwares can facilitate the electronic determination of quantities of work installed. As these models become even more sophisticated and still more capable, it is easy to foresee that the use of the building information model, or other electronic estimating software, may well become the method of choice for determining and tabulating work quantities installed.

The field measurement of work quantities can be, and often is today, performed by the field supervisors. However, on large projects, and especially those with numerous work codes, it may be desirable that the project engineer or project manager carry out this function because of the time and effort required. Weekly reports of quantities of work performed are submitted on standard forms such as that illustrated in Figure 12.9.

Figure 12.9 Weekly Quantity Report

12.15 Forms of Labor Reports

Weekly labor cost reports can be prepared on the basis of either man-hours of labor or labor cost, along with the amount of work produced. That is, labor production can be monitored in terms of either labor-hours per unit of work (production rates) or cost per unit of work (unit prices). Which of these is used is a function of project size, the type of work involved, and company management procedures.

Where labor hours are used as the basis for labor cost reporting and cost control, the project budget is prepared in such a way as to include labor hours per unit of work. In this regard, total labor hours are frequently used, with no attempt to subdivide labor time by craft or trade specialty. For example, the project budget may indicate so many hours of carpenter time and so many hours of ironworker time. Total labor hour project budgets of this type are usually based upon an “average” crew mix for each work category. Alternately, labor hour project budgets can be prepared by using craft-specific hours.

When labor hours are used as the basis for monitoring, during the performance of the work on the project, actual labor hours and work quantities are obtained and reported from the field. This makes possible a direct comparison of actual to budgeted production. Such an approach, of course, reflects labor productivity, but not labor cost. However, this system is simple to implement, and also avoids many of the problems associated with labor cost analysis, such as projects that require long periods of time to complete. On such projects, wage rates may be increased several times during the life of the project, rendering measurement of labor cost against the project budget a cumbersome task.

When the project cost for a very large and very long-term project is first being estimated, educated guesses are made by the estimator with regard to the potential wage rate increases during the life of the project. What this means is that labor costs on long-term projects are often estimated without exact knowledge of the wage rates that will actually apply during the entire construction process. As a result, actual labor wage rates during the work period may turn out to be different from those rates that were used in preparing the original project cost control budget. Thus, labor costs produced by the project cost system are not directly comparable to the budget. To make valid cost comparisons, it is necessary to either adjust these labor costs to a common wage-rate basis, or to form the project budget in terms of labor hours rather than labor cost.

Labor hour project budgets also are convenient and effective as a management tool for the craft foreman or superintendent in those companies that make it their practice to share project budget information with field supervisors. Many supervisors find it easy to understand how many labor hours or crew-hours have been allocated in the project budget, and then to monitor man-hours or crew-hours as they are expended during the performance of the work, so as to make their own assessment of current status relative to the project budget.

While labor hours project budgets can serve as a very effective basis for labor cost reporting and control, many companies prefer to monitor dollars of labor cost instead. These companies simply adjust their labor cost accounting when changes in craft labor rates occur. In fact, for most construction applications, labor cost analysis is more widely applied than is labor hour analysis. For this reason, the labor cost reports discussed in this chapter are based on costs.

12.16 Weekly Labor Cost Reports

In a company that utilizes labor dollar reporting as the basis for project budgeting and for cost reporting, cost analysis, and cost control, labor costs are typically tabulated once per week. In a typical construction company, on the day of the week that has been designated as the reporting cutoff date, labor hours, and labor cost codes as they were entered on the time cards are summarized, and are then tabulated with the summary of work quantities produced during the same week. The results of this analysis are summarized and reported in a weekly labor cost report. While the organization and exact content of these cost reports will vary somewhat from one company to another, the basic information which these cost reports convey is almost always the same. Two different forms of labor cost reports are illustrated in Figures 12.10 and 12.11.

Figure 12.10 Weekly Labor Cost Report Number 1

Figure 12.11 Weekly Labor Cost Report Number 2

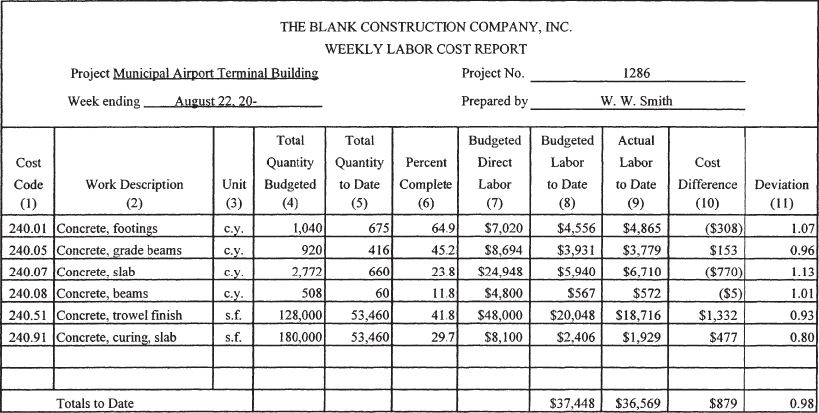

These labor cost reports classify and summarize all labor costs incurred on the project, through the effective date of the report. The labor costs in both of these reports are reported as direct labor costs only, and do not include indirect labor costs. These reports have the objective of providing project supervisors, the project management team, and company management with detailed information concerning the current status of labor costs, and how these costs compare with those that were estimated and brought forward to the project budget. All labor cost reports, including the two labor cost report forms shown here, are intended primarily to identify those work classifications where costs are exceeding the project budget amounts and to indicate the extent of the overruns. These reports will also indicate, and the project management team should take note, where significant labor savings are occurring. This, too, is valuable information for the project management team, as well as for estimating purposes.

Figure 12.10 is a weekly cost report for concrete placement that summarizes labor costs as budgeted, for the week being reported, and a total of labor costs for this activity to date. Not all cost report forms include costs for the week being reported, but most do. These values can be of significance in indicating downward or upward trends in labor costs. The labor report form in this figure indicates work quantities, as well as labor costs for each activity or work category. Unit prices, obtained by dividing the total labor cost in each work category by the respective total quantity, enable direct comparisons to be made between the actual costs and the costs as budgeted. In Figure 12.10, the budgeted total quantity, budgeted total labor cost, and budgeted unit cost for each work type are taken directly from the project budget. The other quantities and labor costs are actual values, either for the week reported, or to date.

When the total quantity of a given activity or work item has been completed, its to-date and projected saving or loss figures are obtained merely by subtracting its actual total labor cost from its estimated total cost. When a work item has been only partially accomplished, the to-date saving or loss of that work item is obtained by multiplying the quantity in place to date by the underrun or overrun of the unit price. The projected saving or loss for each work type can be obtained in different ways. In Figure 12.10, it is determined by assuming that the unit cost to date will continue in linear fashion to the completion of that activity. Multiplying the total estimated quantity by the underrun or overrun of the unit price to date yields the projected saving or loss figure.

The projected saving and loss figures shown in Figure 12.10 afford a quick and informative summary of actual labor cost as compared to project budget labor cost on the project. The activities where labor overruns are occurring are identified, and the financial consequences if nothing changes are also indicated. Some labor cost reports also indicate the trend for each cost code, that is, whether the unit cost involved has been increasing or decreasing. This information can be helpful in assessing whether a given cost overrun is improving or worsening, and can be of assistance in evaluating the effectiveness of cost reduction or cost control efforts which have been undertaken to date.

Figure 12.11 is an alternative form of weekly labor cost report that presents the same weekly cost information for concrete placement as Figure 12.10 in somewhat different form. This figure shows actual and budgeted total labor costs to date for each cost classification. The budgeted total quantities and total labor cost for each cost code are brought forward from the project budget. The actual work quantities and labor costs to date are cumulative totals for each work classification, as obtained from the time cards and weekly quantity reports. Column 10 of Figure 12.11 shows the cost difference as column 8 minus column 9, with a positive difference indicating that the cost in the project budget exceeds the actual cost to date. Hence, in column 10, a positive number is desirable; a negative number, undesirable. The deviation is the actual cost to date (column 9) divided by the budgeted cost to date (column 8). A deviation of less than one indicates that labor costs are within the budget, whereas a deviation of more than one indicates a cost overrun.

Although column 10 in Figure 12.11 does indicate the magnitude of the labor cost variation for each cost code, it does not indicate the relative seriousness of the cost overruns. The deviation is of value in this regard because it shows the relative magnitude of labor cost variance.

It should also be noted that many labor cost reports of the kind illustrated in Figure 12.11 may also include additional columns to provide more information to management. For example, many contractors include a column that indicates “Projected Cost to Complete.” This mathematical determination shows for each work classification item, the impact of the cost overrun or underrun experienced to date, on the final cost of the completion of that item, if no action is taken. This calculation assumes a linear projection, with the work assumed to continue at the current rate. This column provides an indication of the potential total savings or total additional cost of each work item.

For those work types not yet completed, the cost differences listed in column 10 in Figure 12.11 do not always check exactly with the to-date savings and loss values of Figure 12.10. These small variations are caused by the rounding off of numbers, and are not significant.

12.17 Equipment Cost

Project cost and production accounting for equipment is important, especially on engineered construction projects where the cost of equipment frequently constitutes a significant proportion of the total project cost. On projects of this kind, the need to monitor, analyze, and control equipment costs parallels the need for the cost reporting and control of labor costs on building construction projects. The costs associated with large pieces of construction equipment are substantial and are also inherently variable, are variable with a number of different factors, and are a significant element of risk for the contractor, and are therefore deserving of a comprehensive record keeping and cost accounting and cost control system.

The objectives of equipment cost accounting are the same as those that have been discussed for labor costs. Management at all levels requires timely information for effective project cost control, and estimators need accurate data from the field for use in future estimates. It should be noted that usually only the major capital equipment items merit detailed cost study, however. Lesser equipment such as power saws, concrete vibrators, and hand-operated soil compactors are normally charged to a project on a flat rate or lump sum basis and do not require detailed cost analysis.

While labor wage rates may frequently be fixed by or related to local labor agreements, no such determination exists for equipment costs. Therefore, the contractor must establish his own equipment expense rates and the methods of their determination.

In the case of rental or leased equipment, the rental or lease rates are known or easily discernible, but the contractor must still establish the operating costs during the time he is using the equipment. In the case of contractor-owned equipment, both ownership and operating costs must be determined. As discussed in Chapter 5, ownership expenses include depreciation and investment costs. Investment expense includes the costs of interest, insurance, taxes, and storage. Operating costs are on-the-job expenses that accrue when the equipment is in use, such as fuel, oil, grease, filters, hydraulic fluids, scheduled maintenance, tire or track replacement, tire or track repairs, mechanical repairs and parts, and possibly, operating labor. As noted in another section, some contractors prefer to regard the labor associated with equipment operation as a labor expense rather than as a component of equipment cost. Others include the labor cost as a part of equipment operating cost. There are a number of cost accounting advantages in treating equipment operating labor as any other labor cost, and not accounting for it as a component of equipment operating cost. This is the basis for the discussions in this text.

When contractors are preparing estimates for new work, they must obtain the most accurate values possible for the ownership and operating costs of the various equipment units that will be required for the construction of the project. The discussion in Chapter 5, and Figure 5.6 illustrates a procedure that is widely used for estimating such costs. For convenience, this figure is reproduced as Figure 12.12. The contractor's determination of his cost per hour for the ownership and operation of equipment is often referred to as the internal rate for the company, for that piece of equipment.

Figure 12.12 Estimate of Equipment Ownership and Operating Cost

For most items of production equipment, ownership, lease, or rental expense is combined with operating costs into a total cost per operating hour. When the project is under construction, it is the purpose of the project cost accounting system to determine the number of hours that each piece of equipment or equipment type is in operation on the job, and the project work accounts to which these hours apply. With the use of the hourly equipment rates as previously established for estimating purposes, equipment costs can be determined and reported periodically for each activity or work type. When these costs are compared with work quantities produced, equipment unit costs of production are obtained. Thus, once the hourly equipment rates are determined, equipment cost accounting proceeds in very much the same fashion as labor cost accounting, and similar kinds of cost reports are produced. Figures 12.13 and 12.14 depict tabulations of equipment costs and production during the course of a project.

Figure 12.13 Daily Equipment Time Card

Figure 12.14 Weekly Equipment Cost Report

As a general rule, equipment expense is directly chargeable to a single project work account as illustrated above. However, there are certain occasions when this is not true, and equipment costs must be accumulated in a suspense account until such time as they can be distributed to the proper cost accounts. An example might be a central concrete mixing plant consisting of many separate equipment items on a project, which is producing concrete for several different cost accounts for the project. Equipment expenses of this type are typically collected into a suspense account, and then are periodically distributed equitably to the appropriate work item or activity cost accounts on the basis of the quantities involved.

Another special case of equipment, insofar as cost accounting is concerned, is support equipment. Support equipment refers to an equipment item that serves many different operations on the project. Examples include cranes, hoists, air compressors, and electric generators used on a project. The allocation of time of such machines to specific work codes can be very difficult, if not impossible. Therefore, a common approach is to establish special cost codes for such equipment, often in project overhead. All equipment time is charged to its account, with no effort made to distribute the cost of that piece of equipment to the various work accounts involved.

The internal rental rates used to charge equipment time to projects the contractor performs are based on time-average ownership and operating expenses that actually vary over the service life of the equipment. To illustrate, typically investment costs will decrease and repair costs will increase for a piece of equipment as it ages. However, the use of lifetime average costs is the only reasonable way to have each project bear its proper share of the ultimate total expense associated with any particular equipment item. When equipment rental rates are assessed to a job, this is an all-inclusive charge. Correspondingly, the costs of fuel, lubrication, maintenance, repairs, and other such equipment expenses are typically not charged to the job on which they are actually incurred, but to the applicable equipment accounts.

12.18 Equipment Time Cards

Because equipment costs are expressed as a time rate of expense, time reporting is the starting point for equipment cost accounting for a project. Equipment time is kept in much the same way as labor time.

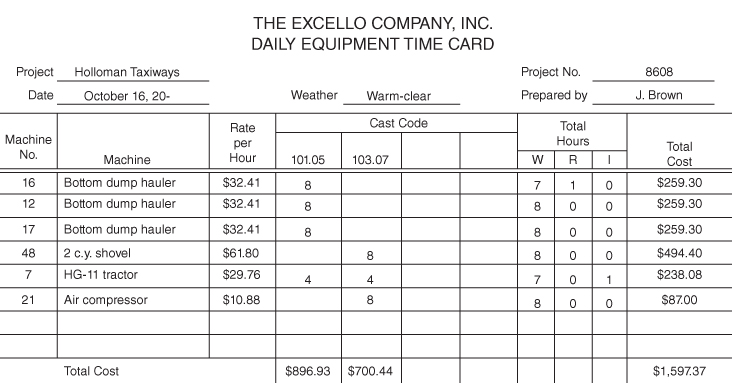

For large construction equipment, a common procedure is to have the equipment supervisor or the project supervisor prepare daily or weekly equipment time cards for each piece of equipment on the job. It should be noted that these equipment time cards are separate from and in addition to the operators' time cards as has been discussed previously. This procedure has merit because, by using different time cards, separate reportings are available for payroll and labor cost accounting purposes, and for equipment cost accounting. In addition, equipment items such as pumps and air compressors may not have full-time operators and could otherwise be overlooked. Figure 12.13 is an example of a typical daily equipment time card.

The equipment time card performs the same project cost accounting function as the labor time card. By allocating equipment times to the proper cost codes for activities or work classifications, it is possible to determine the equipment costs that are chargeable to the various work categories. Accuracy of equipment time allocation to the proper cost codes is just as important as it is for labor. This is the only way accurate and reliable information can be obtained for purposes of cost control on the current project, and for estimating future projects.

As was recommended for labor time card reporting, it is preferable that the time information for equipment be entered on a daily basis, rather than weekly. Just as with labor time, distributing the equipment time on a daily basis is much more conducive to better accuracy.

The supervisor or project superintendent usually prepares the equipment time cards. Sometimes, however, someone else, such as the project engineer or the assistant project manager, may complete the time card, and will enter the budget rates of the individual equipment items reported, and will make the cost extensions.

Additional elements of information may be generated and reflected on the time card for reach piece of equipment. As has been noted previously, company management must decide whether the value of the additional information is justified by the cost and effort of gathering and tabulating the data. Figure 12.13 records equipment time as working time (W), repair time (R), and idle time (I). Excessive equipment idle time may indicate field management problems such as too much equipment on the job, lack of operator skill, improper balance of the equipment spread, or poor field supervision. Appreciable repair time can indicate inadequate equipment maintenance, worn-out equipment, severe working conditions, or operator abuse. Substantial unproductive time can also be caused by job accidents, inclement weather, unanticipated job problems, or unfavorable site conditions.

12.19 Equipment Cost Reports

Once each week, equipment costs are tabulated, along with the corresponding quantities of work produced. Work quantities are derived from the weekly quantity report as discussed in a previous section of this chapter. A weekly equipment cost report is prepared by following the same procedure described in previous sections for labor cost reporting.

An equipment cost report summarizes all equipment costs incurred on the project, through the effective date of the report. Figure 12.14 illustrates a frequently used format for such reports. As can be seen, this figure is very similar to the weekly labor cost report form shown in Figure 12.10. Alternately, management may elect to structure the weekly equipment cost report in a format similar to the weekly labor cost report illustrated in Figure 12.11.

Figure 12.14 serves to inform project management in a quick and concise manner with regard to actual equipment costs being experienced on the project, as compared to the project budget. The figure presents both work quantities produced and equipment cost, and yields actual unit costs for each work category or activity. Cost overruns (“Loss” on the report) and underruns (“Savings” on the report) can be readily identified.

The budgeted total quantity, budgeted total equipment cost, and budgeted unit cost for each work category are taken from the project budget. The other quantities and equipment costs are actual values as reported in the field, either for the week reported, or total to date. The to-date and projected “Saving” and “Loss” values represent the equipment cost experience and projections on the project through the report date of October 18.

12.20 Other Equipment Charges to Projects

The procedure discussed in the preceding sections is the typical method of accounting for equipment costs and for charging equipment costs to activities and work items on construction projects. There are however, some aspects of equipment costs that require special consideration.

For example, some equipment expenses are not included in the usual hourly internal equipment rates. The costs of move-in, erection, rigging, dismantling, and move-out of equipment are fixed costs that cannot be incorporated into time rates of expense. Such costs are normally charged to appropriate project overhead accounts, and are not included in the hourly or monthly equipment rates.

Additionally, for equipment that is charged to a project at an hourly rate, the matter of accounting for idle time and repair time for the equipment becomes a matter of company policy. There are a number of different procedures that may be followed, with the most common approach being to charge the project at the established internal rates for the full working day for each piece of equipment that is on the project. Then, credit is given against this charge, for repair time and for idle time caused by weather and other uncontrollable causes. The cost accounting impact of this procedure is that the project is charged for all equipment which is on the site, whether it is used or not. This policy can materially assist in controlling underusage or hoarding of equipment.

When this process is employed, many companies have established a policy whereby when backup or standby equipment units are purposely kept on a job to handle emergencies, the project is charged only with the ownership cost for that equipment. Additionally, the cost of this backup equipment should be explained in a cost report footnote, so as to indicate the fact that this backup equipment is known and intended to be idle for most or all of its time on the job.

For feedback to the historical cost database and the estimating process, the individual activity or work category cost accounts are charged with net equipment operating hours, plus ordinary or usual idle time. This information may be skewed, however, in the case of backup equipment being kept on a project. The excessive idle time for backup equipment can be charged to a special overhead account, with an explanatory footnote. This will prevent the backup equipment from misrepresenting the actual project equipment usage costs on the project.

12.21 Cost Information and Field Supervisors

Construction supervisors, foremen and superintendents, play a vital role in the management of every project, and certainly this is true for the project cost accounting and control process as well. As has been noted, it is the supervisors who provide labor and equipment cost coding information. The accuracy and honesty with which they perform this function has a profound effect on the proper reporting of project costs. This, in turn, influences management decisions and actions as the construction on the project is performed and has a direct bearing on the project cost information stored in the contractor's historical cost database and used for estimating future projects.

There is some difference of opinion expressed among owners and upper level management of construction companies with regard to whether detailed cost information or project budget information should be shared with field supervisors. The statement is sometimes made, for example, that craft foremen or superintendents may be tempted to charge labor or equipment time incurred on operations showing losses, to other cost codes on which performance has been good. It has also been said that confidential cost information may be compromised or that a superintendent or foreman may tend to relax when he or she knows that his costs are within the estimate.

However, it is well recognized that the only way a cost accounting, reporting, and control system can succeed is with the support and cooperation of the field supervisors. They try to achieve the best possible performance and expect to receive credit and perhaps a bonus or other recognition if they can complete projects at or below the estimated costs. Field costs are very much involved when companies enter into profit-sharing or incentive plans with their supervisors. Decidedly, many modern managers agree that the best management policy is to provide superintendents and craft foremen with all of the project budget information, whether in units of dollars or hours, and then to allow them to conduct their management functions in light of the actual budget information.

12.22 Cost Control

The weekly labor and equipment cost reports make it possible for company management to quickly assess the cost status of the project overall and to identify those work activities where such costs are proving to be excessive. In this way, management attention is quickly focused on those work classifications that need it. If the project expense information is developed promptly, it may be possible to bring cost overruns back within the project budget.

In actual fact, of course, project cost control begins when the project is first estimated and priced, because this is when the values that will appear in the project budget are actually established. This truism reinforces the interrelationship between, and the cyclical nature of project cost accounting and reporting, and the historical cost information database, and the estimating process.

On a typical project, there likely will always be some work classifications whose actual costs will exceed those estimated. The project manager is primarily responsible for getting the total project built for the estimated cost. If some costs go over, the objective becomes to have them counterbalanced by savings in other areas.

Having identified where production costs are excessive during the course of the construction, project management must then decide just what to do about them, if indeed anything can be done. For certain, the hourly rates for labor and equipment are not controllable by management. The only real opportunity for cost control resides in the area of improving production rates. This element of work performance can, to a degree, be favorably influenced by skilled field supervision, astute job management, energetic resource expediting, and the improved makeup of labor crews and selection of equipment.