18

Tokenization

A token is a representation of an object. We use tokens in many different fields, including economics and computing. In daily life, tokens have been used to represent something of value, such as a gift voucher that is redeemable in exchange for items. In computing, different types of tokens are used, which can be defined as objects that represent eligibility to perform some operation. For example, an access token is used to identify a user and its privileges on a computer system. A hardware security token is used in computer systems to provide a means to authenticate a user (verify their identity) to a computer system. Tokens are also used in computer security mechanisms to substitute sensitive data with non-sensitive equivalents to prevent direct access to sensitive information. For example, in mobile payment systems, tokens are used to safeguard credit card information, which is represented by a token on the mobile device instead of the actual credit card data.

Just like the general use of tokens in day-to-day life, in the blockchain world, tokens also represent something of value. However, the critical difference is that the token exists digitally on a blockchain and is operated cryptographically, which means that they are generated, protected, and transferred using cryptographic protocols. Now that we understand what a token is, we can define tokenization as a process that converts an asset to a digital token on a blockchain. Specifically, it is a process of converting the ownership rights of a real-world asset into a cryptographic/digital token on a blockchain.

In this chapter, we will cover blockchain tokens (or crypto-tokens) and tokenization. We will use the term token from now on to represent tokens on a blockchain. We will also cover different types of tokens, relevant standards, tokenization platforms, applications of tokenization, and a practical example of how to develop tokens on Ethereum. A guide to the specific topics we will cover in this chapter is provided here:

- Tokenization on the blockchain

- Types of token

- Token offerings

- Token standards

- Trading and finance

- DeFi

- Building an ERC-20 token

- Emerging concepts

Now, we'll begin our discussion on tokenization in the context of blockchain, which is the main aim of this chapter.

Tokenization on a blockchain

Tokenization, in the context of blockchain, is the process of representing an asset digitally on a blockchain. It can be used to represent commodities, real estate, ownership of art, currency, or anything else of value.

Remember, for the rest of the chapter when we refer to tokenization, it is in the context of blockchain.

After this brief definition, let's explore how tokenization can be beneficial.

Advantages of tokenization

Tokenization provides several benefits, including faster transaction processing, flexibility, low cost, decentralization, security, and transparency. The following are some of the most important of these benefits:

- Faster transaction processing: As transactions and all relevant parties are present on the blockchain and readily available, there is no need to wait for a response from a counterparty or to wait for clearing and settlement operations. All these operations can be performed efficiently and quickly on a blockchain.

- Flexibility: Due to the worldwide adoption of systems that use tokens, such as payment systems, tokenization becomes simple due to easier cross-border use.

- Low cost: In comparison with traditional financial products, tokenization requires a lower cost to implement and incurs a lower cost to the end user due to digitization. Generally, in finance we have seen that digitization, starting from the introduction of digital accounts in the 1960s, has led to more efficient and cheaper financial systems. More recently, the introduction of digital payments has revolutionized the financial industry. In the same spirit, tokenization using blockchain can be considered another step toward achieving further efficiency and cost reduction. In fact, tokenization gives rise to a better, more efficient, and more democratic financial system. For example, just being able to share customer data recorded on one blockchain across all financial institutions reduces costs. Similarly, the possibility of converting illiquid assets into liquid assets is another way of increasing efficiency and profits.

- Decentralization: Tokens are presented on a public blockchain, leveraging the decentralization offered by blockchain technology. However, in some cases, a level of somewhat acceptable centralization is introduced due to the control and scrutiny required by investors and exchanges and other involved and interested parties.

We discussed the benefits of decentralization in detail in Chapter 2, Decentralization. Readers can refer to that chapter to review decentralization.

- Security: As tokens are cryptographically protected and produced using a blockchain, they are secure. However, note that proper implementation must use good practice and meet established security industry standards, otherwise security flaws may result in exploitation by hackers, leading to financial loss.

- Transparency: Because they are on a blockchain, tokens are more transparent than traditional financial systems, meaning that that any activity can be readily audited on a blockchain and is visible to everyone.

- Trust: As a result of the security and transparency guarantees, more trust is naturally placed in tokenization by investors.

- Fractional ownership: Imagine a scenario in which you own a painting by Vincent van Gogh. It is almost impossible in traditional scenarios to have multiple owners of the painting without immense legal, financial, and operational challenges. However, on a blockchain using tokens, any asset (such as our Van Gogh painting) can be fractionalized in such a way that it can be owned in part by many investors. The same situation is true for a property: if I wanted to have shared ownership with someone, it requires complicated legal procedures. However, with tokenization, fractional ownership of any asset, be it art, real estate, or any other off-chain real-world asset, is quick, easy, efficient, secure, and a lot less complicated than traditional methods.

- Low entry barrier: Traditional financial systems require traditional verification mechanisms, which can take a long time for a customer. While they are necessary and serve the purpose in traditional financial systems, these processes take a long time due to the necessary verification processes and the involvement of different entities. However, on a blockchain, this entry barrier is lowered because there is no need to go through the long verification checks. This is because not only is tokenization based on cryptographic guarantees provided by the blockchain, but for many decentralized applications (DApps) in this ecosystem, it is basically just a matter of downloading a DApp on your mobile device, depositing some funds if required, and becoming part of the ecosystem.

- Innovative applications: Tokenization has resulted in many innovative applications, including novel lending systems on blockchain, insurance, and other numerous financial applications, including decentralized exchanges. Securities can now be tokenized and presented on blockchain, which results in client trust and satisfaction because of the better security and faster processing times. An example of this innovation is DeFi, which we will discuss later on in the chapter.

- More liquidity: This is due to the easy availability and accessibility of the tokens for the general public. By using tokens, even illiquid assets such as paintings can be tokenized and traded on an exchange with fractional ownership.

With all these advantages there are, however, some issues that must be addressed in the tokenization ecosystem. We'll discuss these next.

Disadvantages of tokenization

In this section, we present some of the disadvantages of tokenization. At the top of the list we have regulatory requirements:

- Regulatory issues: Regulation is a crucial subject of much debate. It is imperative that the tokens are regulated so that investors can have the same level of confidence that they have when they invest using traditional financial institutions. The big issue with tokenization and generally any blockchain technology is that they are mostly decentralized and in cases where no single organization is in control, it becomes quite difficult to hold someone responsible if something goes wrong. In a traditional system, we can go to the regulatory authorities or the relevant ombudsman services, but who is held responsible on a blockchain?

Some of this situation has changed with recent security tokenization standards and legislation, which consider tokens as securities. This means that security tokens will then be treated as securities, and the same legal, financial, and regulatory implications will be placed on these tokens that are applicable in the currently established financial industry. Refer to https://www.sec.gov/answers/about-lawsshtml.html, where different laws that govern the securities industry are presented. This helps to increase customer confidence levels and trust in the system; however, there are still many challenges that need to be addressed.

A new type of financial crime might be evolving with this tokenization ecosystem where, instead of using well-known and researched traditional financial fraud methods, criminals may choose to launch a technically sophisticated attack. For an average user, this type of attack is difficult to spot and understand as they are entirely on a blockchain and digitized. New forms of front running and market skewing on decentralized finance platforms is increasingly becoming a concern.

- Legality of tokens: This is a concern in some jurisdictions where tokens and cryptocurrency are illegal to own and trade.

- Technology barrier: Traditional financial systems have been the norm with brick and mortar banks. We are used to that system, but things have changed and are expected to change rapidly with tokenization. Tokenization-based financial ecosystems are easier to use for a lot of people, but for some, technological illiteracy can become an issue and could become a barrier. Sometimes the interfaces and software applications required to use tokenization platforms such as trading platforms are difficult to use for an average user.

- Security issues: The underlying blockchain technology is considered solid from a security point of view, and it is boasted sometimes that due to the use of cryptography, it is impossible to launch attacks and commit fraud on a blockchain. However, this is not entirely true, even with the firm security foundation that blockchains provide. The way tokenization platforms and DApps are implemented on the blockchain result in security issues that can be exploited by hackers, potentially leading to financial loss. In other words, even if the underlying blockchain is relatively secure, the tokenization DApp implemented on top may have vulnerabilities that could be exploited. These weaknesses could have been introduced by poor development practices or inherent limitations in the still-evolving smart contract languages.

In this section, we have looked at some of the pros and cons of tokenization. Next, let's look at some of the many types of token. Naturally, the way tokenization has been evolving in the last few years, there are now new and different types of tokens that are present in the ecosystem.

Types of tokens

With the rapid development of blockchain technology and the related applications, there has been a tremendous increase in the development of various types of token and relevant ecosystems. First, let's clarify the difference between a coin and token. Is a Bitcoin a token? Or are tokens and coins the same thing?

A coin is a native token of a blockchain. It is the default cryptocurrency of the blockchain on which it runs. Common examples of such a token are Bitcoin and ether. Both of these tokens or coins have their own native blockchain on which they run: the Bitcoin blockchain and the Ethereum blockchain.

On the other hand, a token is a representation of an asset that runs on top of a blockchain. For example, Ethereum not only has its own ether cryptocurrency as a native token (or coin) but also has thousands of other tokens that are built on top of Ethereum for different applications. Thanks to its support of smart contracts, Ethereum has become a platform for all sorts of different types of tokens ranging from simple utility tokens to game tokens and high-value, application-specific tokens.

Now that we understand the difference between a coin and a token, let's have a look at the usage and significance of different types of tokens. Tokens can be divided broadly into two categories based on their usage: fungible tokens and non-fungible tokens.

Fungible tokens

From an economics perspective, fungibility is the interchangeability of an asset with other assets of the same type. For example, a ten-pound note is interchangeable with a different ten-pound note or two five-pound notes. It does not matter which specific denominations they are: as long as they are of the same type (pound) and have same value (the sum of two five-pound notes), the notes are acceptable.

Fungible tokens work on the same principle. They are:

- Indistinguishable: Tokens of the same type are indistinguishable from each other. In other words, they are identical.

- Interchangeable: A token is fully interchangeable with another token of the same value.

- Divisible: Tokens are divisible into smaller fractions.

Non-fungible tokens

Let's consider non-fungible tokens (NFTs), also called nifty, with the help of an example. We saw that fungibility allows the same types of token to be interchangeable, but non-fungible tokens are not interchangeable. For example, a collectible painting is a non-fungible asset, as it cannot be replaced with another painting of the same type and value. Each painting is unique and distinguishable from others.

Non-fungible tokens are:

- Unique: Non-fungible tokens are unique and different from other tokens of the same type or in the same category.

- Non-interchangeable: Since they are unique and represent specific attributes, these tokens are not interchangeable with tokens of the same type. For example, a rare painting is unique due to its attributes and is not interchangeable with another, even an exact-looking replica. We can also think about the certificate of authenticity that comes with a rare painting: that is also non-interchangeable with another due to its unique attributes representing the rare art.

- Indivisible: These tokens are available only as a complete unit. For example, a college diploma is a unique asset distinguishable from other diplomas of the same type. It is associated with a unique individual and is thus not interchangeable and it is not rational for it to be divided into fractions, making it indivisible.

One of the prime examples of NFTs is the game CryptoKitties—https://www.cryptokitties.co. It can be said that CryptoKitties played a big role in the popularity of non-fungible tokens. This is due to the fact that CryptoKitties was the first game (DApp) that was based on NFTs and, because of the interesting nature of the game, the community grew and many researchers and gamers developed interest not only in the game but also the underlying NFT mechanism. Also, this interest gave rise to more projects based on NFTs. A popular term, "crypto collectibles," also emerged with this development. Some other projects that use NFT and offer crypto collectibles include Gods Unchained, Decentraland, Skyweaver, and My Crypto Heroes.

In the next section, we introduce another interesting topic, stable tokens, which are a different type of token with interesting properties that make them more appealing to some investors.

Stable tokens

Stable tokens or stable coins are a type of token that has its value pegged to another asset's value, such as fiat currencies or precious metals. Stable tokens maintain a stable price against the price of another asset.

Bitcoin and other similar cryptocurrencies are inherently volatile and experience dramatic fluctuations in their price. This volatility makes them unsuitable for usual everyday use. Stable tokens emerged as a solution to this limitation in tokens.

The price stability is maintained by backing the token up by a stable asset. This is known as collateralization. Fiat currencies are stable because they are collateralized by some reserve, such as foreign exchange (forex) reserves or gold. Moreover, sound monetary policy and regulation by authorities play a vital role in the stability of a currency. Tokens or cryptocurrencies lack this type of support and thus suffer from volatility.

There are four types of stable coin.

Fiat collateralized

These stable tokens are backed by a traditional fiat currency such as US dollars. Fiat collateralized coins are the most common type of stable coins. Some of the common stable coins available today are Gemini Dollar (GUSD) (https://gemini.com/dollar), Paxos (PAX) (https://www.paxos.com/pax/), and Libra (https://libra.org/).

Commodity collateralized

As the name suggests, these stable coins are backed up by fungible commodities (assets) such as oil or gold. Common examples of such tokens are Digix gold tokens (https://digix.global) and Tether gold (https://tether.to).

Crypto collateralized

This type of stable coin is backed up by another cryptocurrency. For example, the Dai stable coin (https://makerdao.com/en/) accepts Ethereum-based assets as collateral in addition to soft pegging to the US dollar.

Algorithmically stable

This type of stable token is not collateralized by a reserve but stabilized by algorithms that keep track of market supply and demand. For example, Basecoin (https://basecoin.cc) can have its value pegged against the US dollar, a basket (a financial term for group, or collection of similar securities) of assets, or an index, and it also depends on a protocol to control the supply of tokens based on the exchange rate between itself and the peg used, such as the US dollar. This mechanism helps to maintain the stability of the token.

Security tokens

Security tokens derive their value from external tradeable assets. For example, security tokens can represent shares in a company. The difference is that traditional security is kept in a bank register and traded on traditional secondary markets, whereas security tokens are available on a blockchain. Being securities, they are governed by all traditional laws and regulations that apply to securities, but due to their somewhat decentralized nature, in which no middle man is required, security tokens are seen as a more efficient, scalable, and transparent option.

Now that we have covered different types of token, let's see how an asset can be tokenized by exploring the process of tokenization.

Process of tokenization

In this section, we'll present the process of tokenization, discuss what can be tokenized, and provide a basic example of the tokenization of assets.

Almost any asset can be tokenized and presented on a blockchain, such as commodities, bonds, stocks, real estate, precious metals, loans, and even intellectual property. Physical goods that are traditionally illiquid in nature, such as collectibles, intellectual property, and art, can also be tokenized and turned into liquid tradeable assets.

A generic process to tokenize an asset or, in other words, offer a security token, is described here. Note that there are many other technical details and intricacies involved in the process that we are skipping for brevity:

- The first step is to onboard an investor who is interested in tokenizing their asset.

- The asset that is presented for tokenization is scrutinized and audited, and ownership is confirmed. This audit is usually performed by the organization offering the tokenized security. It could be an exchange or a cryptocurrency start-up.

- The process of tokenized security starts, which leads to the security token offering (STO).

- The physical asset is placed with a custodian (in the real world) for safekeeping.

- The derivative token, representing the asset, is created by the organization offering the token and issued to investors through a blockchain.

- Traders start to buy and sell these tokens using trading exchanges in a secondary market and these trades are settled (the buyer makes a payment and receives the goods) on a blockchain.

Common platforms for tokenization include Ethereum and EOS. Tezos is also emerging as another platform for tokenization due to its support for smart contracts. In fact, any blockchain that supports smart contracts can be used to build tokens.

At this point, a question arises about how all these different types of token reach the general public for investment. In the next section, we examine how this is achieved by first explaining what token offerings are and examining the different types.

Token offerings

Token offerings are mechanisms to raise funds and profit. There are a few different types of token offerings. We will introduce each of these separately now. One main common attribute of each of these mechanisms is that they are hosted on a blockchain and make use of tokens to facilitate different financial activities. These financial activities can include crowdfunding and trading securities.

Initial coin offerings

Initial coin offering or initial currency offering (ICO) is a mechanism to raise funds using cryptocurrencies. ICOs have been a very successful but somewhat controversial mechanism for raising capital for new cryptocurrency or token projects. ICOs are somewhat controversial sometimes due to bad design or poor governance, but at times some of the ICOs have turned out to be outright scams. A list of fraudulent schemes is available at https://cryptochainuni.com/scam-list/. These types of incidents have contributed toward the bad reputation and controversy of ICOs in general. While there are some scams, there are also many legitimate and successful ICOs. The return on investment (ROI) for quite a few of ICOs has been quite big and has contributed toward the unprecedented success of many of these projects. Some of these projects include Ethereum, NXT, NEO, IOTA, and QTUM.

A common question is asked here regarding the difference between the traditional initial public offerings (IPOs) and ICOs, as both of these mechanisms are fundamentally designed to raise capital. The difference is simple: ICOs are blockchain-based token offerings that are usually initiated by start-ups to raise capital by allowing investors to invest in their start-up. Usually in this case, contributions by investors are made using already existing and established cryptocurrencies such as Bitcoin or ether. As a return, when the project comes to fruition, the initial investors get their return on the investment.

On the other hand, IPOs are traditional mechanisms used by companies to distribute shares to the public. This is done using the services of underwriters, which are usually investment banks. IPOs are only usually allowed for those companies who are already well established, but ICOs on the other hand can be offered by start-ups. IPOs also offer dividends as returns, whereas ICOs offer tokens that are expected to rise in value once the project goes live.

Another key comparison is that IPOs are regulated, traditional mechanisms that are centralized in nature, while ICOs are decentralized and unregulated.

Because ICOs have been unregulated, which has resulted in a number of scams and people losing their money, another form of fundraising known as security token offerings was introduced. We'll discuss this next.

Security token offerings

Security token offerings (STOs) are a type of offering in which tokenized securities are traded at cryptocurrency exchanges. Tokenized securities or security tokens can represent any financial asset, including commodities and securities. The tokens offered under STOs are classified as securities. As such, they are more secure and can be regulated, in contrast with ICOs. If an STO is offered on a traditional stock exchange, then it is known as a tokenized IPO. Tokenized IPO is another name for an STO that is used when an STO is offered on a regulated stock exchange, which helps to differentiate between an STO offered on a traditional regulated exchange and one that is offered on cryptocurrency exchanges. STOs are regulated under the Markets in Financial Instruments Directive—MiFID II—in the European Union.

Initial exchange offerings

Initial exchange offering (IEO) is another innovation in the tokenization space. The key difference between and IEO and ICO is that in an ICO, the tokens are distributed via crowdfunding mechanisms to investors' wallets, but in an IEO, the tokens are made available through an exchange.

IEOs are more transparent and credible than IEOs due to the involvement of an exchange and due diligence performed by the exchange.

Equity token offerings

Equity token offerings (ETOs) are another variation of ICOs and STOs. ICOs offer utility tokens, whereas equity tokens are offered in ETOs. When compared with STOs, ETOs offer shares of a company, whereas STOs offer shares in any asset, such as currencies or commodities. From this point of view, ETOs can be regarded as a specific type of STO, where only shares in a company or venture are represented as tokens.

Decentralized autonomous initial coin offering

Decentralized Autonomous Initial Coin Offering (DAICO) is a combination of decentralized autonomous organizations (DAOs) and ICOs that enables investors to have more control over their investment and is seen as a more secure, decentralized, and automated version of ICOs.

Other token offerings

Different variations of ICOs and new concepts are being introduced quite regularly, and innovation is only expected to grow in this area.

A comparison of different types of token offering is presented in the following table:

|

Name |

Concept |

First introduced |

Scale of decentralization |

How to invest |

Regulation |

|

ICO |

Crowdfunding through a utility token |

In July 2013 with Mastercoin |

Semi-decentralized |

Investors send cryptocurrency to a smart contract released by the token offerer. |

Low regulation |

|

STO |

Tokenized security such as bonds and stocks |

2017 |

Somewhat centralized |

Use the exchange provided platform |

Regulated under established laws and directives in many jurisdictions |

|

IEO |

Tokens are made available through an exchange |

2018 |

Somewhat centralized |

Use the exchange provided platform |

Low regulation |

|

ETO |

Offers shares of any asset |

December 2018 with the Neufund ETO |

Somewhat centralized |

Use the exchange provided platform |

Mostly regulated |

|

DAICO |

Combination of DAO and ICO |

May 2018 with ABYSS DAICO |

Mostly decentralized |

Investors send cryptocurrency to the DAICO smart contract |

Low regulation |

With all these different types of tokens and associated processes, a need to standardize naturally arises so that more adoption and interoperability can be achieved. To this end, several development standards have been proposed, which we discuss next.

Token standards

With the advent of smart contract platforms such as Ethereum, it has become quite easy to create a token using a smart contract. Technically, a token or digital currency can be created on Ethereum with a few lines of code, as shown in the following example:

pragma solidity ^0.5.0;

contract token {

mapping (address => uint) public coinBalanceOf;

event CoinTransfer(address sender, address receiver, uint amount);

/* Initializes contract with initial supply tokens to the creator of the contract */

function tokenx(uint supply) public {

supply = 1000;

coinBalanceOf[msg.sender] = supply;

}

/* Very simple trade function */

function sendCoin(address receiver, uint amount) public returns(bool sufficient) {

if (coinBalanceOf[msg.sender] < amount) return false;

coinBalanceOf[msg.sender] -= amount;

coinBalanceOf[receiver] += amount;

emit CoinTransfer(msg.sender, receiver, amount);

return true;

}

}

This code is based on one of the early codes published by Ethereum as an example on ethereum.org.

The preceding code works and can be used to create and issue tokens. However, the issue is that without any standard mechanism, everyone would implement tokenization smart contracts in their own way based on their requirements. This lack of standardization will result in interoperability and usability issues, which obstructs the widespread adoption of tokenization.

To remedy this, the first tokenization standard was proposed on Ethereum, known as ERC-20.

ERC-20

ERC-20 is the most famous token standard on the Ethereum platform. Many token offerings are based on ERC-20 and there are wallets available, such as MetaMask, that support ERC-20 tokens.

ERC-20 was introduced in November 2015 and since then has become a very popular standard for fungible tokens. There are almost 1,000 ERC-20 tokens listed on Etherscan (https://etherscan.io/tokens), which is a clear indication of this standard's popularity. It has been used in many ICOs and has resulted in valuable digital currencies (tokens) over the last few years, including EOS, Golem, and many others.

While ERC-20 defined a standard for fungible tokens and was widely adopted, it has some flaws, which results in some security and usability issues. For example, a security issue in ERC-20 results in a loss of funds if the tokens are sent to a smart contract that does not have the functionality to handle tokens. The effectively "burned" tokens result in a loss of funds for the user.

To address these shortcomings, ERC-223 was proposed.

ERC-223

ERC-223 is a fungible token standard. One major advantage of ERC-223 as compared to ERC-20 is that it consumes only 50% of ERC-20's gas consumption, which makes it less expensive to use on Ethereum mainnet. ERC-223 is backward compatible with ERC-20, and is used in a number of major token projects such as LINK and CNexchange (CNEX).

ERC-777

The main aim of ERC-777 is to address some of the limitations of ERC-20 and ERC-223. It is backward compatible with ERC-20. It defines several advanced features to interact with ERC-20 tokens. It allows sending tokens on behalf of another address (contract or account). Moreover, it introduces a feature of "hooks," which allows token holders to have more control over their tokens.

The Ethereum Improvement Proposal (EIP) is available here:

ERC-721

ERC-721 is a non-fungible token standard. ERC-721 mandates a number of rules that must be implemented in a smart contract for it to be ERC-721 compliant. These rules govern how these tokens can be managed and traded. ERC-721 was made famous by the CryptoKitties project. CryptoKitties is a blockchain game that allows players to create (breed) and trade different types of virtual cats on the blockchain. Each "kitty" is unique and tradeable for a value on the blockchain.

ERC-884

This is the standard for ERC-20 - compliant share tokens that are conformant with Delaware General Corporations Law.

The legislation is available here: https://legis.delaware.gov/json/BillDetail/GenerateHtmlDocument?legislationId=25730&legislationTypeId=1&docTypeId=2&legislationName=SB69

The token standard EIP is available here: https://github.com/ethereum/EIPs/blob/master/EIPS/eip-884.md

ERC-1400

This is a security token standard that defines how to build, issue, trade, and manage security tokens. It is also referred to as ERC-1411 after it was renamed from ERC-1400.

Under ERC-1400, there are a few other standards, which are as follows.

- ERC-1410: A partially fungible token standard that defines a standard interface for grouping an owner's tokens into partitions.

- ERC-1594: This defines a core security token standard.

- ERC-1643: This is the document management standard.

- ERC-1644: This is the token controller operations standard.

- ERC-1066: This standard specifies a standard way to design Ethereum status codes.

The aim of ERC-1400 and the standards within it is to cover all activities related to the issuance, management, control, and processing of security tokens.

ERC-1404

This ERC standard allows the issuance of tokens with regulatory transfer restrictions. These restrictions enable users to control the transfer of tokens in different ways. For example, users can control when, to whom, and under what conditions the tokens can be transferred. For example, an issuer can choose to issue tokens only to a whitelisted recipient or check whether there are any timing restrictions on the senders' tokens.

ERC-1404 introduces two new functions in the ERC-20 standard to introduce restriction and control mechanisms. These two functions are listed as follows:

contract ERC1404 is ERC20 {

function detectTransferRestriction (address from, address to, uint256 value) public view returns (uint8);

function messageForTransferRestriction (uint8 restrictionCode) public view returns (string);

}

More information on ERC-1404 is available at https://erc1404.org.

With this, we have completed our introduction to ERC standards.

Now let's have a quick introduction to finance and financial markets. This will provide a foundation for the material presented next, such as DeFi, as many of the terms and ideas are the same, albeit in a different context.

Trading and finance

Before we move onto exploring one of the largest ecosystems based on tokenization, decentralized finance (DeFi), let's first look at some traditional finance and trading concepts. This will provide a solid foundation for the material presented in the next section and will covers token trading and related concepts such as decentralized exchanges and asset tokenization.

Financial markets

Financial markets enable the trading of financial securities such as bonds, equities, derivatives, and currencies. There are broadly three types of markets: money markets, credit markets, and capital markets:

- Money markets are short-term markets where money is lent to companies or banks for interbank lending. Foreign exchange, or forex, is another category of money markets where currencies are traded.

- Credit markets consist mostly of retail banks who borrow money from central banks and loan it to companies or households in the form of mortgages or loans.

- Capital markets facilitate the buying and selling of financial instruments, mainly stocks and bonds. There are many types of financial instruments, such as cash instruments, derivative instruments, loans, securities, and many more. Securitization is the process of creating a new security by transforming illiquid assets into tradeable financial instruments. Capital markets can be divided into two types: primary and secondary markets. Stocks are issued directly by the companies to investors in primary markets, whereas in secondary markets, investors resell their securities to other investors via stock exchanges. Various electronic trading systems are used by exchanges today to facilitate the trading of financial instruments.

Trading

A market is a place where parties engage in exchange. It can be either a physical location or an electronic or virtual location. Various financial instruments, including equities, stocks, foreign exchanges, commodities, and various types of derivatives are traded at these marketplaces. Recently, many financial institutions have introduced software platforms to trade various types of instruments from different asset classes.

Trading can be defined as an activity in which traders buy or sell various financial instruments to generate profit and hedge risk. Investors, borrowers, hedgers, asset exchangers, and gamblers are a few types of traders. Traders have a short position when they owe something; in other words, if they have sold a contract, they have a short position. When traders buy a contract, they have a long position. There are various ways to transact trades, such as through brokers or directly on an exchange or over the counter (OTC) where buyers and sellers trade directly with each other instead of using an exchange. Brokers are agents who arrange trades for their customers, and act on a client's behalf to deal at a given price or the best possible price.

Exchanges

Exchanges are usually considered to be a very safe, regulated, and reliable place for trading. During the last decade, electronic trading has gained popularity over traditional floor-based trading. Now, traders send orders to a central electronic order book from which the orders, prices, and related attributes are published to all associated systems using communications networks, thus in essence creating a virtual marketplace. Exchange trades can be performed only by members of the exchange. To trade without these limitations, the counterparties can participate in OTC trading directly.

Orders and order properties

Orders are instructions to trade, and they are the main building blocks of a trading system. They have the following general attributes:

- The instrument's name

- The quantity to be traded

- Direction (buy or sell)

- The type of the order that represents various conditions, for example, limit orders and stop orders

In finance, a limit order is a type of order that allows the selling or buying of an asset at a specific price or better. A stop order is similar, but the key difference is that a limit order is visible to the market, whereas a stop order only becomes active (as a market order) when the specified stop price is met.

Orders are traded by bid prices and offer prices. Traders show their intention to buy or sell by attaching bid and offer prices to their orders. The price at which a trader will buy is known as the bid price. The price at which a trader is willing to sell is known as the offer price.

Order management and routing systems

Order routing systems route and deliver orders to various destinations depending on the business logic. Customers use them to send orders to their brokers, who then send these orders to dealers, clearing houses, and exchanges.

There are different types of orders. The two most common ones are market orders and limit orders. A market order is an instruction to trade at the best price currently available in the market. These orders get filled immediately at spot prices.

In finance, spot price is a term used to refer to the current price of an asset in a marketplace at which it can be bought or sold for immediate delivery.

On the other hand, a limit order is an instruction to trade at the best price available, but only if it is not lower than the limit price set by the trader. This can also be higher depending on the direction of the order: either to sell or buy. All of these orders are managed in an order book, which is a list of orders maintained by the exchange, and it records the intention of buying or selling by the traders.

A position is a commitment to sell or buy a number of financial instruments, including securities, currencies, and commodities for a given price. The contracts, securities, commodities, and currencies that traders buy or sell are commonly known as trading instruments, and they come under the broad umbrella of asset classes. The most common classes are real assets, financial assets, derivative contracts, and insurance contracts.

Components of a trade

A trade ticket is the combination of all of the details related to a trade. However, there is some variation depending on the type of the instrument and the asset class. These elements are described here.

The underlying instrument

The underlying instrument is the basis of the trade. It can be a currency, a bond, an interest rate, a commodity, or an equity.

The attributes of financial instruments are discussed here.

General attributes

This includes the general identification information and essential features associated with every trade. Typical attributes include a unique ID, an instrument name, a type, a status, a trade date, and a time.

Economics

Economics are features related to the value of the trade; for example, the buy or sell value, ticker, exchange, price, and quantity.

Sales

Sales refers to the sales characteristic - related details, such as the name of the salesperson. It is just an informational field, usually without any impact on the trade lifecycle.

Counterparty

The counterparty is an essential component of a trade as it shows the other side (the other party involved in the trade) of the trade, and it is required to settle the trade successfully. The normal attributes include the counterparty name, address, payment type, any reference IDs, settlement date, and delivery type.

Trade lifecycle

A general trade lifecycle includes the various stages from order placement to execution and settlement. This lifecycle is described step-by-step as follows:

- Pre-execution: An order is placed at this stage.

- Execution and booking: When the order is matched and executed, it is converted into a trade. At this stage, the contract between counterparties is matured.

- Confirmation: This is where both counterparties agree to the particulars of the trade.

- Post-booking: This stage is concerned with various scrutiny and verification processes required to ascertain the correctness of the trade.

- Settlement: This is the most vital part of the trade life cycle. At this stage, the trade is final.

- End-of-day processing: End-of-day processes include report generation, profit and loss calculations, and various risk calculations.

This life cycle is also shown in the following image:

Figure 18.1: Trade life cycle

In all the aforementioned processes, many people and business functions are involved. Most commonly, these functions are divided into functions such as front office, middle office, and back office.

In the following section, we introduce some terminology that's relevant to crimes that occur in the financial industry.

Order anticipators

Order anticipators try to make a profit before other traders can carry out trading. This is based on the anticipation of a trader who knows how the activities of other trades will affect prices. Frontrunners, sentiment-oriented technical traders, and squeezers are some examples of order anticipators.

Market manipulation

Market manipulation is strictly illegal in many countries. Fraudulent traders can spread false information in the market, which can then result in price movements, enabling illegal profiteering. Usually, manipulative market conduct is trade-based, and it includes generalized and time-specific manipulations. Actions that can create an artificial shortage of stock, an impression of false activity, and price manipulation to gain criminal benefits are included in this category.

Both of these terms are relevant to financial crime. However, it is possible to develop blockchain-based systems that can thwart market abuse due to its transparency and security properties.

Now that we have gone through some basic financial and market concepts, let's dive into decentralized finance.

DeFi

DeFi stands for decentralized finance, which is the largest application of tokenization. It is an ecosystem that has emerged as a result of the development of many different types of financial applications built on top of blockchains. With blockchains being decentralized and the applications being related to finance, the term emerged as decentralized finance, or DeFi for short.

DeFi is an umbrella term used to describe a financial services ecosystem that is built on top of blockchains. Centralized finance, or CeFi for short, is a term now used to refer to the traditional financial services industry, which is centralized in nature, while DeFi is a movement to decentralize the traditional centralized financial services industry.

We covered the concept of decentralization in Chapter 2, Decentralization, which readers can refer to for review.

Tokenization plays a vital role in the DeFi ecosystem, which is the largest use of tokenization. DeFi is a vast subject with many different applications, protocols, assets, tokens, blockchains, and smart contracts.

The DeFi ecosystem is the fastest-growing infrastructure running on different blockchains. Most DeFi applications are running on Ethereum, but some are also running on EOS. The range of DeFi DApps includes, but is not limited to lending and borrowing, trading, asset management, insurance, tokenization, and prediction markets. All these decentralized applications, along with their smart contracts and infrastructure, make up the DeFi ecosystem.

In DeFi and in blockchain-based trading systems in general, the trading of tokens is the prime activity. We briefly describe this next.

Trading tokens

Tokens can be traded on exchanges. With the advent of DeFi, now decentralized exchanges are also emerging, abbreviated as DEX.

DEXs are decentralized and therefore require no central authority or intermediary to facilitate trading. Traders can trade with each other directly on a peer-to-peer basis. One of the advantages of DEXs due to decentralization is that traders are not required to transfer their funds to an intermediary; instead, funds can remain under their own control and they can directly trade with another counterparty without the involvement of an intermediary.

While the entry barrier to DEXs is low due to a lack of traditional know your customer (KYC) requirements, this also makes them risky for investors because if somehow the DEX is hacked, then there is no protection against loss of funds.

KYC is a standard due diligence practice in the financial services industry that ensures that the customer is legitimate and genuine.

Some examples of DEXs are Uniswap, Bancor, WavesDEX, and IDEX. This ecosystem is growing at a very fast pace and is only expected to grow further.

With all this activity in token trading, some malpractices are expected. In order to control these and ensure a fair and just system, regulation, which we'll discuss next, plays a vital role.

Regulation

Regulation of tokens is an important subject. In the last few years, especially after a wave of scam ICOs, there is genuine interest in protecting the investor. Due to this, many regulatory authorities have issued warnings and guidelines around ICOs, and some have also issued directives mandating the process of issuing and managing tokens. We will cover regulation in a bit more detail in Chapter 21, Scalability and Other Challenges.

Now after all this theoretical background, let's see how a token can be built on Ethereum. We will build our own ERC-20 - compliant token, called My ERC20 Token, or MET for short.

Building an ERC-20 token

In this section, we will build an ERC-20 token. In previous chapters, we saw several ways of developing smart contracts, including writing smart contracts in Visual Studio Code and compiling them and then deploying them on a blockchain network. We also used the Remix IDE, Truffle, and MetaMask to experiment with various way of developing and deploying smart contracts. In this section, we will use a quick method to develop, test, and deploy our smart contract on a Goerli test network. We will not use Truffle or Visual Studio Code in this example as we have seen this method before; we are going to explore a quicker method to build and deploy our contract.

In this example, we will see how quickly and easily we can build and deploy our own token on the Ethereum blockchain network.

Pre requisites

We will use the following components in our example:

- Remix IDE, available at http://remix.ethereum.org. Note that in the following example, the user interface and steps required might be slightly different depending on the stage of development. This is because Remix IDE is under heavy development, and new features are being added to it at tremendous pace—as such, some changes are expected in the user interface too. However, the fundamentals are not expected to change, and no major changes are expected in the user interface.

- MetaMask, which we installed in Chapter 12, Further Ethereum. We used it again in Chapter 16, Serenity, to deploy a contract on a Goerli test network, and we will use the same network in this example. You can create a new account if required.

Building the Solidity contract

Now let's start writing our code. First, we explore what the ERC-20 interface looks like, and then we will start writing our smart contract step by step in the Remix IDE.

The ERC-20 interface defines a number of functions and events that must be present in an ERC-20-compliant smart contract. Some more rules that must be present in an ERC-20-compliant token are listed here:

totalSupply: This function returns the number of the total supply of tokens:function totalSupply() public view returns (uint256)balanceOf: This function returns the balance of the token owner:function balanceOf(address _owner) public view returns (uint56 balance)transfer: This function takes the address of the recipient and a specified value as a number of tokens and transfers the amount to the address specified:function transfer(address _to, uint256 _value) public returns (bool success)transferFrom: This function takes_from(sender's address),_to(recipient's address), and_value(amount) as parameters and returnstrueorfalse. It is used to transfer funds from one account to another:function transferFrom(address _from, address _to, uint256 _value) public returns (bool success)approve: This function takes_spender(recipient) and_value(number of tokens) as parameters and returns a Boolean,trueorfalse, as a result. It is used to authorize the spender's address to make transfers on behalf of the token owner up to the approved amount (_value):function approve(address _spender, uint256 _value) public returns (bool success)allowance: This function takes the address of the token owner and the spender's address and returns the remaining number of tokens that the spender has approval to withdraw from the token owner:function allowance(address _owner, address _spender) public view returns (uint256 remaining)

There are three optional functions, which are listed as follows:

name: This function returns the name of the token as astring. It is defined in code as follows:function name() public view returns (string)symbol: This returns the symbol of the token as astring. It is defined as follows:function symbol() public view returns (string)decimals: This function returns the number of decimals that the token uses as an integer. It is defined as follows:function decimals() public view returns (uint8)

Finally, there are two events that must be present in an ERC-20-compliant token:

Transfer: This event must trigger when tokens are transferred, including any zero-value transfers. The event is defined as follows:event Transfer(address indexed _from, address indexed _to, uint256 _value)Approval: This event must trigger when a successful call is made to theapprovefunction. The event is defined as follows:event Approval(address indexed _owner, address indexed _spender, uint256 _value)

Now let's have a look at the source code of our ERC-20 token. This is written in Solidity, which we are familiar with and have explored in detail in Chapter 14, Development Tools and Frameworks.

Solidity contract source code

The source code for our ERC-20 token is as follows:

pragma solidity ^0.6.1;

contract MyERC20Token {

mapping (address => uint256) _balances;

mapping (address => mapping(address => uint256)) _allowed;

string public name = "My ERC20 Token";

string public symbol = "MET";

uint8 public decimals = 0;

uint256 private _totalSupply = 100;

event Transfer(address indexed _from, address indexed _to, uint256 _value);

event Approval(address indexed _owner, address indexed _spender, uint256 _value);

constructor() public {

_balances[msg.sender] = _totalSupply;

emit Transfer(address(0), msg.sender, _totalSupply);

}

function totalSupply() public view returns (uint) {

return _totalSupply - _balances[address(0)];

}

function balanceOf(address _owner) public view returns (uint balance) {

return _balances[_owner];

}

function allowance(address _owner, address _spender) public view returns (uint remaining) {

return _allowed[_owner][_spender];

}

function transfer(address _to, uint256 _value) public returns (bool success) {

require(_balances[msg.sender] >= _value,"value exceeds senders balance");

_balances[msg.sender] -= _value;

_balances[_to] += _value;

emit Transfer(msg.sender, _to, _value);

return true;

}

function approve(address _spender, uint256 _value) public returns (bool success)

{

_allowed[msg.sender][_spender] = _value;

emit Approval(msg.sender, _spender, _value);

return true;

}

function transferfrom(address _from, address _to, uint256 _value) public returns (bool success)

{

require(_value <= _balances[_from],"Not enough balance");

require(_value <= _allowed[_from][msg.sender],"Not enough allowance");

_balances[_from] -= _value;

_balances[_to] += _value;

_allowed[_from][msg.sender] -= _value;

emit Transfer(_from, _to, _value);

return true;

}

}

Let's explain this code step by step, before writing it into the Remix IDE.

First is the Solidity compiler and language version:

pragma solidity ^0.6.1;

The first line of the code specifies the compiler version using the pragma directive for which our program is written.

Then we create the contract object:

contract MyERC20Token {

After this, the contract object is defined with the name MyERC20Token.

Then we have the mappings:

mapping (address => uint256) _balances;

mapping (address => mapping(address => uint256)) _allowed;

These are the two mappings used in the ERC-20 smart contract. The first one is for keeping balances and the other one is used for allowances.

These are the state variables:

string public name = "My ERC20 Token";

string public symbol = "MET";

uint8 public decimals = 0;

uint256 private _totalSupply = 100;

They describe the name, symbol, and decimal precision points and the total supply of our token.

This is the Transfer event:

event Transfer(address indexed _from, address indexed _to, uint256 _value);

It has three parameters: from, to, and value. from represents the address from which the tokens are coming, to is the account to which tokens are being transferred, and value is the number of tokens.

This is the Approval event:

event Approval(address indexed _owner, address indexed _spender, uint256 _value);

This has three parameters: owner address, recipient address, and value. The indexed keyword allows us to search for a specific log item instead of searching through all logs. It enables log filtration to search and extract only the required data instead of returning all logs.

This is the constructor that is executed when the contract is created:

constructor() public {

_balances[msg.sender] = _totalSupply;

emit Transfer(address(0), msg.sender, _totalSupply);

}

It is optional in Solidity and is used to run initialization code. In our example, the initialization code contains the statements to transfer the entire balance, _totalSupply, to the creator of the smart contract; in our case, it is the sender account. It also then emits the Transfer event, indicating that the transfer has taken place from address(0) to msg.sender (our contract creator) and _totalSupply, which is 100 in our case, just to keep things simple.

This is the totalSupply function:

function totalSupply() public view returns (uint) {

return _totalSupply - _balances[address(0)];

}

This function returns the total amount of tokens after deducting it from the balance of the account.

This is the balanceOf function:

function balanceOf(address _owner) public view returns (uint balance) {

return _balances[_owner];

}

The balanceOf function returns the balance of the token owner.

The allowance function is as follows:

function allowance(address _owner, address _spender) public view returns (uint remaining) {

return _allowed[_owner][_spender];

}

The allowance function returns the total remainder of the tokens.

This is the transfer function, which returns true or false depending on the result of the execution:

function transfer(address _to, uint256 _value) public returns (bool success) {

require(_balances[msg.sender] >= _value,"value exceeds senders balance");

_balances[msg.sender] -= _value;

_balances[_to] += _value;

emit Transfer(msg.sender, _to, _value);

return true;

}

The require convenience function is used to check for certain conditions and throw an exception if the conditions are not met. In our example, this checks whether the value exceeds the sender's balance, and if it does, an error message will be generated stating that value exceeds senders balance. If this check passes, the transfer occurs, and after emitting the Transfer event, the function returns true, indicating the successful transfer of tokens.

This is the approve function, which returns true or false depending on the result of the execution of the function:

function approve(address _spender, uint256 _value) public returns (bool success)

{

_allowed[msg.sender][_spender] = _value;

emit Approval(msg.sender, _spender, _value);

return true;

}

This function takes _spender (the user) and _value (number of tokens) as arguments and serves as a mechanism to provide approval to the user to acquire the allowed number of tokens from our ERC-20 contract.

This function is the transferFrom function, which can be used to automate the transfer of tokens from one address to another:

function transferfrom(address _from, address _to, uint256 _value) public returns (bool success)

{

require(_value <= _balances[_from],"Not enough balance");

require(_value <= _allowed[_from][msg.sender],"Not enough allowance");

_balances[_from] -= _value;

_balances[_to] += _value;

_allowed[_from][msg.sender] -= _value;

emit Transfer(_from, _to, _value);

return true;

}

It takes three parameters: _from, _to, and _value. It returns true or false depending upon the execution of the function. First, with the require functions, the balance and allowances are checked to ensure that enough balance and allowance is available. After that, the transfer occurs, and eventually the Transfer event is emitted, followed by a true Boolean value returned by the function indicating the successful transfer.

Now that we understand what our source code does, the next step is to write it in the Remix IDE and deploy it.

Deploying the contract on the Remix JavaScript virtual machine

In this step, we simply take the source code and write or simply paste it in the Remix IDE. Once pasted, this code will look like this:

Figure 18.2: Remix IDE showing erc20example.sol

To achieve this, begin by opening the Remix IDE. When the Remix IDE opens up, it will show an interface similar to the following:

Figure 18.3: Remix IDE environments

Select SOLIDITY under Environments, as we are going to write smart contracts using the Solidity smart contract language.

After selecting the Solidity environment, create a new file by choosing the FILE EXPLORERS option from the list of icons on the left-hand side and add a new file by clicking the + sign:

Figure 18.4: Remix IDE file explorer

Create a new file in the Remix IDE named erc20example.sol.

When we have created the new file, it will look like the following screenshot:

Figure 18.5: New file in Solidity

Now simply write the source code in the IDE, or paste it directly.

The next step is to compile the source code. To do this, click on Compile erc20example.sol. Optionally, Auto compile can also be selected under COMPILER CONFIGURATION, which will compile the code automatically as soon as it is written into the IDE:

Figure 18.6: Solidity compiler in Remix

Once compiled successfully, it is ready to be deployed. First, we will deploy it on JavaScript VM available with the Remix IDE to ensure that everything works. Once we have tested that it can be deployed correctly and works as per our expectations, we could deploy it on the mainnet using MetaMask. In our example, however, we will deploy it on the Goerli testnet using MetaMask.

To deploy on the mainnet, simply choose mainnet from MetaMask after ensuring that enough funds are available to deploy it on mainnet.

Remember that we have some ether left from our exercise in Chapter 16, Serenity, and have a test account on the Goerli network. We can use the same account for this example, or create a new account and fund it using the process in Chapter 16, Serenity. The aim of this exercise is to understand how MetaMask can be used to deploy our new token smart contract on an Ethereum network. We will also see how we can import ERC-20 tokens in MetaMask and use it to transfer funds from one account to another.

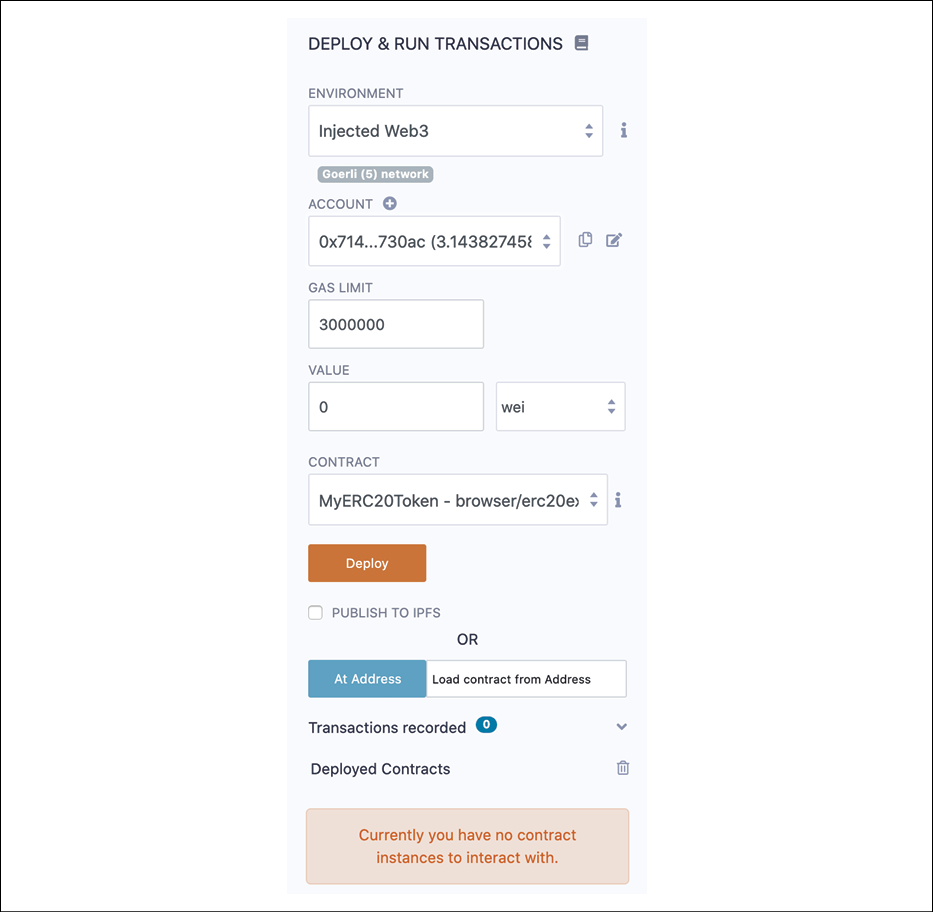

After compilation, we deploy the smart contract using the Deploy & Run Transactions interface available within the Remix IDE. This is shown in the following screenshot:

Figure 18.7: Deploying and running transactions in Remix

Make sure the environment JavaScript VM is selected and an account is selected from which to deploy, and then select Deploy.

Once it's deployed, we will see an output similar to the following screenshot, where the contract will become available under Deployed Contracts and, in the logs, we can see relevant details regarding the deployment of the contract:

Figure 18.8: Contract creation in Remix

Most importantly, we can see in the logs that when the contract is created, the first event emitted is 'Transfer'. Here, we can see that all 100 tokens have been transferred to the owner account, 0x87C8E1937825c045a63D87e9b0B9c639ca99965b:

[

{

"from": "0x87c8e1937825c045a63d87e9b0b9c639ca99965b",

"topic": "0xddf252ad1be2c89b69c2b068fc378daa952ba7f163c4a11628f55a4df523b3ef",

"event": "Transfer",

"args": {

"0": "0x0000000000000000000000000000000000000000",

"1": "0x24a6ccd8C71775Da3EC4C40fD0C69bB51d4236B6",

"2": "100",

"_from": "0x0000000000000000000000000000000000000000",

"_to": "0x24a6ccd8C71775Da3EC4C40fD0C69bB51d4236B6",

"_value": "100",

"length": 3

}

}

]

Once it's deployed, we will see under Deployed Contracts all the functions exposed by the contract in the Remix IDE:

Figure 18.9: Exposed functions in Remix for our contract

We can test the functionality of our contract using this interface. For example, calling totalSupply shows a value of 100, which indicates the number of tokens, and calling symbol shows the string MET, our token's symbol.

At this point, our contract works and we have tested it locally. Now we can deploy it onto the Goerli testnet. We will use MetaMask for this purpose.

In the Remix IDE, under DEPLOY & RUN TRANSACTIONS, select the Injected Web3 option, as shown in the following screenshot:

Figure 18.10: Remix Inject Web3

This is the execution environment that is provided by enabling web3 within the browser using the MetaMask plugin.

First, confirm that MetaMask is running and connected to the Goerli test network. This should be easy to check, as we used this same network in Chapter 16, Serenity.

If everything is working in MetaMask, it should display a screen similar to the following screenshot. Note that you may have to log in again to MetaMask. Once you're logged in, select the Goerli network and an account that has some ether in it:

Figure 18.11: Goerli test network in MetaMask

In the Remix IDE, choose Injected Web3 in the ENVIRONMENT field under DEPLOY & RUN TRANSACTIONS. This is shown in the following screenshot:

Figure 18.12: DEPLOY & RUN TRANSACTIONS in MetaMask

Note that in the screenshot, the Goerli (5) network is selected. It also shows the account that we have set up in MetaMask. Now we are all set to deploy this on the Goerli test network.

Click Deploy, which will open the MetaMask window to confirm the transaction, as shown here:

Figure 18.13: Confirm transaction

Click Confirm, and the contract will be deployed. We can see this in the history in MetaMask, as shown here:

Figure 18.14: My ERC token contract deployment using MetaMask

Similar to the tests that we did earlier in this example when we deployed our contract on the JavaScript VM, we can invoke different functions exposed by our new ERC-20 token directly from the Remix IDE, as shown here:

Figure 18.15: Deployed ERC-20 contract in Remix

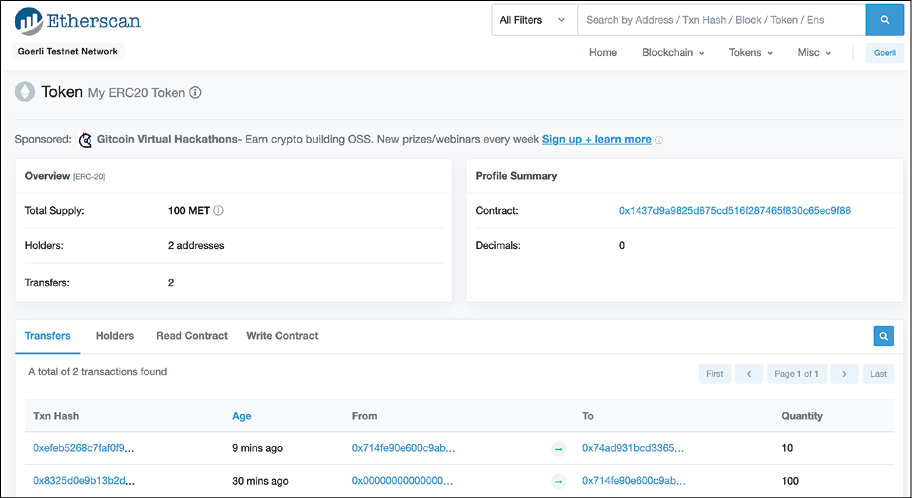

We can also see our token on the Etherscan token tracker. This is shown by accessing the following link:

https://goerli.etherscan.io/token/0x1437d9a9825d875cd516f287465f830c65ec9f86

The Etherscan page can also be seen in the following screenshot:

Figure 18.16: Etherscan token view

So here we have it, our own MET token deployed on the Goerli test network.

Now, if desired, we could deploy this to the Ethereum mainnet, provided that we have some ether available. We can perform exactly the same steps to deploy it, with the only difference being that in MetaMask, we will choose the Ethereum mainnet as the network.

Adding tokens in MetaMask

Once we have deployed our contract and our ERC-20 token is now on the blockchain (so to speak), unless we are able to view it and perform operations on it, the token on its own is of no real use.

To perform operations on the token, we can manually create commands using the Web3.js sendRawTransaction method, and use the JavaScript and command-line geth console to interact with it. Alternatively, we can use an easier option and simply add the token to a wallet. Wallets abstract away the complexities associated with transaction creation and management and provide an easy-to-use interface to perform transfers and similar tasks. MetaMask can serve as a wallet for tokens and provides an interface to add tokens. In this section, we'll see how we can add our MET token to MetaMask and perform some operations on it.

Open MetaMask and find the Add Token option, either on the main user interface, or open the account menu and it will display the current account, as shown here:

Figure 18.17: Adding a new token in Remix

Click on Add Token and select Custom Token.

Enter the contract address, 0x1437d9a9825d875cd516f287465f830c65ec9f86, which will automatically display the Token Symbol and the decimal points, as shown in the following screenshot:

Figure 18.18: Custom token in MetaMask

Press Next, and then confirm that you want to add these tokens, as shown here:

Figure 18.19: Adding a token in MetaMask

Now we have 100 MET in our MetaMask wallet:

Figure 18.20: METs in MetaMask

Now let's send 10 MET to another account on the Goerli network. Click on Send, then enter the target account's details:

Figure 18.21: Send tokens

Figure 18.22: Remix confirmation

Click Confirm, and the transaction will be processed:

Figure 18.23: Tokens sent

We can see this transfer on Etherscan here:

https://goerli.etherscan.io/tx/0xefeb5268c7faf0f9ccf2fe32213b279a69db728c0f1fbdccc0a0a8f2e5afd1ad

This page is also shown in the following screenshot

Figure 18.24: Etherscan view

Now, coming back to the Remix IDE, we can now see that our balance has been reduced by 10 MET:

Figure 18.25: Deployed contracts in Remix

Similarly, we can check the balance of the target account to which we transferred 10 MET, which is now 10 MET:

Figure 18.26: Balance of remix

We can see all the transfers of our ERC-20 token, MET, here on Etherscan:

https://goerli.etherscan.io/token/0x1437d9a9825d875cd516f287465f830c65ec9f86

This page can also be viewed in the following screenshot:

Figure 18.27: Etherscan view of token transfers

With this, we have covered how to create an ERC-20 token from scratch and deploy it on the Ethereum blockchain.

Let's now have a look at some of the novel concepts that are emerging due to the remarkable success of tokenization and the blockchain ecosystem in general.

Emerging concepts

With the advent of blockchain and tokenization, several new concepts have emerged over the last few years. We will introduce some of them now.

Tokenomics/token economics

Tokenomics or token economics is an emerging discipline that is concerned with the study of economic activity, economic models, and the impact of tokenization. It deals with the goods and assets that have been tokenized and the entities that are involved in the entire process of token issuance, sale, purchase, and investment.

You might have heard another term, cryptoeconomics, which is a related but slightly different term. Cryptoeconomics is concerned with the same topics but it is a superset of tokenomics. In other words, tokenomics is a subset of cryptoeconomics. Tokenomics is only concerned with tokens and tokenization ecosystems, but does not include the broader blockchain networks, protocols, and cryptocurrencies.

With the use of the proof of work (PoW) mechanism in Bitcoin, it was demonstrated for the first time that computer protocols can be designed in such a way that attacking a system does not result in achieving an uneven advantage or commercial benefit. This concept then further matured into what we call today cryptoeconomics. This can also be understood as a combination of economics, game theory, and cryptography.

Token engineering

Token engineering is an emerging concept that is looking at tokenization from an engineering perspective and is striving to apply the same rigor, systems thinking, and mathematical foundations to tokenization and blockchain in general that a usual engineering discipline has. This subject is still in its infancy; however, good progress has been made toward the development of this new discipline.

More information on token engineering can be found at https://tokenengineeringcommunity.github.io/website/.

Token taxonomy

There is a lack of consistent taxonomy for tokens. As such, there are no clear standards defined on how to design and manage tokens. Also, it is not clear how to reuse an already existing and working token design, or if any exist at all.

Therefore, there is a need for a classification system that categorizes all different types of tokens according to different attributes they have. There is also no universal classification of different attributes of tokens such as type, value, and economic attributes. Such a system would benefit the tokenization ecosystem tremendously.

Don't confuse this with the ERC standards we explained earlier; those are development standards and they are certainly useful. But they are limited in scope and are not the universal classification of tokens.

Some work on this was started by Interwork Alliance by producing a Token Taxonomy Framework (TTF). More details on this work can be found on their website: https://interwork.org.

Summary

In this chapter, we covered tokenization and relevant concepts and standards. We also covered different types of tokens and related token standards. Moreover, a primer on trading and finance was also provided to familiarize readers with some standard finance concepts, which help us to understand the DeFi ecosystem too, as most DeFi terminology is borrowed from traditional finance.

Also, we introduced a practical example on how to create our own ERC-20-compliant token using the Ethereum platform. Finally, we introduced some emerging ideas related to tokenization.

In the next chapter, we will explore how blockchain can be used outside of the context of its original usage, that is, cryptocurrencies. We will cover various use cases, and consider in particular detail the use of blockchain in IoT.