Financial Management

Business plan, cashflow forecast, profit and loss forecast

Business plan

The RIBA Business Benchmarking Survey 2012/13 showed that 62% of architectural practices did not have a business plan, and that only 13% planned beyond the current year.5 This might explain why some architectural practices do not make much money, even if they work hard and produce good buildings.

No matter how small the practice, even if you are a sole practitioner, every practice should have a business strategy and a plan for the coming year and the longer-term future. When putting together a business plan bear in mind that you will use this document if you have to borrow capital at any point, whether in the first year of the practice or in subsequent years. The first business plan will include some guesswork about income and may make reference to relevant experience gained elsewhere, but from the second year onward the plan will reference targets that have been met, completed projects and actual turnover.

Ask your accountant or an experienced colleague to have a look at your draft business plan and give their opinion before you speak to the bank if you are hoping to borrow money.

To decide what information is relevant to the business plan, ask yourself what a bank or a relative investing in your company would want to know about you, your finances and your new company, then write this down. For the small practice or a sole practitioner, a small amount of text and a few spreadsheets (based on your last set of company accounts) that can be read and digested in 10–15 minutes should be sufficient.

It’s always hard to find time in a busy small practice, and you will be juggling priorities daily. Keep the format simple so it is quick and easy to update at least once a year. A good time to do this is after you have checked and signed the company accounts. Don’t let day-to-day deadlines on projects distract you from the longer-term objectives of the practice.

Be realistic with targets for income and growth so that in future years you will be able to demonstrate that you have met them.

A small practice might have a four- to six-page business plan, including the following sections:

Mark the business plan ‘confidential’, and arrange the signature of a simple non-disclosure agreement if you leave it with a third party such as the bank.

Cashflow forecast and profit and loss forecast

One of the advantages of having a limited company is that the accounts must be prepared in considerable detail, usually by an accountant, and an abbreviated account will be submitted to Companies House at the end of the company year. This account can provide all the information necessary to prepare a cashflow forecast for the coming year. If the practice is small and intends to stay small, and the previous year’s net profit was in line with the target set, it should not take longer than a few hours to produce a new cashflow forecast and profit and loss forecast.

As the year progresses you should make periodic checks that income is meeting the target set, and take action if income is falling short. If income cannot be increased, see whether the admin and overhead costs can be reduced. If income is not on target you may not be able to pay out planned dividends or make a one-off pension contribution as planned.

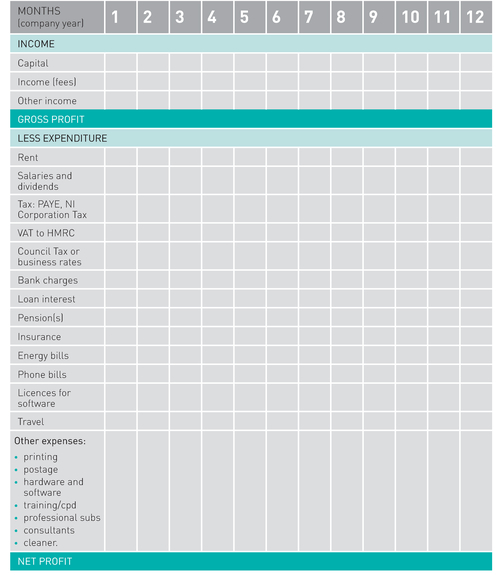

Monthly cashflow forecast

The purpose of the cashflow forecast is to ensure that there will always be enough cash in the company bank account throughout the year to make all payments when they are due.

All the figures you put in the table opposite will be estimates in year one, and you may have to do quite a lot of guesswork, but after year one you will be able to use the previous year’s figures as a reference and be more accurate. You should be able to say where the figures come from if asked.

To update the cashflow forecast, record your outgoings under the same headings used in the original cashflow forecast.

The most important figure is the income to date from fees, and this can easily be checked on an ongoing basis. For example, if the target fee income for a sole practitioner is £80k/year the target for each month will be £6.66k and the quarterly target will be £20k. A quick check against fees invoiced to date and paid will show whether the income targets are being met. Monthly expenditure can be controlled in the same way using the monthly expenses sheets and a bank statement.

Regular invoicing and prompt payment are important so you can check that your income is on target. If you do work in January you should aim to get paid in January as soon as the work or stage is complete and an invoice has been issued. Make the terms of payment clear in your appointment contract as well as the rate of interest on late payments.

You should have an overdraft facility in place with the company bank in case of the need for short-term cashflow, but it is wise to have a reasonable cash reserve in the company bank account or another reserve of capital so one or two late payments or some unexpected expenditure will not force you to rely on the overdraft facility.

Monthly profit and loss forecast

The purpose of a profit and loss forecast is to see how profitable your business is. VAT is not listed, as this is simply a tax that you collect and forward to the government.

If you exceed your target income this will enable you to set more ambitious targets for the coming year. Some practices will have one cashflow forecast to show the bank, and another more ambitious one for internal use. However, in a very small practice or when working as a sole practitioner your time is probably better spent on projects that are bringing in income.

Remember to set aside enough cash for the large lump sum payment you might have to make to pay Corporation Tax on the net profit of the company in the previous financial year. If your accountant submits your accounts at the last minute you might not get much notice of when the tax payment is due.

If you are hoping to raise capital you may be asked to provide your previous cashflow forecasts and profit and loss forecasts, so keep these records simple and accurate. If necessary, ask your accountant to prepare this information and discuss it with you before you approach the bank.

If income is less than expected, maybe there is time and scope to reduce the overheads to compensate and reduce the risk of going into your overdraft. Remember that regular outgoings will not go down even if the fee income does, and when you borrow money it must be paid back with interest.

Clients will sometimes run company checks on their architects (if they are limited companies), so it is best not to operate with a bank balance tottering close to the red line – this might give the impression that the practice is too small to do the project, or at risk of going under.

Raising money, making a profit and the company bank account

Raising money

You will need to have a business plan and a cashflow forecast to work out how much money you need to borrow, how long you need it for, who you can approach and what security you can offer.

Do not underestimate how difficult it will be to raise capital, and when you ask for a loan make sure it is for the right amount as it may not be possible to ask for more money later.

A good rule of thumb is not to use up all your own money before trying to raise more money. Your investor will want you to invest in your business as well to be sure you are committed, so will not be impressed if you say all your own money has already been spent.

There are a few different ways to raise money depending on whether you are doing this alone or with others:

There are pros and cons with all of the above, and potential risks such as being asked to provide personal guarantees or high rates of interest, so make sure you have made the right decision for your business and prepare your presentation carefully with input from your accountant as necessary.

Making a profit

Along with every other small business, the challenge you face is that everything is constantly changing and moving. If you run out of money, your business will fail. You cannot afford to not monitor your financial affairs. The first step for a business is to break even, and then to be considered successful you must make a profit.

Profit is important, as it will give you the opportunity to expand the business in whatever way you choose and will provide a healthy balance in your bank account that will not only make the company more credible, but will also help to balance the books if future months prove more difficult than expected or the odd invoice is paid late.

Controlling cash in an architectural practice means careful monthly monitoring of your debtors and creditors, and the company bank account. The better this control is, the more likely you are to see any warning signs early enough to take action. For a small practice the amount of paperwork relating to expenditure is relatively small, and the number of invoices coming in and going out will be limited, so it is easy to keep a summary sheet of income to date in any financial year. It is important to invoice regularly and to keep on top of the paperwork and chase payment if necessary. Sometimes this will mean prioritising the chasing of an invoice over another task or deadline in the office. For the small practice this constant prioritising of tasks is an essential skill that you will use daily.

If you are working as a sole practitioner you will know and deal with everything yourself, but if you employ staff and delegate parts of the business it is important to have weekly/monthly meetings to review performance and targets, and to agree and take whatever action is necessary.

You can run out of cash for a number of reasons:

The company bank account

There is no reason why you should use the same bank for your business account as for your personal account. Before setting up a new company bank account decide what advice, services and facilities you need, including overdraft and loan facilities. Check what services the different banks will provide as well as their charges, and whether there is any advantage to using a bank that has a local branch with an approachable manager you can meet when you need advice.

Charges and services vary from bank to bank for business accounts, so it is worth doing some research and shopping around.

If you have a loan from the bank, check what information the bank will need from you and how frequently.

If interest rates increase it might be worth having more than one account so cash can be moved from a current account to a savings account. However, when interest rates are low, there is little merit in doing this.

Accounts and bookkeeping

When you set up your practice you must decide what company structure to adopt and what kind of accounts you will need. It is best to take professional advice on this. It is not necessary to understand all the different types of accounting systems, but it is crucial that you understand the accounting system selected for your particular business. Regardless of who prepares the accounts, remember that you will sign them and be responsible for them.

A sole practitioner/sole trader with a small turnover might opt to do their own bookkeeping and do simple cash accounting with minimal input from an accountant at the end of the year, but unless you are short of architectural work and good with figures it makes much more sense to employ your skills as an architect to do architectural work, as this will maximise your income, and you can then employ a bookkeeper and an accountant to do the books and the accounts, run your PAYE system and do the VAT returns.

Remember that your accountant and your bookkeeper are not just the providers of spreadsheets, information and accounts required by HMRC, HM Customs & Excise (HMC&E) or Companies House. They are your colleagues, who care about what they do and what they bring to your business. If you work remotely try to make a point of meeting up with them at least once a year.

Because many small architectural practices are set up as limited companies, the advice in this section focuses on the bookkeeping and the company accounts that limited companies must prepare and submit to Companies House each year. The same systems could serve a sole trader equally well, although sole traders have the option to use simple cash accounting if their businesses are very small.

If you engage the services of a bookkeeper and an accountant you will have little to do other than provide information on a quarterly basis to your bookkeeper, and check and sign the company accounts when issued by your accountant at the end of each company year.

Accountant services

The services provided by your accountant can include the following:

Some years your accountant will do nothing more than prepare the end-of-year accounts, submit various forms to the tax office and calculate the Corporation Tax liability, but it is helpful to know that you can discuss various matters and get advice from your accountant during the year as well.

Bookkeeping services

The services provided by your bookkeeper can include the following:

Your bookkeeper will be able to run your PAYE system and set up the spreadsheets to be used throughout the year to record income and expenditure, so that the company accounts can be prepared by your accountant at the end of each company year.

The bookkeeping spreadsheets will include:

In order for your bookkeeper to have all the information necessary to prepare the above spreadsheets and to do the VAT returns each quarter, you must provide the following information on a quarterly basis just before the VAT return is due:

In a small office you should be able to keep all the above information in one filing tray, so at the end of each quarter the paperwork for the bookkeeper is ready and in one place. It should not take longer than an hour for you to sort the paperwork into bundles and hand it over to the bookkeeper. Your bookkeeper may not even need to come to the office, as the information can be sent by email or post. This paperwork should also be properly archived, as you might need it in the event of a tax office investigation.

Tax and invoices

Tax

As a small architectural practice and limited liability company the various taxes that will apply are as follows:

Paye

HMRC will provide a tax code for each individual employed by your company, including directors, and tax on salary payments will be deducted at source. Employer’s contribution is also paid monthly.

National Insurance

National insurance (NI) is paid monthly to HMRC.

Corporation Tax

Corporation Tax is paid once a year to HMRC and is based on the company net profit shown in the company accounts. Remember to set aside enough cash to pay this tax. (Sole traders will pay Income Tax rather than Corporation Tax on the profits of their company).

Vat

As a business you collect this tax from your clients and pass it on quarterly to HMC&E. You must register for VAT if the turnover of your company exceeds £83k (this value may change) in any 12-month period, and once registered you must charge your clients VAT on all the services you provide. If your business falls below the threshold you can de-register. As a business registered for VAT you will be able to claim back any VAT your company pays on purchases or services.

There are various ways of dealing with VAT depending on the size and turnover of your business:

The tax office will notify you of the dates when returns and payments are due. Late returns or late payments will result in a fine or interest being charged.

Capital Gains Tax

You may be liable for tax on any profit if you sell your business assets, including property, furniture or equipment.

Making a loss

If the company has a bad year and makes a loss it may be possible to offset this against tax due on profit in other years. Your accountant will advise you how best to deal with this loss, and the tax regulations applicable at the time of the loss.

Personal Income Tax

For company directors it makes sense for the practice accountant to do your personal tax returns as well. They will already have all the details about your employment income. All you need to do is provide details of any private pension contributions and any income not related to your company, such as interest on savings accounts or dividends on shares or rental income. Your accountant will also be able to tell you how much you must pay, and when.

Directors who take part of their income in the form of dividends will be paying tax monthly through PAYE and topping up with lump sums twice a year (31 January and and 31 July). These lump sums are based on the assumption that your income in the coming year will be the same as in the previous year. On receipt of your tax return the tax office will notify you how much you must pay, or how much is to be refunded, and the deadlines.

Tax investigation

Remember that it is illegal to conceal any earnings from the tax office, and you should try to avoid any investigation by the tax authorities. You can do this by ensuring that all income is declared, your accounts are sufficiently up to date and accurate, and that your returns are filed and payments are made on time. Having an agent to do this for you will help.

Tax invoices

Tax invoices that are sent to your clients should include the following details:

Copies of your invoices should be archived. Each invoice amount should be recorded on a spreadsheet so that income to date can be calculated at any point during the year in seconds.

Overheads

It is important for the long-term success of your business to establish the right balance between income and expenditure. Fee income in any architectural practice will vary from year to year, but most of your overheads (rent, salaries, software licences, etc.) will remain fixed.

The typical overheads for a small architectural practice include:

Some of this will be capital expenditure, such as furniture or computers that will last for more than two years. These items will depreciate over time and the depreciation will be accounted for in your end-of-year accounts.

The other items are revenue expenditure, and these items are allowable as expenses that can be deducted from your gross profit to calculate the net profit on which your company Corporation Tax will be based.

Any petty cash expenditure during each month should be recorded on an expenses sheet, with copies of all receipts stapled to the sheet. At the end of each month you will be paid back for any mileage or out-of-pocket expenses on behalf of the company. These expenses sheets should be archived.

Fees

The way you charge for your services will depend on the size and type of work. The fee can be a combination of the following methods of charging:

Percentage fees

For domestic work, a percentage fee based on the construction cost is the traditional way of charging for architectural services. The percentage is based on the initial budget for construction, but at the end of the project the percentage is based on the final account figure – you should explain to your clients how this works. The benefit of this fee structure is that it is self-adjusting throughout the project, so as your client adds work to the project and the construction cost increases the fee increases without the need for further negotiation. You will need to keep your client informed of any increase in the construction cost and the overall cost of the project, and obtain their agreement to the revised cost.

The RIBA used to issue a fee graph showing the recommended percentage fee appropriate to every type of project for both new-build and refurbishment work, but this graph and the idea of mandatory fees were scrapped in favour of the free market. However, there is nothing to stop you having your own in-house fee graph similar to the old RIBA one to help you set percentage fees. As long as the fee has been carefully set at the right level, the method works well.

The percentage fee covers the basic services from the RIBA Plan of Work Stages 2–6. Services at Stage 1 and additional services during Stages 2–6 can be charged on an hourly basis. The percentage and any hourly charged services should be explained to your client and confirmed in the appointment contract before you start work. You can also show fees on the Plan of Work. Any change to the appointment contract (such as the construction cost on which your fee is based) should be agreed with the client and confirmed in writing.

The total percentage fee can be broken down into the RIBA Plan of Work Stages as follows:

RIBA Fee Calculator

The RIBA provides guidance on how to calculate fees using the RIBA Fee Calculator.6 With this guidance and the RIBA Plan of Work 2013 you will be able to give a detailed breakdown of the service you will provide at each stage, the fees at each stage and the total fee. If you agree a total fee at appointment you will also have to agree the basis on which you will be paid for any additional work, and how this will be measured. Domestic clients almost always add in work at every stage of the project or take work out and substitute it with other work, so you must ensure in advance that you will be paid for any extra or abortive work.

Lump sum fee

If your client asks you to agree a lump sum fee, explain that the fee will be based on a fixed scope of work. Explain that any work not included in the original brief will be charged for separately on an hourly basis. This explanation is often enough to persuade a domestic client that a percentage fee is probably a better option, as most of these clients add work to the contract at every stage.

Time charge

Other services that are not included in your percentage fee can be charged on a time basis, such as feasibility studies at Stage 1, or additional submissions to planning, or negotiating a contract instead of going out to tender.

On very small projects (£40,000 and less) it may be appropriate to charge on a time basis rather than a percentage fee. Your total fee can be based on an estimate of the time the project will take and broken down into Stages 1–6. If your estimate will be exceeded you must agree in advance the additional time necessary. For example, if you estimate that six site visits are necessary to administer the contract but eight site visits are required, you must agree the additional cost of the two site visits in advance. If your client adds work into the contract you must also estimate and agree the additional time required.

Expenses

Expenses will be incurred on all your projects (travel, parking, printing, postage, purchase of contracts, OS maps, etc.) so you should make it clear in your appointment that these expenses will be counter-charged to the client and will be in addition to your percentage fee or time charge fees.

Working for nothing

In the early days of our practice a psychiatrist friend made a wise observation: ‘If you work for free you will always have work!’

Not all the work you take on will be as productive as intended or make the profit you had in mind, but you should never agree to provide professional services for free, as you will always be liable for professional advice given. If you charge properly you are more likely to have your time and your work appreciated. Further guidance on this topic is included in Part 3, under ‘The Architect’s Appointment’.

Competitions

If your practice enters competitions for which there is no guaranteed payment or fee, you must ensure that sufficient funds are available within the practice to cover this, and that the lack of payment for this work will be offset by other profitable projects in the practice. A competition can benefit the practice in other ways: it might raise the profile of the practice, generate a project that will look good on the practice website or allow you to gain experience in a new area of work. If you win the competition you might secure the project (and the future of the practice), so it could prove a good investment of time. Sadly not all projects for new buildings won through competition are built.

Chasing money and reducing the risk of bad debt

There are various ways of reducing the risk of bad debt within your practice.

Very occasionally a client will find fault with your work to justify withholding payment. They may wait until receipt of court papers before paying, or worse, on receipt of court papers they may make a counter-claim that will mean you must involve your insurers. Immediately you have a situation that could cost you far more than the outstanding fee. If you can spot the type of person who will behave like this early enough, try to avoid working with them in the first place. Not only will they waste a lot of your time, they will be unpleasant to work with and could cost you a lot of money. If you are halfway through a project before the client reveals their true colours, accept the fact that they will be difficult and decide how you will deal with the situation. Seek advice if necessary and invoice on a regular basis for small amounts.

Good financial management is important, especially when it comes to the collection of money that is owed to the business.