FIXED ASSETS PROCESSES (STUDY OBJECTIVE 5)

There may be many kinds of fixed assets owned by a company. The fixed assets pool may include the following categories: vehicles, office equipment and computers, machinery and production equipment, furniture, and real estate (such as land and buildings). These assets are all necessary for the company to conduct business. They are considered long-term assets because they were purchased with the intention of benefiting the company for a long time. For many companies, the investment in fixed assets is often the largest asset reported on the balance sheet.

Even though fixed assets are classified as long-term assets, they are constantly changing. Companies continually add to or replace items in their fixed assets pool as the old items become used, worn, or outdated. Due to this frequency of change, it is important that clear accounting records exist so that the status of fixed assets accounts can be determined at any point during their useful life.

This section presents three phases of fixed assets processes: acquisition, continuance, and disposal. These three phases span the entire useful life of the fixed assets.

FIXED ASSET ACQUISITIONS

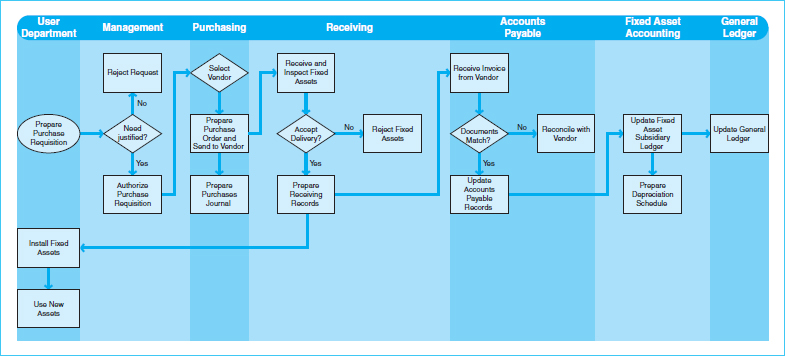

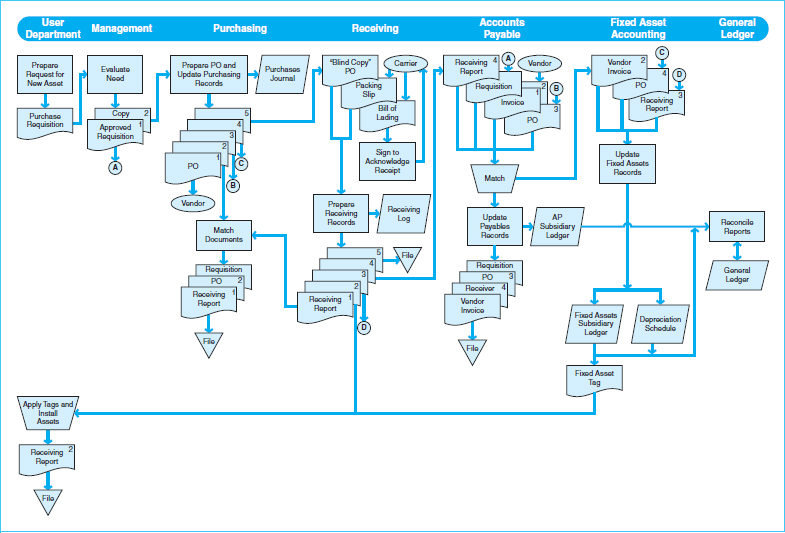

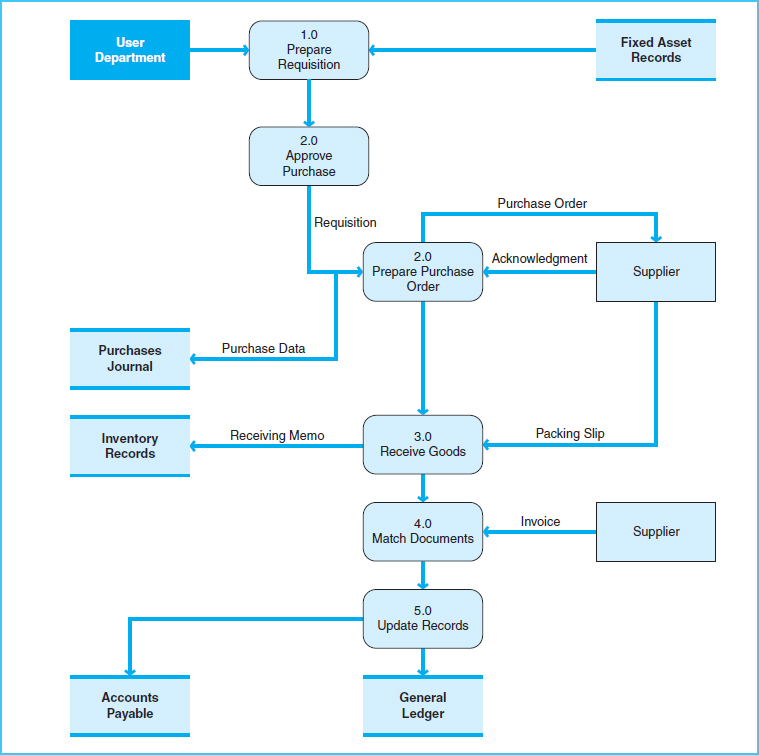

Acquisitions of fixed assets are carried out in much the same way as inventory purchases described in Chapter 9. Exhibit 10-8 presents a business process map of the fixed assets acquisition process. You can see the similarities in these processes by comparing this exhibit with Exhibit 9-3 in Chapter 9. Two notable differences here are the placement of the acquired assets in the user department (rather than a warehouse) and the inclusion of a fixed assets department (instead of the inventory control department). Exhibit 10-9 presents a document flowchart of the records used in a fixed asset acquisition process, and Exhibit 10-10 is a data flow diagram of that process.

Fixed assets acquisitions are generally initiated when a user department identifies a need for a new asset, either to replace an existing asset or to enhance its current pool. If the need is for an asset whose cost is below a preestablished dollar amount, the process will be carried out in a routine manner, as illustrated in Exhibit 10-8. That is, a member of management will authorize the purchase of the asset, and the purchasing department will select a vendor and prepare the purchase order.

Sometimes, large cash outlays are required for fixed asset purchases. The company should have a policy in place requiring special processing for purchases of fixed assets that exceed a preestablished dollar limit. Accordingly, large fixed asset acquisitions would be regarded as nonroutine transactions that require specific authorization. This may delay the process significantly, as it may take weeks or months for management or the board of directors to approve large fixed asset purchase requests. Some companies require that large cash outlays for fixed assets be included in the capital budget. A capital budget is a financial plan detailing all of the company's investments in fixed assets and other investments. In addition, the company may require that an investment analysis or feasibility study be conducted in order to assess the merit of the purchase request in terms of the relative costs and benefits. Accordingly, these purchases need to be planned well in advance of their desired implementation time.

Exhibit 10-8 Fixed Assets Acquisitions Process Map

Exhibit 10-9 Document Flowchart for Fixed Asset Acquisition Processes

Exhibit 10-10 Fixed Asset Acquisitions Processes Data Flow Diagram

Upon receipt, new fixed assets are inspected by the receiving department. A receiving report is prepared, and the items are sent to the user department for installation and use. Many companies apply a fixed asset tag, number, or label to the item so that it can be tracked in the future and distinguished from other, similar assets. Accounts payable and cash disbursement activities are also initiated at this time, in the same manner as for the expenditure processes described in Chapter 9. In addition, a fixed asset subsidiary ledger is updated. A fixed asset subsidiary ledger is a detailed listing of the company's fixed assets, divided into categories consistent with the general ledger accounts. Historically, companies have maintained all the subsidiary ledger details within spreadsheets. Separate spreadsheets may be prepared for each category of fixed assets.

Extreme care must be taken in recording all the necessary information in the fixed asset subsidiary ledger. All relevant information should be documented, such as acquisition dates, costs, tag numbers, and estimates of useful lives and salvage values.

In some cases, a company may construct its own fixed assets instead of purchasing them. When this occurs, the conversion processes as described in Chapter 11 are relevant.

FIXED ASSETS CONTINUANCE

The fixed assets continuance phase refers to the processes required to maintain accurate and up-to-date records regarding all fixed assets throughout their useful lives. This phase involves the following activities:

- Updating cost data for improvements to the assets

- Updating estimated figures as needed

- Adjusting for periodic depreciation

- Keeping track of the physical location of assets

Cost information may need to be updated when new costs are incurred related to an asset. Companies should have written procedures in place describing the circumstances under which these costs are capitalized to the fixed asset account or recorded as a repair and maintenance expense. New costs should be capitalized whenever the expenditure causes the fixed asset to become enhanced, either in terms of increased efficiency or an extended useful life. On the other hand, costs incurred to repair the assets or to maintain them in their current working state should be recorded as expenses, and not capitalized in the fixed assets account. The fixed asset accountant must make sure the appropriate adjustments are made in the fixed asset subsidiary ledger. This facilitates the accuracy of depreciation calculations.

Fixed asset accounting depends on the use of estimates. Each asset must be assigned an estimated useful life and an estimated salvage value. The judgmental nature of fixed asset accounting makes it different than the other expenditure processes discussed in Chapter 9 and earlier in this chapter. The use of estimates also means that recorded amounts may need to be changed as time passes and new information is discovered that renders the original estimates misleading. The fixed assets subsidiary ledger may need to be adjusted from time to time as the company makes changes in the estimates that feed its depreciation calculations. For instance, it may be discovered that the asset's useful life will be shortened because of heavy usage of the asset, or lengthened due to a capital improvement. Similarly, an asset's estimated salvage value may be reduced because a new product will make the asset obsolete, or increased when the outlook for an after-market sale becomes more favorable. Regardless of the type of change, the fixed asset accountant must again exercise care in recording these changes in order to ensure the accuracy of depreciation calculations.

The periodic depreciation schedule is the most important part of the asset continuation phase. A depreciation schedule is the record detailing the amounts and timing of depreciation for all fixed asset categories except land and any construction-in-progress accounts. The information recorded in the fixed asset subsidiary ledger is used as the basis for computing periodic depreciation. In turn, accumulated depreciation is used to determine the book value of an asset at any point in its life. These activities recognize the fact that fixed assets diminish in value throughout their lives. Therefore, the accounting records need to gradually reduce a portion of the asset's cost in order to reflect the asset's proper book value. The related computations may be relatively straightforward when performed for one individual asset at a time, but the process tends to be complicated by the large number of fixed assets the company maintains. There may be many different categories of fixed assets, and the useful lives of the company's fixed assets may range from two years to several decades. Different methods of depreciation may also be used. In addition, because of the staggered timing of fixed assets purchases, depreciation may not even be computed consistently within a particular category. Moreover, there may be multiple sets of records required by the company for financial statement and tax purposes. Because of all these varying inputs, the accounting for fixed assets may become quite complex. This is certainly an area where strong internal controls are warranted.

FIXED ASSETS DISPOSALS

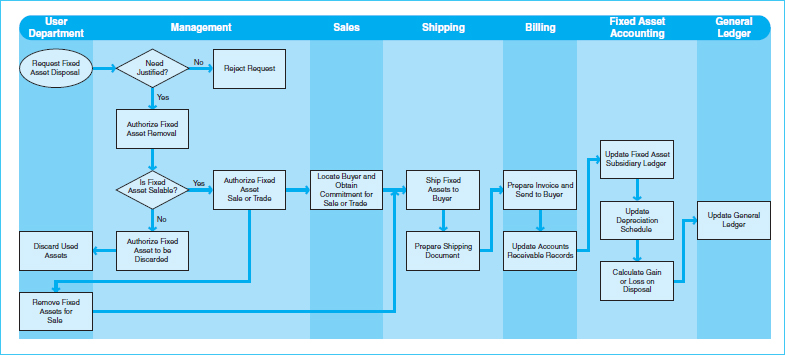

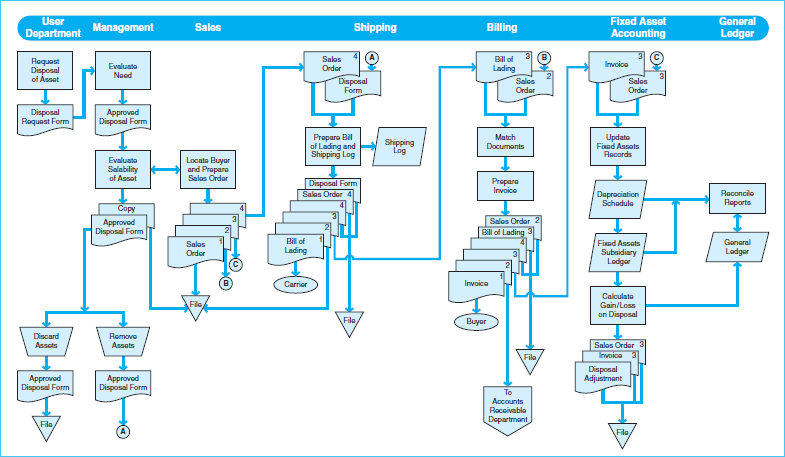

When an asset becomes old, outdated, inefficient, or damaged, the company should dispose of it and adjust its records accordingly. Disposing of an asset may include selling or exchanging it, discarding it (throwing it away), or donating it to another party who may be able to use it. The activities and documents that make up the fixed assets disposal process are depicted in Exhibits 10-11 and Exhibit 10-12, respectively.

Because fixed asset disposals involve the flow of assets out of the company, there are many similarities between these processes and those related to the revenue processes discussed in Chapter 8. The most significant difference between these activities is the role of the company's fixed asset accountant. This employee or department must carry out four basic steps in accounting for the disposal of fixed assets:

- The date of disposal is noted, and depreciation computations are updated through this date.

- The disposed assets are removed from the fixed asset subsidiary ledger.

- The depreciation accounts related to disposed assets are removed from the depreciation schedule and the fixed asset subsidiary ledger.

- Gains or losses resulting from the disposal are computed.