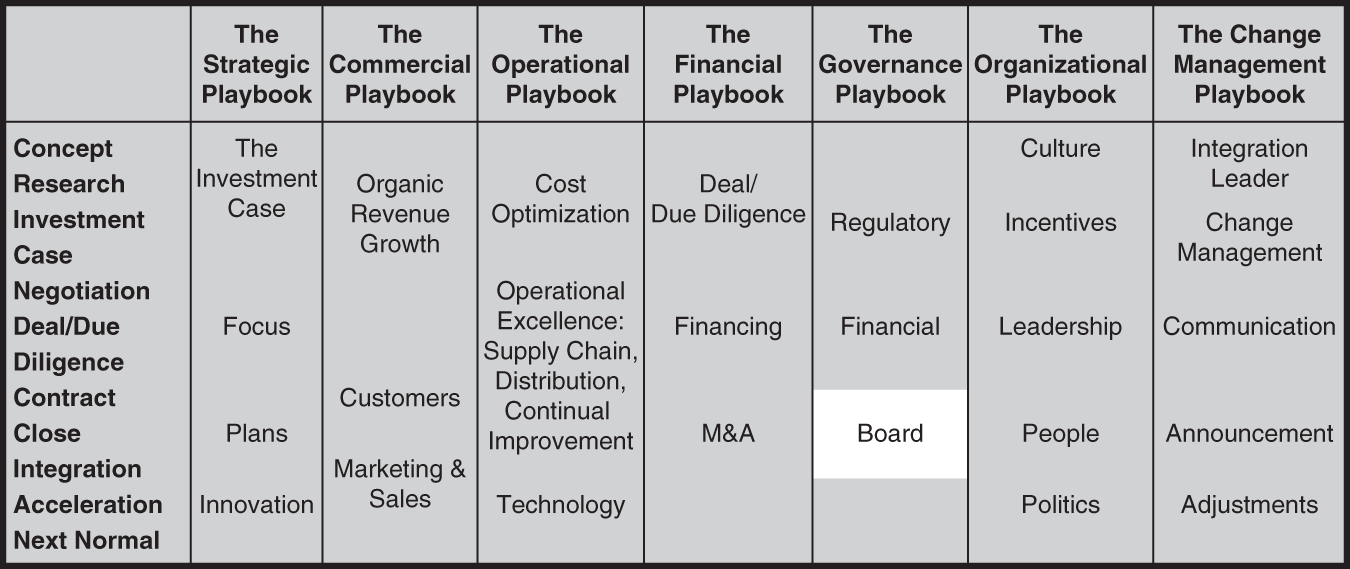

CHAPTER 16

The Board: And Its Multiple Roles

The third component of the governance playbook is the board. Boards play multiple roles: part governance and part advisory. Building the right board can make a massive impact on the success of a merger or acquisition.

In general, boards are accountable for governance and oversight as highlighted in Figure 16.1. They approve strategic, annual operating (profit and loss [P&L], cash flows, balance sheet), future capability, succession, contingency, and compensation plans and are consulted and informed on everything else. More specifically:

Public boards normally have fiduciary duties of care and loyalty in the best interest of their corporations and of all their shareholders and stakeholders, including customers, employees, suppliers, and communities. These boards are subject to the strictest public regulation and scrutiny even beyond their traditional fiduciary responsibilities (legal, regulatory, audit, compliance, risk, and performance reporting) to their input into strategy, mergers and acquisitions (M&A), technology, culture, talent, resilience, and external communications.

FIGURE 16.1 Board Roles and Management

Private fiduciary boards represent the owners of nonpublic companies. Although they are not subject to all the regulations and scrutiny that boards of public companies face, they are subject to many of them and must look out for the interests of all the owners, debt holders, and stakeholders.

Nonfiduciary boards (private or public) are really advisory boards. While the controlling owners may vest board members with some decision rights, those owners can overrule board members at any time and thus maintain the real fiduciary responsibility. Those owners may be private equity firms, families, or individuals. Their organizations may be operating with different levels of maturity. In particular, early-stage companies come with their own special sets of issues and opportunities.

Nonprofit board members serve different roles across governance, getting or giving money, representing stakeholders, making connections, and contributing their own advice or time.

RACI Terms

Leverage RACI to clarify decision rights, accountabilities, and communication protocols.

- Approving authority: Passes accountability to someone else, retaining approval and decision rights

- Accountable: The person called to account. Overall ownership of results. Drives decisions. Ensures implementation.

- Responsible: Does defined work (and signs off on their portion)

- Consulted: Provides expertise-based input (to be considered) and/or direction/concurrence (to be followed)—Two-way conversations.

- Informed: In advance or after the fact—One-way communication

- Support: Assist in completing the work

Board Roles

Be clear on board roles.

- Air cover: Dealing with some owners and stakeholders to free up the chief executive officer's (CEO) time

- Accountable for governance and oversight on behalf of owners and stakeholders (Noses in—especially through audit committee interacting directly with the chief financial officer [CFO] and so forth)

- Approves strategic, annual operating (P&L, cash flows, balance sheet), future capability, succession, contingency, and compensation plans.

- Consulted and informed on everything else (hands out)

- Hire and fire the CEO

- Evaluate, compensate, and develop the CEO and their leadership team

CEO Role

- Accountable for strategic, operating, organization plans and results, culture

Board Management

Chair accountable for board management

- Operations (committees) and board organization

CEO responsible for board management

- Prepare and brief in advance, manage meetings, follow up

- Manage board, group, one-on-one, board two-step: (1) test or consult; (2) sell

Some private equity firms support their portfolio companies in increasing value by providing:

- Perspective on customers, collaborators including community leaders, competitors, and conditions to drive organic growth

- Connecting company leaders with potential customers and collaborators

- Increased leverage in mergers and acquisitions to drive inorganic growth

- Perspective and resources to strengthen company infrastructure, including human capital and management team, technical and information technology, new product development, financial infrastructure for reporting, and managing cash flows

- Review commercial competitiveness of the business and advise on the strategic and operating plans

The Right Way to Divide Responsibilities Between Chair and CEO

There is no single right way to divide responsibilities among owners, chairs, CEOs, chief operations officers (COOs), and the rest of the executive team. Authority is delegated. That delegation is dependent on the business context and confidence the leaders have in one another.1

Having said that, Rita's Italian Ice and Falconhead Capital—the investment firm that owns a controlling interest of the company—have a pretty good working model. Rita's executive chair of the board Mike Lorelli explained to George how they've broken down the roles:

The executive chair takes the lead on:

- Running the board of directors

- Dealing with external funding (investors and lenders)

- Joint venture pursuits and relations

- Compensation practices

- Management development

- CEO succession

- Strategic plan guidance

- M&A

The CEO takes the lead on running the company, across its:

- Strategic process

- Operating process

- Organizational process

But that's just at this moment in time. Back up a couple of years. Falconhead Capital's then CEO David Moross recruited Lorelli to represent Falconhead on the board of Rita's. Once he understood what was going on, Lorelli started recruiting for a new CEO for Rita's in March 2013 while the old CEO was still in place. As one of PrimeGenesis' partners Rob Gregory puts it, “Never fire anyone until you know who's going to do their job.”

Great theory. As the situation dictated, Lorelli needed to change out both the CEO and CFO in June. So he jumped in as interim CEO. A month later, Lorelli met Jeff Moody, and they hit it off as only two ex-Pepsi employees can do. After several long conversations, a double date, and walks in the woods à la Steve Jobs and John Scully, during which they “nurtured” their relationship, Moody came onboard as CEO.

Lorelli had been conscious about managing his own transition from interim CEO to executive chair. As soon as Moody joined, Lorelli immediately vacated his CEO office and moved to an office as far away from Moody as possible. He backed off even more over time as both he and Moody became more and more comfortable in their roles.

Lorelli said, “The roles of executive chair and CEO should not be just additive but also synergistic.” It's essential to have clear lines of authority. It's even better when the two share chemistry and can bounce ideas off each other. Moody described the split as “a soft division” with clear categories of responsibility but major overlaps as partners.

When it works, it works great. Think about how Bill Gates backed off and gave Steve Ballmer room to run Microsoft. Think about Ajay Banga's transition into Mastercard.

But when it doesn't work, the pain and suffering are spread across all of those people who are trying to follow their leaders. If leaders can't sort through their own responsibilities, they have no chance of providing clear direction to anyone else. And don't kid yourself—there are no secrets in any company (no matter how large or small).

In summary, here is a rough guide for dividing responsibilities between a chair and CEO:

- Owners delegate authority to boards.

- Chairs or lead directors run boards. (This is the only responsibility of a nonexecutive chair. Executive chairs are employees of the companies by definition and take more active roles in supporting the CEO's leadership of the company.)

- CEOs run companies.

- COOs, CFOs, chief human resource officers (CHROs), and others help CEOs run core operating, strategic, and organizational processes.

- People lean in or out depending on their confidence in the ability of the people they have chosen to deal with.

Treat this as a general framework. What really matters is clear leadership that inspires and enables others. Titles don't matter. Formal divisions of responsibility don't matter. Behaviors, relationships, attitudes, values, and the environment matter. Focus on these at every level and every interaction in the organization.

How to Build Mutual Respect, Trust, and Support Between CEOs and Boards per Deloitte

Deloitte's chief executive program published a paper on “Seven Steps to a More Strategic Board.” Its insights are well worth reading. They did, however, bury the lead. The seven steps add up to the importance of CEOs taking a leadership role in managing boards and building relationships rooted in “mutual respect, trust, and support.” That's the lead.2

Deloitte's seven steps are as follows:

- CEOs, it's really up to you. Take an active role in board management.

- Be fearlessly transparent. Be open and humble.

- Take advantage of tension. Grow through debate.

- Facilitate the board experience, not just the board meeting. Build relationships over time.

- Curate information and then curate it again. Give enough, but not too much information.

- To chair or not to chair? Think about it very carefully. Choose your level of influence.

- Say your piece on board composition. Build the right board over time.

Relationships rooted in “mutual respect, trust, and support” don't happen by mistake. They are built together, deliberately, and over time.

Respect

Be respectful of board members' context, strengths, roles. Give them every reason to respect you. Respect their time and help them learn enough to contribute as effectively and efficiently as possible.

Per one director, “Too much information can be just as bad as too little information.” You can keep boards in the dark by giving them too little information too infrequently. You can accomplish the same end by drowning them with a board book on an iPad “and secretly hidden are 1,800 pages.”

Think what, so what, now what. Then lead with the “now what” you're asking the board member to do. Do you want them thinking guidance, advice, and input or thinking governance, compliance, and approval? Then give them your perspective on “so what.” These are your conclusions from the information that leads to your request for input or approval. Finally, organize the back-up “what” data and information in a way that makes it searchable by the board members that want to dig deeper into the basis of your assumptions and logic.

Another way to respect board members is not to surprise them. No one likes surprises that make them look stupid, weak, or ill-informed. Treat your board members like they are, well, board members. Build relationships with them. Keep them informed. No excuses.

Finally, do the same future capability planning with your board that you're doing with the rest of the organization. Figure out what capabilities you're going to need in the future and then create and implement a plan to recruit board members with the talents you need and to help them acquire the knowledge and practice the skills they'll need to optimize their contributions.

Trust

At one level, this is pretty straightforward. Be trustworthy and have a bias to trust them. This is one of the keys to taking advantage of constructive disagreements. As the Deloitte paper put it:

With a strong partnership between the board and CEO, what at first may feel like difficult conversations can become revelatory dialogues, surfacing ideas and insights that might otherwise stay buried from a desire to smooth tension and maintain civility.3

Support

One of the Deloitte paper's authors, Maureen Bujno, told George the key to gaining respect, trust, and support lies in CEOs being “fearlessly transparent” and “open to soliciting input.” Yet Stanford Business School ex-dean Robert Joss once said, “Only 20 percent of leaders have the confidence to be open to input.” Be part of that 20 percent.

Help board members know when to provide guidance, advice, and input and when to exercise their fiduciary obligations around governance, compliance, and approvals.

The board two-step can help a lot here:

Step 1: Seek their input. Then go away so they talk among themselves or with others or give you off-the-record perspective.

Step 2: Taking into account their input and encouraging debate, seek their approval to your recommended path forward.

Notes

- 1 Bradt, George, 2013, “The Right Way to Divide Responsibilities Between Chairman and CEO,” Forbes (August 28).

- 2 Bradt, George, 2019, “How to Build Mutual Respect, Trust and Support Between CEOs and Boards per Deloitte,” Forbes (July 9).

- 3 https://www2.deloitte.com/us/en/insights/topics/leadership/strategic-board-of-directors-ceo.html.