Chapter 17

Ten Criticisms of Cryptocurrencies and Mining

IN THIS CHAPTER

![]() Re-evaluating Proof of Work energy consumption

Re-evaluating Proof of Work energy consumption

![]() Finding ways to reduce computational waste

Finding ways to reduce computational waste

![]() Putting transaction-throughput metrics in context

Putting transaction-throughput metrics in context

![]() Avoiding scams and rip-offs

Avoiding scams and rip-offs

![]() Averting fires and neighbor complaints

Averting fires and neighbor complaints

Many criticisms and complaints have been leveled at cryptocurrencies and, in particular, the Proof of Work mining that often underpins them. Many of these criticisms are valid, but these topics have a ton of nuances that deserve thorough explanation, discussion, and debate. In this chapter, we explain some of the most common criticisms as well as some of the counter arguments associated with them.

Energy Consumption

There has been much ado about Bitcoin’s and other cryptocurrencies’ network energy consumption that occurs as a result of Proof of Work mining. As you learn in this book, it takes truly massive amounts of electrical energy to mine the Bitcoin blockchain.

It is true that Proof of Work mining consumes a very large amount of electricity. However, the exact amount is in dispute and, in fact, very difficult to calculate precisely. Many frequently cited estimates are based on a single-sourced energy estimation that performs an estimation based on how much energy network miners could afford to expend. In other words, it is an economic calculation with many assumptions involved, including market price, miners’ electricity costs, and miners’ electricity consumption.

This type of economic energy estimate ignores many on-chain statistics that can more accurately calculate network energy consumption with physics based on chain data, such as blocks mined per day, total network hash rate, and average mining equipment efficiency.

Luckily, today there are now many different estimations of the Bitcoin network’s Proof of Work energy consumption, from a variety of reputable sources that have calculated energy consumption using more realistic physics-based calculations. Table 17-1 lists a variety of estimates of Bitcoin’s mining instantaneous power consumption in Gigawatts (GW), and yearly energy equivalents (in Terawatt-hours/year — TWh/year).

TABLE 17-1 Estimates of Bitcoin’s Mining Power Consumption

Source | URL | Instantaneous Power Consumption | Yearly Energy Equivalents |

|---|---|---|---|

Alex de Vries (July 2019) | 8.34 GW | 73.12 TWh/year | |

Coin Center (May 2019) |

| 5 GW | 44 TWh/year |

CoinShares (June 2019) |

| 4.7 GW | 41.17 TWh/year |

EPRI (April 2018) | 2.05 GW | 18 TWh/year | |

Hass McCook (August 2018) |

| 12.08 GW | 105.82 TWh/year |

IEA (July 2019) | 6.62 GW | 58 TWh/year | |

Marc Bevand (January 2018) | 2.1 GW | 18.39 TWh/year | |

University of Cambridge, Judge Business School (June 2019) | 6.36 GW | 58.97 TWh/year |

You can see these various estimations in the chart shown in Figure 17-1. The chart shows the various energy estimations in TWh/Year on a timeline, along with the Bitcoin network hash rate (EH/s) from 2017 to 2019 (as hash rate goes up, power consumption rises, of course).

FIGURE 17-1: The various Bitcoin yearly energy estimates measured in Terawatt-hours per year, along with the Bitcoin network hash rate measured in Exahashes per second.

To put these consumption figures in perspective, the United States typically uses 6.63 TWh/Year to decorate and celebrate the holiday season with Christmas lights (and those typically are only on for around a month).

Perhaps a more appropriate comparison would be the amount of electrical energy annually dedicated to gold mining and recycling. Hass McCook, in the paper previously cited, estimates the amount of global energy used in this arena is the electrical equivalent of 196.03 TWh/Year, almost twice the energy (based on Haas’ calculations) used by Bitcoin mining, even including the power used to create the mining equipment — considerably more if we take some of the other power estimates for Bitcoin. And, by the way, have you any idea of the huge environmental impact of gold mining? Do a search for gold mining environmental impact … the more environmentally minded among you might just give up gold jewelry! For example, gold mining creates huge amounts of toxic waste: 60 tons of toxic waste, including cyanide, arsenic, and mercury, for every ounce of gold mined by some measures!

Around 90 percent of the world’s gold is used as an asset store of value and for jewelry, and much of the world’s gold jewelry is itself regarded as a store of value, so the industrial uses of gold makes up a relatively small portion of its use. Thus, according to McCook’s numbers, around 175 TWh/Year of energy is being used for these essentially nonproductive uses of gold. One might argue that shifting the investment role of gold over to Bitcoin (as some cryptocurrency proponents claim will happen eventually) may actually save energy! (And the environment.)

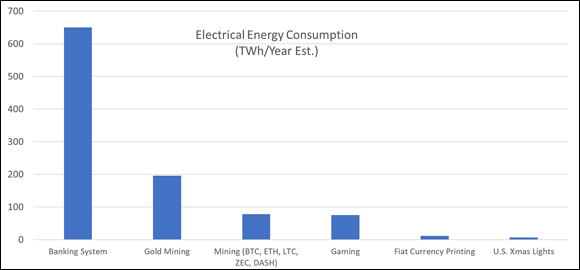

In a similar report from 2014, Hass McCook also estimates (see www.coindesk.com/markets/2014/07/19/under-the-microscope-conclusions-on-the-costs-of-bitcoin) the amount of yearly energy dedicated to paper currency printing and coin minting (11 TWh/Year) and the amount of yearly consumption of the banking system (650 TWh/Year). A new world of cryptocurrency (wait 25 years and see what happens!) may well reduce the amount of energy expended each year to manage the world’s money supply. See Figure 17-2 for a graphical display of these various comparisons in estimated yearly electrical energy. The cryptocurrency mining yearly energy bar includes estimates of power consumed by the Bitcoin, Ethereum, Litecoin, DASH, and Zcash networks.

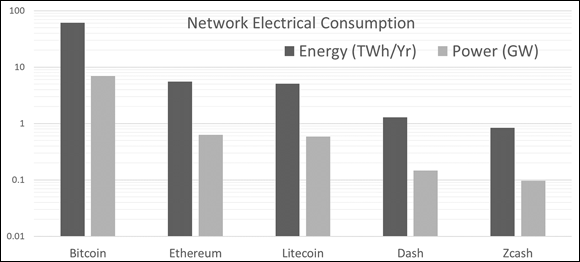

We also estimated the energy consumption levels for other popular Proof of Work cryptocurrencies, by comparing the network hash rates with the efficiency of the network’s ASIC miners based on manufacturer-provided data. These include Bitcoin, Ethereum, DASH, Litecoin, and Zcash. Figure 17-3 shows the comparisons. Data includes instantaneous electrical power consumption, measured in Gigawatts, as well as yearly energy values, measured in Terawatt-hours per year.

While the levels of energy consumption for global Bitcoin mining may sound obscenely large, they only total around 0.2 percent of global electricity usage, and a few of the preceding studies also estimate that 60 to 75 percent of the electricity sourced for Bitcoin and cryptocurrency mining is from renewable resources.

FIGURE 17-2: Comparison of yearly energy consumption for a variety of uses, measured in Terawatt-hours per year.

FIGURE 17-3: Network electrical power and yearly energy estimations for various cryptocurrency networks that use Proof of Work mining.

Wasted Processing

Another criticism often leveled is that Bitcoin or cryptocurrency mining is a waste of processing resources that could be better used elsewhere. This criticism has some validity. Vast amounts of processing power are being used to mine cryptocurrency rather than cure cancer or malaria or solve critical physics problems that could lead to new materials or energy supplies.

Of course, it all depends on what an individual considers waste. The definition of both waste and value lie in the eyes of the beholder.

Waste is typically defined as careless usage toward no purpose. Certainly, cryptocurrency mining does in fact have a purpose: to secure the various peer-to-peer blockchain networks against would-be attackers by making it too computationally expensive to manipulate the network. The Proof of Work mechanism rests in game theoretical mechanisms and economic theory that make it more rewarding for an attacker to work in cooperation with the network than to use their computational resources against it.

However, it still seems wasteful that as soon as a block has been added to the blockchain, the value of the computations that went into mining the block has gone, and no further value is provided (and remember, we’re not talking about the computations provided by the winning miner; we have to count the vast amount of computing power provided by the entire network).

Many people cringe at the thought of this immense waste, and so, perhaps not surprisingly, there are examples of Proof of Work cryptocurrencies that have tried to solve the wasted-processing-power problem. After all, Proof of Work depends on a mathematical game. What if that game could, at the same time as it secures the blockchain, provide humanity with an additional benefit, the icing on the cake as it were? Here are a few examples of cryptocurrencies that have attempted to point their Proof of Work mechanisms toward philanthropic causes:

- Primecoin (

http://primecoin.io) is a cryptocurrency system that rewards miners for finding prime numbers. A prime number is a whole number that can only be divided evenly by itself or 1. Prime numbers have been a subject of mathematical study since the time of the ancient Greeks and are very valuable to mathematicians for, um, whatever they do with prime numbers. (Okay, a real example is encryption, which uses prime numbers; apparently, it’s useful to have a library of these things. Quantum physicists like them, too.) - Foldingcoin (

https://foldingcoin.net) is cryptocurrency that rewards miners for folding proteins based on the Stanford Folding@home distributed-computing project. Protein folding helps search for protein compounds that can help cure cancer, Alzheimers, and other diseases. - Curecoin (

https://curecoin.net) is another cryptocurrency rewarding miners for folding proteins based on the Stanford Folding@home project. - Gridcoin (

https://gridcoin.us) is another coin based on a different distributed computing project, but this time using the BOINC (no, it’s not a joke) distributed-computing project. BOINC uses spare computing resources (and, through Gridcoin, computing power being employed for mining) to help with a variety of science-research projects that investigate diseases, study global warming, discover pulsars, and do many other things.

Unfortunately, these cryptocurrencies are all pretty small, with a total combined market capitalization of around $7 million, a drop in the bucket compared to Bitcoin’s current $177 billion. But, there could be a day when the world’s cryptocurrencies are mined using algorithms that both protect the blockchains and do additional good. As Sunny King, founder of Primecoin, puts it, “I would expect Proof of Work in cryptocurrency to gradually transition toward energy-multiuse, that is, providing both security and scientific computing values.” On the other hand, the argument against this is that the Proof of Work algorithms of the major cryptocurrencies are pretty simple. Introducing more complicated algorithms may also introduce vulnerabilities and create more potential for attack.

One more thing: How much computing power do you suppose the world’s gamers use? That’s hard to accurately compute, but someone has tried to compute the energy use, and as a lot of mining is using similar equipment (GPU cards were designed for gaming!), the comparison is probably similar (that is, the relationship between energy consumption and computing power is similar, although gamers also have to power their displays). This guy, Evan Mills of the Lawrence Berkeley National Laboratory, and a member of the Intergovernmental Panel on Climate Change, came up with 75 TWh/Year.

Scalability, Transaction Speed, and Throughput

Bitcoin and other cryptocurrencies have often been criticized for having low transaction speed and throughput. This criticism is valid, as current on-chain transactions per second average between 2 and 8. The theoretical maximum for on-chain transactions on the Bitcoin network stands at around 14 transactions per second, which would equate to roughly 1.2 million transactions per day.

To put this amount in perspective, think about the credit card networks. Visa processes around 150 million transactions per day, a little more than 1,700 a second. That’s an average, of course, so they must be able to handle plenty more than that during peak hours, and they claim to be able to handle 24,000 a second, though it’s unclear if that is true. Regardless, these numbers are vastly higher than Bitcoin’s capabilities.

Credit card systems are widely misunderstood; they appear instantaneous to the user — they seem to take just seconds to process while you’re in the grocery checkout line — but in fact they actually take considerably longer. Take a look at your credit card statement, and you will find transactions taking a day, sometimes two — sometimes even longer — to post to your account. Then, of course, the transactions can be challenged, and sometimes reversed, often weeks later.

Your credit card transactions go through multiple steps, in fact, and this system is very complicated with multiple parties involved. A transaction begins with a payment processor, such as First Data (America’s largest processor for brick-and-mortar stores), or an ecommerce payment processor, such as Stripe or PayPal; it gets passed to the credit card company’s own network — VisaNet, for example, or, for MasterCard, BankNet — but it ultimately ends up at a bank, which handles the final clearance, running it through the SWIFT network (the Society for Worldwide Interbank Financial Telecommunication). The process frequently takes a day, but it can take as long as four business days to complete a credit card transaction, and in some cases, the transaction can be disputed for up to three months later.

These types of credit card charge backs and disputes are one reason some credit card companies do not allow Bitcoin or cryptocurrency payments via their credit card infrastructure, because credit card transactions can be disputed, reversed, and refunded while Bitcoin transactions cannot.

How about Bitcoin and other cryptocurrency transactions? As far as Bitcoin goes, a transaction is considered to be settled and essentially irreversible in a matter of six blocks, or so (roughly an hour). This may seem slow until you compare it to the one to three days for credit card transactions. We think Satoshi Nakamoto put this settlement time in perspective: “Paper cheques can bounce up to a week or two later. Credit card transactions can be contested up to 60 to 180 days later. Bitcoin transactions can be sufficiently irreversible in an hour or two.” (For a comparison of relative blockchain transaction security and finality times for other cryptocurrencies, view the real time statistics on https://howmanyconfs.com.)

The on-chain transaction count for Bitcoin and other cryptocurrencies is somewhat skewed, however, as many transactions can occur off-chain. These off-chain transactions can occur via exchanges, custodial wallets, or more distributed second layer solutions, such as the Lightning Network. This protocol is built on top of the Bitcoin blockchain that uses Hash Time Locked Contracts (HTLCs) that allows for more transactions per second and quicker transaction finality. A single on-chain Bitcoin transaction can contain thousands (or more) lightning network transactions. (For more information on this complicated subject, check out the lightning network whitepaper at https://lightning.network/lightning-network-paper.pdf and the lightning network Bitcoin wiki at https://en.bitcoin.it/wiki/Lightning_Network.)

Another way that transaction speed can be higher than the simple Bitcoin transaction count is through the use of batched transactions. A pool or exchange can batch a single on-chain transaction that includes up to 100 to 250 output addresses, essentially increasing the transaction throughput while the blockchain counts only a single transaction.

However, the underlying criticism still remains: There is an on-chain throughput bottleneck, but this blockchain space scarcity is also critical to the network’s decentralization. Each on-chain transaction is verified, validated, and stored on the entire peer-to-peer system of nodes, and efficient utilization of this scarce space and shared resource is critical to maintaining the distributed nature of cryptocurrency systems such as Bitcoin.

Coin Distribution Fairness

Cryptocurrencies such as Bitcoin are often criticized for unfair coin distribution. This criticism stems from the front-loaded block subsidy rewards. The Bitcoin network subsidy rewards programmatically decline over time, as shown in Chapter 8. As seen in Chapter 8, rewards are greater for early miners and steadily decline over time (the Bitcoin subsidy halves roughly every 4 years or 210,000 blocks). Many cryptocurrencies mimic this same type of distribution.

However, Proof of Work coin distribution is much fairer than Proof-of-Stake (POS) systems that reward large stake holders and also more fair than initial coin offerings (ICOs) that often steal investor funds with no measurable return. Cryptocurrencies that have significant premines rewarding early investors, or even our current paradigm of the fiat-based currency distribution system, in which certain large financial institutions control the flow of money through the economy, taking large bites out of it as it passes through their hands, are much less fair.

Market Bubbles and Volatility

Another common criticism of cryptocurrencies is that it’s nothing more than an investment bubble. Skeptics often compare cryptocurrencies to other famous investment bubbles, such as the Dutch Tulipmania in the early 17th century, the South Sea Company (early 18th century), and the Internet, or Dotcom, bubble (from 1994 to 2000).

Peter has an interest in financial bubbles, having lived through and intimately experienced the Dotcom bubble. The summer before it began, 1993, he was writing the Complete Idiot’s Guide to the Internet (he dates the start of the bubble to the dramatic growth in press coverage, and the millions of Americans jumping online, in the summer of 1994). By the time the bubble burst (the late summer and fall of 2000) he was running a VC-funded dotcom. Early in 2000, he read The Internet Bubble (Harperbusiness), a book predicting the coming crash, and circulated it among his dotcom’s executive staff.

The authors of this book, Anthony Perkins and Michael Perkins, editors at Red Herring (a dotcom-business print magazine that ironically did not long survive the bubble bursting!), proposed that financial bubbles typically last six to seven years. The South Sea Company’s stock price crashed about nine years after the company was founded (though it’s hard to say exactly when the bubble began, of course). The Dotcom bubble burst six years after the Internet craze began.

Are cryptocurrencies, and Bitcoin in particular, in a “bubble”? That’s hard to tell, but so far it’s not looking that way. The Bitcoin software was first released in January 2009, so it’s been around for more than 13 years now. (Of course, it doesn’t mean the bubble itself began with the founding of Bitcoin; the Internet dates to the 1960s, but the Internet Bubble did not begin until the 1990s.)

It may be that because cryptocurrencies have relatively low market capitalizations compared to other traditional assets, such as gold or the U.S. dollar, they are subject to less liquidity, and thus more volatility. Any new asset, as it gains popularity and acceptance, has large fluctuations in market exchange rates. This is, in part, due to market price discovery and asymmetric information surrounding the cryptocurrency markets. Volatility and the perception of a bubble may not completely subside until Bitcoin and other cryptocurrencies gain relative market capitalization parity and exchange rate stability in comparison to other large capitalized assets.

For the moment, it looks very much like cryptocurrencies are not going away. In fact, more and more large companies, including financial powerhouses, are getting involved. There are good reasons why cryptocurrencies may be a technical advancement that can be beneficial and will stick around.

Also, consider this: While the South Sea Company crashed and eventually went out of business … while tulips in Holland eventually came down to a reasonable price and stayed there (though even today rare tulips command high market prices) … the Internet or Dotcom bubble destroyed thousands of companies, but the Internet didn’t go away! The Internet is now thoroughly entrenched in modern life; it’s inconceivable, barring global catastrophe, that it will go away. And many companies founded before the bubble burst are still with us. One of the very earliest, Amazon, is today one of the world’s largest companies.

Centralization

Centralization of cryptocurrencies is often cited as a serious problem. Cryptocurrencies require decentralization to function safely and securely. Both mining and code development needs to be decentralized and distributed to ensure that no single party or group can dominate and manipulate the currency.

It’s often claimed that mining is centralized in a few countries and dominated by a few pool entities, and even that the program code running the cryptocurrency networks is written and managed by relatively few people. This calls into question the distributed properties of these peer-to-peer cryptocurrency networks. While these criticisms are valid and worth intellectual pursuit, they are also somewhat misconstrued.

Bitcoin and most other cryptocurrencies are based on open-source software, to which anyone can review and contribute code improvements. While many code improvements can and do occur on these open, distributed cryptocurrency systems, and numerous individuals are involved in adding code changes, for those who would like to change the underlying principles and mechanisms of the Bitcoin code base for their own personal or business interests, we think Satoshi Nakamoto said it best: “The nature of Bitcoin is such that once version 0.1 was released, the core design was set in stone for the rest of its lifetime.” In other words, the consensus rules are set from the start of the blockchain, from the genesis block. Change the consensus rules, and you become “out of consensus” with the rest of the chain and network; you “fork off” and become a different blockchain and network.

However, centralization is a real concern. These peer-to-peer systems were designed to center around CPU miners running their own fully validating node. However, since Bitcoin’s inception, mining pools have been popularized, ASIC equipment has developed, and massive cryptocurrency mining farms have become commonplace. These developments have led to greater centralization of the ecosystem.

In Chapter 8, we discuss the decentralization scale, how centralization and decentralization are not simply two distinct things, but that systems can be centralized or decentralized to differing degrees. That applies here; Bitcoin and cryptocurrency mining centralization falls somewhere on that scale, at the time of writing arguably more toward the decentralized side of the scale. With proposed mining developments, such as BetterHash pool improvement and Stratum v2 (which are proposals to improve the integration mechanisms between pool users and pool operators), Bitcoin and other Proof of Work mined cryptocurrencies may move toward even greater decentralization.

Scams and Rip-offs

The cryptocurrency arena is rife with scams and rip-offs. Between hacked exchanges, nefarious mining equipment providers, and dishonest cloud mining companies, the history of Bitcoin is littered with many examples of companies and individuals taking advantage and scamming well-intentioned consumers out of their hard-earned value in Bitcoin, other cryptocurrencies, or local fiat currency.

There have also been countless scams involving initial coin offerings (ICOs) that have promised more than their propagators can deliver (or ever intended to deliver) and stole billions of dollars’ worth of investors’ money.

This is a serious problem for cryptocurrencies, as it helps to paint a picture of cryptocurrency as being dangerous and unreliable, and not something the average Joe would want to be involved with. This viewpoint, of course, retards growth in the cryptocurrency markets.

These criticisms are incredibly valid, and the only way to protect yourself from would-be bad actors, scams, and rip-offs in the Bitcoin and cryptocurrency space is to learn and understand what you are doing, do your research thoroughly, and as always don’t trust, verify.

Hardware Price Inflation and Scarcity

Another issue with Bitcoin and cryptocurrency mining as of late is that hardware price inflation and scarcity has led to shortages for other uses of the equipment.

For example, as GPU mining was gaining popularity and profitability, demand for this form of computational hardware skyrocketed, prices soared, and availability dropped. This led to typical users of this type of computer equipment (predominantly PC gamers, as well as video producers and graphic designers) to have to pay higher prices for their equipment, if they could get it at all.

However, it can also be argued that the high demand for GPUs and ASICs led to innovation in the printed circuit board (PCB) arena, resulting in increased production, development, and manufacturing volume and the improvement of other chip applications, such as cells phones, laptops, and basically any other electronic devices that rely on PCB-based computer chips. The innovations that have been spearheaded by cryptocurrency mining ASICs have leaked into almost every other industrial computer-chip application.

Fire Hazards

There have been a few noteworthy examples of cryptocurrency hardware catching fire; it’s not common, but it does sometimes happen. GPU rigs and ASICs run at very high temperatures, and if the equipment, which uses large amounts of electrical power, is not properly installed, configured, or maintained, it could very well be a fire risk.

For example, a fire in a cryptocurrency mine, operating out of an apartment in Vladivostok, Russia, destroyed eight apartments; 30 more were flooded when firefighters were dispatched to put out the blaze.

This just means you must do this right! You need a properly rated and installed power supply and electrical infrastructure; in fact, if electrical supply equipment is installed correctly by a qualified and certified electrician, this problem is almost nonexistent.

Seek the advice of a local certified electrician in the installation of circuits or the inspection of existing wiring to be used for your cryptocurrency mining electrical equipment. Also, ensure fire alarms and proper fire extinguisher equipment is always nearby in the event of an electrical fault or an equipment fire. (Of course, this is good advice for any home or work location.)

Seek the advice of a local certified electrician in the installation of circuits or the inspection of existing wiring to be used for your cryptocurrency mining electrical equipment. Also, ensure fire alarms and proper fire extinguisher equipment is always nearby in the event of an electrical fault or an equipment fire. (Of course, this is good advice for any home or work location.)

Neighbor Complaints

Cryptocurrency mining equipment can be very loud, thanks to its high-frequency cooling fans. Neighbor complaints related to both small and large mining operations are common. (Go ahead, search your favorite search engine for neighbors cryptocurrency mining noise, and you’ll find a bunch of headlines: “What’s that noise? One of the world’s largest Bitcoin facilities is too loud.” “Bitcoin mining operator struggles to comply with city noise ordinance.” “Buzz From Bitcoin Mining Upsets the Neighbors,” and so on).

This criticism falls into the category of NIMBY (Not in My Back Yard). Not surprisingly, folks don’t want their peace disturbed by what are essentially industrial processes near their homes. A few small towns have even lobbied their local governing boards to place a moratorium on cryptocurrency mining due to the noise and other concerns, such as power usage and local grid limitations, related to cryptocurrency mining.

What’s the answer? For large facilities, probably the only reasonable answer is to locate far from homes! For small, home-based mining operations, it may be more difficult, especially if you are an apartment dweller. However, silencing mechanisms do exist for mining equipment, and some enterprising miners have deployed quiet installations (see Chapters 12 and 15).