END OF CHAPTER MATERIAL

CONCEPT CHECK

1. Which of the following statements about payroll and fixed asset processes is true?

1. Which of the following statements about payroll and fixed asset processes is true? - Both have only routine processes.

- Both have only nonroutine processes.

- Both have routine and nonroutine processes.

- Payroll has only routine processes, while fixed asset has only nonroutine

- 2. For a given pay period, the complete listing of paychecks for the pay period is a

- payroll register

- payroll ledger

- payroll journal

- paymaster

- 3. A payroll voucher

- authorizes an employee paycheck to be written

- authorizes the transfer of cash from a main operating account to a payroll account

- authorizes the transfer of cash from a payroll account to a main operating account

- authorizes the paymaster to distribute paychecks

- 4. For proper segregation of duties, the department that should authorize new employees for payroll would be

- payroll

- human resources

- cash disbursement

- general ledger

- 5. Which of the following is not an independent check within payroll processes?

- Time sheets are reconciled with production records.

- Time sheets are reconciled with the payroll register.

- Paychecks are prepared on prenumbered checks.

- The payroll register is reconciled with the general ledger.

- 6. An integrated IT system of payroll and human resources may have extra risks above those of a manual system. Passwords and access logs are controls that should be used in these integrated systems to lessen the risk of

- hardware failures

- erroneous data input

- payroll data that does not reconcile to time cards

- unauthorized access to payroll data

- 7. Internal control problems would be likely to result if a company's payroll department supervisor was also responsible for

- reviewing authorization forms for new employees

- comparing the payroll register with the batch transmittal data

- authorizing changes in employee pay rates

- hiring subordinates to work in the payroll department

- 8. Which of the following procedures would be most useful in determining the effectiveness of a company's internal controls regarding the existence or occurrence of payroll transactions?

- 9. In meeting the control objective of the safeguarding of assets, which departments should be responsible for distribution of paychecks and custody of unclaimed paychecks, respectively?

- 10. A company's internal controls policies may mandate the distribution of paychecks by an independent paymaster in order to determine that

- payroll deductions are properly authorized and computed

- pay rates are properly authorized and separate from the operating function

- each employee's paycheck is supported by an approved time sheet

- employees included in the period's payroll register actually exist and are currently employed

- 11. The purpose of segregating the duties of hiring personnel and distributing payroll checks is to separate the

- authorization of transactions from the custody of related assets

- operational responsibility from the recordkeeping responsibility

- human resources function from the controllership function

- administrative controls from the internal accounting controls

- 12. Which of the following departments or positions most likely would approve changes in pay rates and deductions from employee salaries?

- Human resources

- Treasurer

- Controller

- Payroll

- 13. The purchase of fixed assets is likely to require different authorization processes than the purchase of inventory. Which of the following is not likely to be part of the authorization of fixed assets?

- Specific authorization

- Inclusion in the capital budget

- An investment analysis or feasibility analysis of the purchase

- Approval of the depreciation schedule

- 14. Which of the following is not a part of “adequate documents and records” for fixed assets?

- Fixed asset journal

- Fixed asset subsidiary ledger

- Purchase order

- Fixed asset tags

- 15. Which of the following questions would be least likely to appear on an internal control questionnaire regarding the initiation and execution of new property, plant, and equipment purchases?

- Are requests for repairs approved by someone higher than the department initiating the request?

- Are prenumbered purchase orders used and accounted for?

- Are purchase requisitions reviewed for consideration of soliciting competitive bids?

- Is access to the assets restricted and monitored?

- 16. Which of the following reviews would be most likely to indicate that a company's property, plant, and equipment accounts are not understated?

- Review of the company's repairs and maintenance expense accounts

- Review of supporting documentation for recent equipment purchases

- Review and recomputation of the company's depreciation expense accounts

- Review of the company's miscellaneous revenue account.

- 17. Which of the following is not an advantage of fixed asset software systems when compared with spreadsheets?

- Better ability to handle nonfinancial data such as asset location

- Easier to apply different depreciation policies to different assets

- Manual processes to link to the general ledger

- Expanded opportunities for customized reporting

- 18. The term “ghost employee” means that

- hours worked has been exaggerated by an employee

- false sales have been claimed to boost commission earned

- overtime hours have been inflated

- someone who does not work for the company receives a paycheck

DISCUSSION QUESTIONS

- 19. (SO 1) Sales and inventory purchases are routine processes that occur nearly every day in a business. How are these routine processes different from payroll or fixed asset processes?

- 20. (SO 1) Even though payroll and fixed asset processes may not be as routine as revenue processes, why are they just as important?

- 21. (SO 2) Why do you think management should specifically approve all employees hired?

- 22. (SO 2) Why is it important that the human resources department maintain records authorizing the various deductions from an employee's paycheck?

- 23. (SO 2) Explain why an employee's individual record is accessed frequently, but changed relatively infrequently.

- 24. (SO 2) Explain two things that should occur to ensure that hours worked on a time card are accurate and complete.

- 25. (SO 2) Explain the reasons for an organization having a separate bank account established for payroll.

- 26. (SO 3) What is the purpose of supervisory review of employee time cards?

- 27. (SO 3) Why is it important to use an independent paymaster to distribute paychecks?

- 28. (SO 3) Why do payroll processes result in sensitive information, and what is the sensitive information?

- 29. (SO 4) Why is batch processing well suited to payroll processes?

- 30. (SO 4) What are the advantages of automated time keeping such as bar code readers, or ID badges that are swiped through a reader?

- 31. (SO 4) What are the advantages of outsourcing payroll?

- 32. (SO 5) Fixed assets are purchased and retired frequently. Given this frequent change, why are clear accounting records of fixed assets necessary?

- 33. (SO 5) Why is it important to conduct an investment analysis prior to the purchase of fixed assets?

- 34. (SO 5) Explain why categorizing fixed asset expenditures as expenses or capital assets is important.

- 35. (SO 5) What are some of the practical characteristics of fixed assets that complicate the calculation of depreciation?

- 36. (SO 6) What is different about the nature of fixed asset purchasing that makes authorization controls important?

- 37. (SO 6) Explain the necessity of supervision over fixed assets.

- 38. (SO 6) Why are some fixed assets susceptible to theft?

- 39. (SO 7) Explain why a real-time update of fixed asset records might be preferable to batch processing of fixed asset changes.

- 40. (SO 7) Why is the beginning of a fiscal year the best time to implement a fixed asset software system?

- 41. (SO 7) What negative things might occur if fixed asset software systems lacked appropriate access controls?

- 42. (SO 8) Why might a supervisor collude with an employee to falsify time cards?

- 43. (SO 8) How does the misclassification of fixed asset expenditures result in misstatement of financial statements?

BRIEF EXERCISES

- 44. (SO 2) Describe the type of information that a human resources department should maintain for each employee.

- 45. (SO 2) The calculation of gross and net pay can be a complicated process. Explain the items that complicate payroll calculations.

- 46. (SO 3) Explain how duties are segregated in payroll. Specifically, who or which departments conduct the authorization, timekeeping, recording, and custody functions?

- 47. (SO 3) Explain the various reconciliation procedures that should occur in payroll.

- 48. (SO 4) Explain the ways in which electronic transfer of funds can improve payroll processes.

- 49. (SO 5) Explain the kinds of information that must be maintained in fixed asset records during the asset continuance phase.

- 50. (SO 6) The authorization to purchase fixed assets should include investment analysis. Explain the two parts of investment analysis.

- 51. (SO 8) Explain the types of unethical behavior that may occur in the fixed assets area.

PROBLEMS

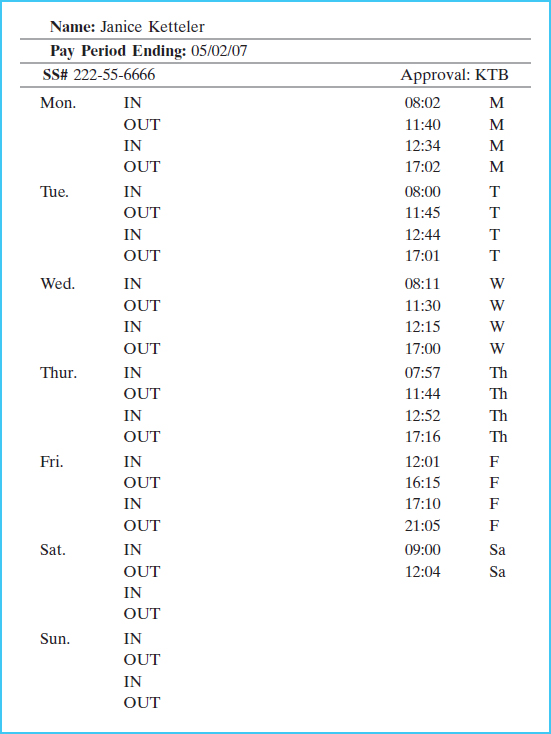

52. (SO 2) Following is a time sheet completed by an hourly wage earner at Halfrid, Inc.:

52. (SO 2) Following is a time sheet completed by an hourly wage earner at Halfrid, Inc.:

Use Microsoft Excel to perform the following tasks:

- Design an appropriate format for a data entry screen that could be used in the payroll department to enter information from this time sheet in the company's payroll software program.

- Prepare a payroll journal with the column headings shown in the next table. Enter the relevant information from the preceding time sheet onto this journal and calculate gross pay, federal withholdings, and net pay. Use two lines for this employee, and assume that the pay rate is $19.75 per hour, with time-and-a-half for overtime. (Overtime applies to any time worked over 40 hours within one week.) Use the following withholding rates: FICA (Social Security)—6.2 percent of gross pay; Medicare—1.45 percent of gross pay; federal income taxes—20 percent. Assume no additional withholdings.

- 53. (SO 2) The textbook website has a Microsoft Excel spreadsheet titled payroll_problem.xls. This spreadsheet is used by Naltner Company to calculate its biweekly payroll. Using the information in that spreadsheet, calculate all details for the February 22, 2013, payroll. Hours worked by each employee are contained in the first worksheet. The following four worksheets contain details for each of the three employees and a total for the three employees. The sixth and last worksheet contains federal tax withholding tables to calculate federal tax to withhold. Calculate the gross pay and deductions for all three employees.

- 54. (SO 5) The textbook website has a Microsoft Excel spreadsheet titled fixed_asset.xls. The spreadsheet represents a fixed asset subsidiary ledger for Brozzos Corporation. On July 3, 2013, Brozzos purchased for the office a multifunction printer/fax/copier from Brereton Office Supplies for $200. The machine has no salvage value and a four-year life. Add a new ledger record for this machine and calculate and record the 2013 depreciation expense for all fixed assets. Brozzos uses straight-line depreciation with a half-year convention.

- 55. (SO 6) Explain the process of approval of purchases for fixed assets. How does this process differ from that of purchasing raw materials?

- 56. (SO 3) Using an Internet search engine, search for the phrase “biometric time clock.” (Be sure to include the quotation marks.) From your search results, describe a biometric time recording system and its advantages.

- 57. (SO 7) Using an Internet search engine, search for the phrase “fixed asset software.” (Be sure to include the quotation marks.) Examine the results to find companies that sell fixed asset software. List and explain some of the features of fixed asset software that these companies offer as selling points for their software.

58. (SO 8) Read the article at this link: http://www.itnews.com.au/News/121683.in-car-spy-units-to-catch-misuse.aspx. Describe any ethics considerations in using such technology. Consider both the company and employee perspectives. Also discuss whether you believe the use of this device could be an internal control for the company.

58. (SO 8) Read the article at this link: http://www.itnews.com.au/News/121683.in-car-spy-units-to-catch-misuse.aspx. Describe any ethics considerations in using such technology. Consider both the company and employee perspectives. Also discuss whether you believe the use of this device could be an internal control for the company.- 59. (SO 8) Using an Internet search engine, search for the terms “Patti Dale” and “theft.” (Be sure to include the quotation marks around the name.) Explain the unethical behavior that occurred. Also, explain any internal controls that you believe were missing or not followed in this case.

CASES

- 60. Flozner Company is a small manufacturing firm with 60 employees in seven departments. When the need arises for new workers in the plant, the departmental manager interviews applicants and hires on the basis of those interviews. The manager has each new employee complete a withholding form. The manager then writes the rate of pay on the W-4 and forwards it to payroll.

When workers arrive for their shift, they pull their time cards from a holder near the door and keep the time card with them during the day to complete the start and end times of their work day. On Friday, the time cards are removed from the holder and taken to payroll by any employee who is not busy that morning. If there were any pay rate changes for the payroll period due to raises or promotions, the manager calls the payroll department to inform payroll of these rate changes.

Using the rate changes and the time cards, the payroll department prepares the checks from the regular bank account of the Flozner Company. The manager of the payroll department signs the checks, and the checks are then forwarded to each department manager for distribution to employees.

Required:

Describe any improvements you would suggest to strengthen the payroll internal controls at Flozner.

- 61. Alomna Industries has payroll processes as described in the following paragraphs:

When a new employee is hired, the human resources department completes a personnel action form and forwards it to the payroll department. The form contains information such as pay rate, number of exemptions for tax purposes, and the type and amount of payroll deductions. When an employee is terminated or voluntarily separates from Alomna, the human resources department completes a personnel action form to indicate separation and forwards it to the payroll department.

Each employee in the production department maintains his own time card weekly. Employees fill out their time cards in ink each day, and at the end of the week, the time cards are forwarded to the payroll department. Employees in the payroll department use the time cards and employee records to prepare a weekly paycheck for each employee who has turned in a time card. A copy of the payroll checks is forwarded to the accounts payable department, and the original payroll checks are forwarded to the cash disbursements department to be signed. The payroll department updates the payroll subsidiary ledger. After the paychecks are signed, they are given to department supervisors to distribute. Any unclaimed checks are returned to the payroll department.

Required:

- Prepare a process map of the payroll processes at Alomna.

- Identify both internal control strengths and internal control weaknesses of the payroll processes.

- For any internal control weaknesses, describe suggested improvements.

- 62. Breightner Enterprises is a midsize manufacturing company with 120 employees and approximately 45 million dollars in sales. Management has established a set of processes to purchase fixed assets, described in the following paragraphs:

When a user department determines that it may be necessary to purchase a new fixed asset, the departmental manager prepares an asset request form. When completing the form, the manager must describe the fixed asset, the advantages or efficiencies offered by the asset, and estimates of costs and benefits. The asset request form is forwarded to the director of finance. Personnel in the finance department review estimates of costs and benefits and revise these if necessary. A discounted cash flow analysis is prepared and forwarded to the vice president of operations, who reviews the asset request forms and the discounted cash flow analysis, and then interviews user department managers if she feels it is warranted. After this review, she selects assets to purchase until she has exhausted the funds in the capital budget.

When an asset purchase has been approved by the VP of operations, a buyer looks up prices and completes a purchase order. The purchase order is mailed to the vendor, and a copy is forwarded to accounts payable. The fixed asset is delivered directly to the user department so that it can be installed and used as quickly as possible. The user department completes a receiving report and forwards a copy to accounts payable. If the invoice, purchase order, and receiving report match, payment is approved and cash disbursements prepares and mails a check.

The accounts payable department updates the accounts payable subsidiary ledger and the fixed asset spreadsheet file.

Required:

- Identify any internal control strengths and weaknesses in the fixed asset processes at Breightner. Explain why each is a strength or weakness.

- For each internal control weakness, describe improvement(s) in the processes that you would recommend to address the weakness.

- 63. The Grundoll Company has the following processes related to fixed assets: When a department manager determines a need for a new fixed asset, he prepares a purchase requisition, which is forwarded to the chief financial officer. If the requested fixed asset purchase will not exceed remaining funds in the capital budget, the CFO approves the purchase and forwards the requisition to the purchasing department.

The purchasing agent assigned to purchase the fixed assets begins phoning vendors until she finds a vendor selling the requested asset. The purchase order is prepared and mailed to the vendor. Vendors are instructed to deliver the fixed asset to the requesting department.

A copy of the invoice is forwarded to the fixed asset department to record the asset details. Personnel determine the estimated life and salvage value by looking up the last similar asset purchase and using the previous estimated life and salvage value.

Required:

Describe any improvements you would suggest to strengthen the fixed asset internal controls at Grundoll.

- 64. (CMA Adapted) Rophna Co. makes automobile parts for sale to major automobile manufacturers in the United States. The following information is available regarding internal controls over machinery and equipment:

When a departmental supervisor needs a new item of machinery or equipment, he or she must initiate a purchase request. The acquisition proposal must be presented to the plant manager. If the plant manager agrees with the need, he must review the corporate budget allocation for his plant to determine the availability of funds to cover the acquisition. If the allocation is sufficient, the departmental supervisor is notified of the approval and a purchase requisition is prepared and forwarded to the purchasing department.

Upon receipt of a purchase requisition for machinery and equipment, the purchasing department researches the company records in order to locate an appropriate vendor. A purchase order is then completed and mailed to the vendor.

As soon as new machinery or equipment is received from the vendor, it is immediately sent to the department for installation. Bellott's policy is to place new assets into service as soon as possible so that the company may immediately begin to realize the economic benefits from the acquisition.

The property accounting department is responsible for maintaining property, plant, and equipment ledger control accounts. The ledger is supported by lapsing schedules that are used to compute depreciation. These lapsing schedules are organized by year of acquisition so that depreciation computations can be prepared in units that combine all assets of the same type that were acquired the same year. Standard depreciation methods, rates, and salvage values were determined ten years ago and have been used consistently since that time.

When machinery or equipment is retired or replaced, the plant manager notifies the property accounting department so that the proper adjustments can be made to the ledger and lapsing schedules. No regular reconciliation between the physical assets on hand and the accounting records has been performed.

Required:

Identify any internal control weaknesses and suggest improvements to strengthen the internal controls over machinery and equipment at Rophna.

CONTINUING CASE: ROBATELLI'S PIZZERIA

Reread the continuing case on Robatelli's Pizzeria at the end of Chapter 1. Consider the following issues that relate to Robatelli's payroll and fixed assets systems, then answer the questions pertaining to these expenditure processes:

As mentioned in the opening part of the Robatelli's Pizzeria case, there are now 53 locations throughout the greater Pittsburgh area. Each one of those restaurant locations employs a full-time store manager and varying numbers of kitchen staff, servers, and delivery staff. The kitchen staff, servers, and delivery staff vary between full-time and part-time status. There tend to be high rates of turnover, especially among the part-time staff.

Robatelli's pays its employees on a weekly basis each Friday for the week ending on the previous Saturday. Employee paychecks include withholdings for federal taxes as well as state and local taxes applicable for the employee's residence. Employees may live in one of three states and over 25 municipalities that are included in the greater Pittsburgh regional area. All payroll accounting is handled by Robatelli's at its home office.

Each restaurant must also maintain various fixed assets in order to operate. Following is a general list of fixed assets for each store:

- Furniture and store fixtures, including tables, chairs, and built-in items such as shelving, counters, and booths

- Kitchen equipment, such as refrigerators, stoves, ovens, and dishwashing machines

- Computers

Note that the number of each of these fixed assets maintained at each location varies, depending upon the size of the store. Also note that each member of the delivery staff uses his or her personal automobile (rather than a company-owned car) for customer deliveries.

In addition, the home office maintains the following types of fixed assets:

- Land and the office building

- Office furniture and fixtures

- Computers and other office equipment

- Telephone systems

Finally, fixed assets maintained at the commissary include the following:

- Fixtures, such as built-in cabinets and shelving

- Kitchen equipment

- Computers

- Delivery trucks

All fixed asset accounting is handled by Robatelli's at its home office.

Required:

- Describe how you believe an efficient and effective payroll system should be organized at Robatelli's. Include details such as the answers to these questions:

- What types of payroll documentation should be prepared at the restaurant locations?

- How will the necessary information for payroll flow between restaurants and the home office?

- How should IT systems be used in the payroll processes?

- How could Robatelli's prevent the occurrence of a ghost employee at one of its restaurant locations?

- From a cost–benefit perspective, what risks factors exist in Robatelli's payroll processes that make it worthwhile to implement thorough internal controls? Describe the related internal control that could help detect or prevent each risk.

- If Robatelli's wished to reduce the payroll risks you identified previously, it could consider outsourcing much of the payroll processing. (ADP is an example of a payroll processing company.) Search the website of a payroll processing firm to determine the benefits to Robatelli's of outsourcing a substantial portion of its payroll processing. Describe these benefits, the risks avoided by outsourcing, and the risks still borne by Robatelli's after outsourcing. Also, describe the payroll record keeping functions that Robatelli's must still maintain even if it outsources a substantial portion of its payroll processing.

- Describe how you believe an efficient and effective system of fixed assets accounting should be organized at Robatelli's. Be sure to include the following issues in your response:

- How should the fixed assets accounting department maintain control over fixed assets in the various restaurant locations?

- How should IT systems be used in the fixed assets process?

SOLUTIONS TO CONCEPT CHECK

- 1. (SO 1) Which of the statements about payroll and fixed asset processes is true? c. Both have routine and nonroutine processes. Examples of routine processes are regular payroll runs and recording depreciation. Nonroutine processes are hiring employees and purchasing fixed assets.

- 2. (SO 2) For a given pay period, the complete listing of paychecks for the pay period is a a. payroll register.

- 3. (SO 2) A payroll voucher b. authorizes the transfer of cash from a main operating account to a payroll account. After reviewing the payroll register, accounts payable prepares a payroll voucher to transfer an amount of cash necessary to cover the payroll checks written.

- 4. (SO 3) For proper segregation of duties, the department that should authorize new employees for payroll would be b. human resources. This segregates the authorization from the timekeeping and payroll record keeping.

- 5. (SO 3) Which of the statements is not an independent check within payroll processes? c. Paychecks are prepared on prenumbered checks. This is an important control concerning completeness, but it is not part of the independent check control procedures.

- 6. (SO 4) An integrated IT system of payroll and human resources may have extra risks above those of a manual system. Passwords and access logs are controls that should be used in these integrated systems to lessen the risk of d. unauthorized access to payroll data. Passwords and logs are both examples of access controls, whereas the other options are related to equipment controls and data controls.

- 7. (CPA Adapted) (SO 3) Internal control problems would be likely to result if a company's payroll department supervisor was also responsible for c. authorizing changes in employee pay rates. This would be a violation of the principle of segregation of duties, as the same employee would have both record keeping and authority functions.

- 8. (CPA Adapted) (SO 3) The procedure most useful in determining the effectiveness of a company's internal controls regarding the existence or occurrence of payroll transactions would be a. to observe the segregation of duties concerning personnel responsibilities and payroll disbursement. Option b. is concerned with the completeness assertion, option c. related to accuracy, and option d. is an independent check.

- 9. (CPA Adapted) (SO 3) In meeting the control objective of safeguarding assets, the a. treasurer should be responsible for distribution of paychecks and the treasurer should have custody of unclaimed paychecks. The payroll department should not have responsibility for either of these payroll custody functions, because it is responsible for payroll record keeping.

- 10. (CPA Adapted) (SO 3) A company's internal control policies may mandate the distribution of paychecks by an independent paymaster in order to determine that d. employees included in the period's payroll register actually exist and are currently employed. Each of the other options is related to authorization for payroll transactions.

- 11. (CPA Adapted) (SO 3) The purpose of segregating the duties of hiring personnel and distributing payroll checks is to separate the a. authorization of transactions from the custody of related assets. The human resources department has authorization responsibility with regard to payroll transactions, whereas the distribution of paychecks involves custody of payroll cash.

- 12. (CPA Adapted) (SO 3) The a. personnel department most likely would approve changes in pay rates and deductions from employee salaries. This is another name for human resources. None of the other responses is appropriate, because they each include record keeping or custody functions.

- 13. (SO 5) The purchase of fixed assets is likely to require different authorization processes than the purchase of inventory. d. Approval of the depreciation schedule is not likely to be part of the authorization of fixed assets. This is generally categorized as an independent check rather than an authorization function.

- 14. (SO 6) a. A fixed asset journal is not a part of “adequate documents and records” for fixed assets. While there should be either a manual or computerized fixed asset subsidiary ledger, a fixed asset journal is nonexistent.

- 15. (CPA Adapted) (SO 6) The question least likely to appear on an internal control questionnaire regarding the initiation and execution of new property, plant, and equipment purchases would be d. Is access to the assets restricted and monitored? This question is concerned with safeguarding of the asset after it is placed in service. Each of the other responses relates to acquisitions.

- 16. (CPA Adapted) (SO 6) a. Review of the company's repairs and maintenance expense accounts is most likely to be an indication that a company's property, plant, and equipment accounts are not understated. Fixed asset additions are sometime misclassified as repairs or maintenance expenses, so it is wise to monitor this account for the nature of the underlying expenditures.

- 17. (SO 7) c. Manual processes to link to the general ledger are not an advantage of fixed asset software systems compared with spreadsheets. Fixed asset system software usually has linkages to the general ledger. Spreadsheets do not have linkages to the general ledger and require manual processes to enter data into the general ledger.

- 18. (SO 8) The term “ghost employee” means that d. someone who does not work for the company receives a paycheck.

1“Don't Let ‘Peopleware’ Tank a New Automated Payroll System,” Human Resources Department Management Report, vol. 4 issue 1, Jan 2004, pp. 6–7.