EXECUTIVE SUMMARY

Those leading through a merger, acquisition, or the like do so to create more value faster. They look for revenues to double or more on the way to returning many times their initial investments. Maybe you're driving or leading the investment. Maybe you're leading the business itself or playing a supporting role. In any case, you need a leadership playbook for the merger or acquisition.

This is that playbook, the one we've used as investors, leaders, and supporters. It gives you the frameworks, tools, and sub-playbooks you need to create that value faster. Our overarching approach is to work through customers, capabilities, and costs—in that order. First, figure out how you're going to win with customers. Then build the leadership, team, and capabilities required for that. Fund those efforts by cutting less valuable efforts and their associated costs.

This is how we've created value faster against a backdrop of others failing to deliver the desired results 83 percent of the time. In a Harvard Business Review article, Kenny Graham noted that “between 70 and 90 percent of acquisitions fail.”1 A KPMG M&A study found that 17 percent of deals added value, whereas 30 percent produced no discernible difference and 53 percent destroyed value.2

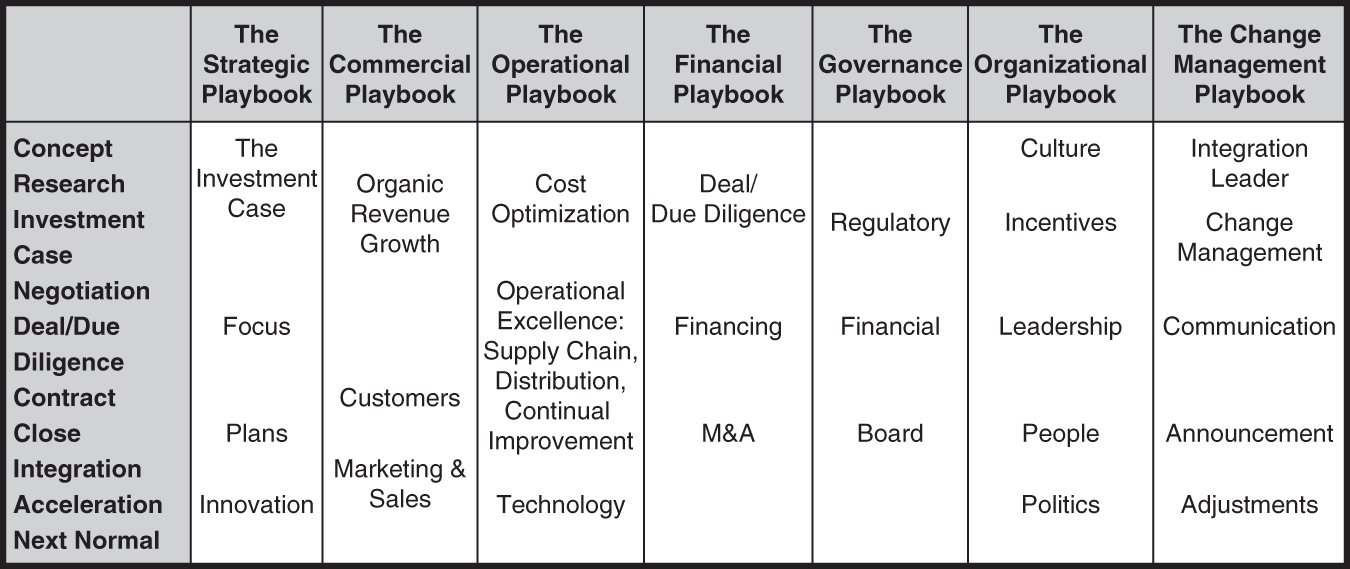

This book lays out the seven sub-playbooks and a prototypical order that comprise the M&A leader's complete playbook. We also include summaries of tools to help along the way, each of which has an editable download available at www.primegenesis.com/tools.

The seven sub-playbooks are:

- The Strategic Playbook

- The Commercial Playbook

- The Operational Playbook

- The Financial Playbook

- The Governance Playbook

- The Organizational Playbook

- The Change Management Playbook

As this is inherently a non-linear process, parts of each of these playbooks need to be deployed at different times in different mergers or acquisitions. With that in mind, adapt this prototypical order for your particular situation.

Concept => Research => Investment Case => Negotiation => Deal/Due Diligence => Contract => Close => Integration => Acceleration => The Next Normal => The Next Chapter

The Strategic Playbook

Be clear on what you want out of an acquisition or merger, how it would fit with what you've already got, and what you're willing to give up to get it. Then broaden your perspective to look at different possibilities before narrowing on the few best candidates and putting together investment cases for them.

Before you attempt to acquire and integrate another entity, it's best to know your own entity first. When leaders have in-depth knowledge of their own core focus and strategic, organizational, and operational processes as well as their culture, they are far better positioned to leverage and blend the combined strengths of their own and other entities.

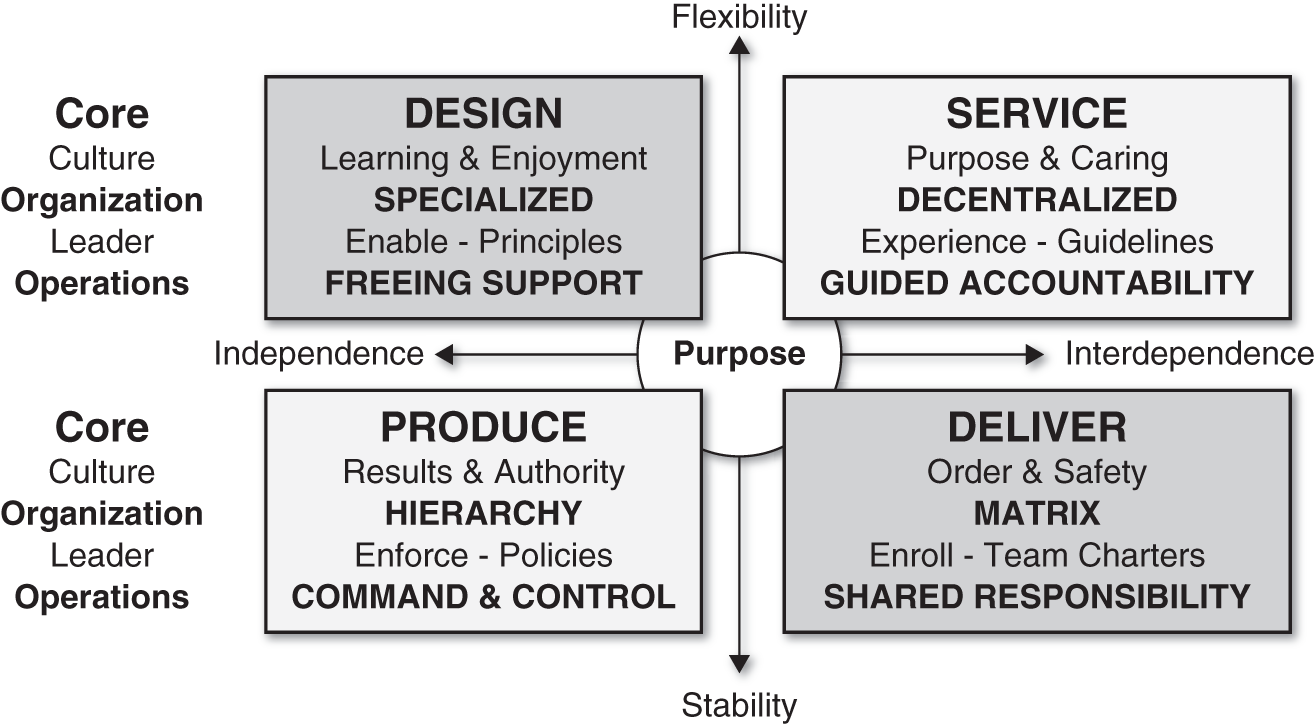

Align on the core focus of the new organization: design, production, delivery, or service (see Figure I.1). That choice dictates the nature of your culture, organization, and ways of working.

FIGURE I.1 The Core Focus

Similarly, understand the business context in which you're operating. Your strategy revolves around a set of choices about the markets, segments, and customers you'll serve. Know and understand them better than anyone else.

The fundamental U-shaped profit curve for almost every industry is that the vast majority of profits accrue to the most innovative who sell fewer “units” at higher prices and margins at the top and to the low-cost producers who make higher than average margins at the “market” price.

Choose whether your innovation will drive higher prices—most likely in design or service-focused organizations—or drive down your production or delivery costs.

If you can't define the value you are seeking to create, it doesn't exist. Get clear on the desired outcomes for your markets, segments, customers, organization, shareholders, and people—as well as how new value is going to be created with choices around where you will:

- Win by being predominant/top 1 percent, superior/top 10 percent, strong/top 25 percent

- Not lose by being above average/competitive, good enough/scaled, or

- Not do by outsourcing or not doing at all

Play this out through the investment case fundamentals:

- Pay fair value for what company is currently worth.

- Grow top-line (organically and inorganically) innovating with customers through people.

- Make operational–operational engineering improvements, cutting costs.

- Invest in top-line and bottom-line enablers including technology to accelerate progress.

- Improve cash flows and pay down debt.

- Exit or recapitalize when this round of value creation is done.

We look at this in the four chapters of the strategic playbook:

The Commercial Playbook

One private equity firm looked at its 25 years of deals across its eight separate funds. They calculated that 30 percent of their portfolio companies' revenue growth over time had been organically fueled by their own innovation, marketing, and sales while 70 percent came from further acquisitions. In most cases you'll need both. Organic revenue growth is harder and riskier, but you keep all of it.

There's an important difference between value creation and value capture. Value is created when a customer pays someone for a product or service that costs the supplier less than the price paid. This is why you have to think customer-back to create value by innovating to provide more valuable products and services than your competitors do.

Don't read this wrong. There's nothing wrong with capturing value from competitors—generally by undercutting their price to take market share. This is why the price of everything gets competed down to its marginal cost over time. You don't want to be the ultimate winner of the race to the bottom. But you can make a lot of money winning some of the stages along the way.

We didn't include marketing and sales in the core focus chart shown in Figure I.1. That chart is derived from Michael Porter's value chain work in which he suggests every company designs, produces, sells, delivers, and services.3 It turns out the most successful companies focus on one of design, production, delivery, or service in addition to marketing and selling.

We look at this in the three chapters of the commercial playbook:

The Operational Playbook

The operational processes that worked before your merger or acquisition may not be adequate to deliver your future ambitions. Maintain and evolve the best of your current processes while leveraging innovation and technology to layer in the new processes required to deliver the needed cost reductions and fuel revenue growth.

Essentially, you're going to need to craft, implement, and manage four plans concurrently:

- Resource allocation and plan (requirements, sources, application): Human, financial, technical, operational

- Rules of engagement across critical business drivers

- Action plan (near-term and long-term): Actions, measures, milestones/timing, accountabilities, linkages

- Performance management plan: Operating and financial performance standards and measures

We look at these in the three chapters of the operational playbook:

- Chapter 8: Cost Optimization: To Free Up Resources to Fuel Commercial Growth

- Chapter 9: Operational Excellence: Supply Chain, Distribution, Continual Improvement

- Chapter 10: Technology: Because All Companies Are Technology Companies Today

The Financial Playbook

Do the deal in a way that reduces your risk of being part of the 83 percent of mergers and acquisitions that fail to deliver the desired results. The first of the many investments you need to get a return on is the purchase price. It is better not to pay enough and lose a deal than to over pay and “win” one of the 30 percent that take a lot of work for no gain, or, even worse, one of the 53 percent that actually destroy value.

The starting point for your deal should be a fair value for what the company is currently worth based on current cash flows. This would reward the seller for what they've built and give you all future value creation. Of course, in the real world, others may be willing to give the seller a portion of the estimated future value. Couple that with some overestimation of possible future value and ego, and it's easy to see how people bid more than they should to “win” bidding contests.

Your real investment is different depending on how you finance the deal. Consider options for funding beyond cash, including equity, seller funding or earnout, and debt in the form of loans, bonds, credit lines, bridge financing, mezzanine, or subordinated debt.

Due diligence is your chance to check your assumptions. If you put a breakup fee in the deal, you did that to allow you to walk away if appropriate. Historically, 83 percent of the time others should have done that. Do due diligence in multiple phases to manage resource allocations (e.g., time, costs, opportunity). Do some before negotiating, some while negotiating, and some between contract and close to avoid wasting much time and resources on low probability or low-impact deals.

Learn as much as you can about the strategic, organizational, and operational processes and culture of the entity you're acquiring. Don't just take third parties' opinions; be active in learning as much as you can—as soon as you can.

- Check your assumptions about the value creators that can enhance competitive advantages, increase impact, and enable top-line growth with customers.

- Check your assumptions about cultural compatibility. Because if you can't make the people work, nothing else matters.

- Check your assumptions about synergistic cost reductions that can fuel investment in the value creators.

- Look for other investments that will be new and needed for the combined company and need to be planned for and part of the strategy.

- Then make a go or no-go decision being clear on the advantage of cutting your losses before they become material.

We look at this in the three chapters of the financial playbook:

- Chapter 11: The Deal/Due Diligence: Iteratively

- Chapter 12: Financing the Deal: The Different Options

- Chapter 13: Further M&A: Enabling Commercial and Operational Success

The Governance Playbook

You need a license to drive a car. And you need licenses to do mergers and acquisitions. Those licenses come from government regulators, banks, and other investors and get translated and managed by your board.

We look at this across the three chapters of the governance playbook:

- Chapter 14: Regulatory: And the License to Play

- Chapter 15: Financial Governance: Always Necessary

- Chapter 16: The Board: And Its Multiple Roles

The Organizational Playbook

The root cause of many mergers' success or failure is culture. Choose the behaviors, relationships, attitudes, values, and environment (BRAVE) that will make up your new culture. Make sure you are encouraging helpful things and discouraging unhelpful things with your incentives and other tools. Also, as you're choosing key leaders and the broader team, keep in mind that you are inviting people into the new culture, noting who really accepts your invitation in what they say, do, and are.

Take a hard look at the combined organization's skills and capabilities through the lens of the new core focus and strategy to determine if any critical capability sets are missing or misaligned. Not only look at the people, plans, and practices, but also pay particular attention to how well you are performing in the markets, segments, and customers you've decided to pursue. Quickly move to bridge any gaps that exist.

Start by defining the right structure and roles to execute on your mission. Be specific about talent, knowledge, skill, experience, and craft requirements for success in each key role, and then match them with the right people.

- Innate talent: Either born with or not

- Learned knowledge: From books, classes, or training

- Practiced skills: From deliberate repetition

- Hard-won experience: Digested from real-world mistakes

- Apprenticed craft: Absorbed over time from masters with artistic care and sensibilities

We look at this across the five chapters of the organization playbook:

- Chapter 17: Culture: The Underlying Root Cause of Nearly Every Merger's Success or Failure

- Chapter 18: Incentives: Show Me How They're Paid and I'll Tell You What They Do

- Chapter 19: Leadership: Starting with the Core Leadership Team

- Chapter 20: People: Acquire, Develop, Encourage, Plan, Transition

- Chapter 21: Politics: What Current and New Leaders Need to Know Organizationally and Personally

The Change Management Playbook

We've all seen organizations acquire other organizations and then run them as wholly owned, separate entities. You can't possibly realize synergies out of separate organizations. Synergies must be created together by teams looking beyond themselves to new problems they can solve for others. This is why a deliberate and detailed integration plan that spans across organizational, operational, strategic, and cultural issues is essential.

All lasting change is cultural change in attitudes, relationships, and behaviors following a point of inflection change in environment or situation and ambition and objectives. Manage that cultural transformation purposefully, deliberately, actively, and in detail. Have a cultural transformation plan in place. When you merge cultures well, value is created. When you don't, value is destroyed.

Implement systems to track, assess, and adjust daily, weekly, monthly, quarterly, and annually: Don't confuse communication with operating cadences. Avoid the public company sprint to do things just ahead of quarterly earnings calls, instead staying ahead of the curve at all times.

- Balanced scorecard (e.g., financial, customer, internal business processes, learning and growth)

- Finance (e.g., revenue, cash flow and cash conversion cycle, earnings before interest, taxes, depreciation, and amortization [EBITDA], return on investment)

- Customer (e.g., sales from new products, on-time delivery, share, customer concentration)

- Internal business processes (e.g., cycle time, unit cost, yield, new product development)

- Learning and growth (e.g., time to market, product life cycle)

We look at this across the five chapters of the change management playbook:

- Chapter 22: Integration Leadership: Start Here

- Chapter 23: Change Management: Leading Through the Point of Inflection

- Chapter 24: Communication: Everything Communicates

- Chapter 25: Announcement Cascade: Emotional, Direct, Indirect

- Chapter 26: Adjustments: Because You’ll Need Them

Prototypical Order

Chapter 27, “Prototypical Order,” covers the last step: preparing for further growth and transformation like the next exit or other “event” as a platform company or bait for strategic buyer. When preparing for an exit, get the story right:

- Strategically: Organic revenue growth; Other M&A

- Organizationally: Buyable management team; Capabilities valuable to others

- Operationally: Buyable infrastructure (Assets, data, IT systems, financial reporting;) Processes; New product development capabilities

- Personally: Making yourself invaluable to the next owners

What really matters is how you influence others and the impact you all make together. Do start with the context and industry landscape. Do align people, plans, and practices around a shared purpose to create commercial and other value. Do the cost-cutting required to free up the resources you need to strengthen the combined entity's culture and strategic, organizational, and operational processes. Do that, thinking customers, then capabilities, then cash, and the merger and acquisitions you lead will go well.