INTERRELATIONSHIPS OF BUSINESS PROCESSES AND THE AIS (STUDY OBJECTIVE 1)

Chapter 1 introduced an accounting information system as a system that captures, records, processes, and reports accounting information. The information captured is the result of financial transactions within the organization or between the organization and its customers and vendors. When a transaction occurs, there are systematic and defined steps that take place within the organization to complete the underlying tasks of the transaction. These steps are business processes. A business process is a prescribed sequence of work steps completed in order to produce a desired result for the organization. A business process is initiated by a particular kind of event, has a well-defined beginning and end, and is usually completed in a relatively short period of time. Business processes occur so that the organization may serve its customers.

Every organization exists to serve customers in some way. Some organizations make and sell products, while others provide services to customers. Nearly everything that an organization does to fulfill its day-to-day activities is part of a business process. When organizations buy, sell, produce, collect cash, hire employees, or pay expenses, they are engaged in business processes, all of which support the objective of serving customers. The examples of beverage or food service to customers are business processes.

Each business process has a set of systematic steps undertaken to complete it. Some business processes you see in your everyday life. For example, when you eat at a restaurant, the restaurant must have established a systematic set of steps that employees perform to serve you. A host meets you at the door to seat you, and a server has been preassigned to that table. The server takes your order and relays the order to the kitchen. The kitchen personnel have a predesigned set of activities to prepare your meal. The server then delivers your meal, checks on you periodically throughout the meal while you are eating, and presents a bill; then you pay the bill. All of these activities are business processes for a restaurant.

As these many business processes occur, data are generated that must be collected by the accounting information system. The restaurant must have a system to capture and record the revenue generated by your meal, the details of your credit card payment, the food used in your meal and its cost, the wages paid to the server and host, and any tips. For nearly all of the business processes in an organization, there are accounting effects. As the systematic steps are undertaken in a business process, the accounting information system must capture and record the related financial data.

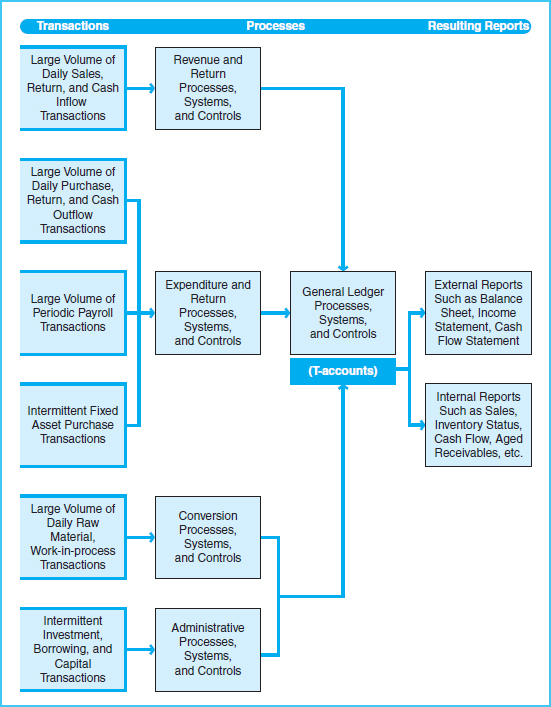

Exhibit 2-1 shows the relationships among transactions, business processes, and the reporting of information. As transactions occur, business processes are undertaken to complete the transaction and record any relevant data. Within any business, there may be hundreds of business processes. Moreover, these business processes may vary from company to company. For example, the business processes of a local, family restaurant are probably very different from the business processes of a global fast food franchise like McDonald's. In addition, the business processes of McDonald's would be vastly different from, for example, the business processes of Nokia Corp., a mobile phone manufacturer. However, regardless of the type of business, as you will recall from Chapter 1, the general categories of business processes that are used to organize the concepts of most business processes include revenues processes, expenditure processes, conversion processes, and administrative processes.

Exhibit 2-1 Overall View of Transactions, Processes, and Resulting Reports

To properly capture and record all relevant financial data, an accounting information system must maintain both detail and summary information. In traditional, manual accounting systems, the detailed transaction data are taken from source documents, special journals, and subsidiary ledgers and are summarized and posted to the general ledger. Exhibit 2-1 depicts the processes that summarize the detailed data into general ledger accounts.

Most accounting systems today are computerized to some extent, but there still remains a need for paper documents in many systems. Regardless of the extent of computerization, all accounting information systems must capture data from transactions within business processes, complete the necessary processing of that data, and provide outputs.