CASH DISBURSEMENT PROCESSES (STUDY OBJECTIVE 4)

The processing flow related to procurement activities requires that payments be made for purchase obligations that have been incurred. The cash disbursements process must be designed to ensure that the company appropriately processes payments to satisfy its accounts payable when they are due.

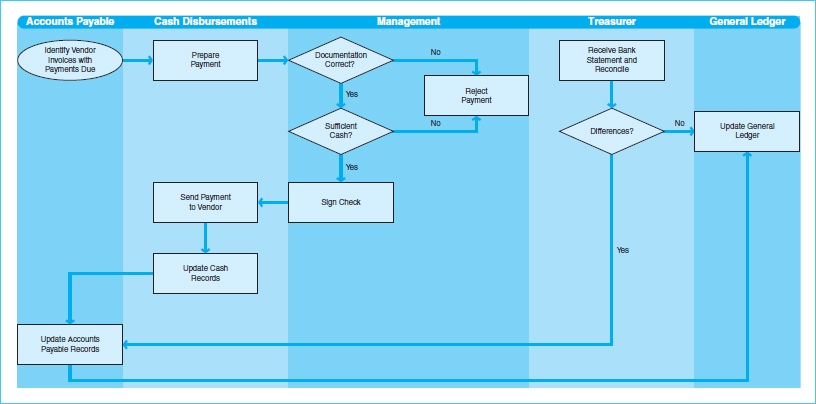

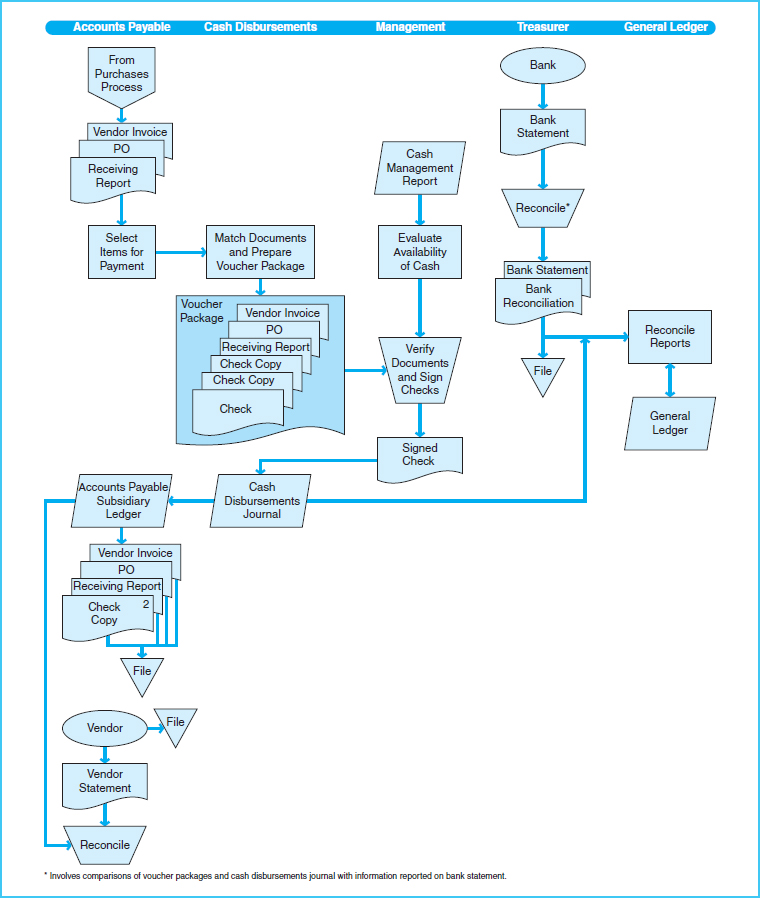

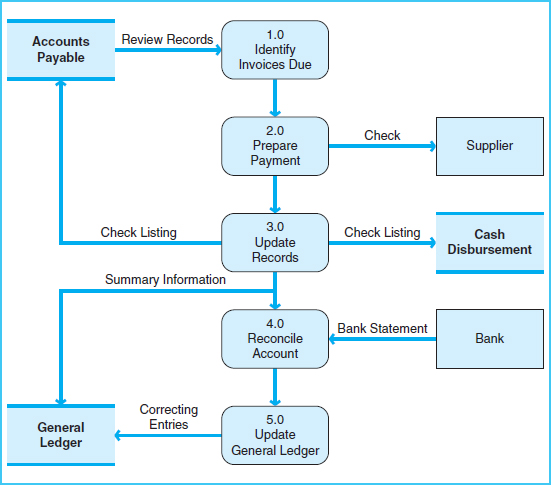

Cash disbursements may include payments made by check or with currency. Most companies conduct business transactions with checks so that a written record is established of the cash disbursement. Because the practice of writing checks enhances internal control, here we will describe cash disbursements made by check. Exhibit 9-14 presents a business process map of a typical cash disbursement system, while Exhibit 9-15 shows the document flowchart for that process. Exhibit 9-16 is a data flow diagram of cash disbursements.

The accounts payable department is generally responsible for notification of the need to make cash disbursements and the maintenance of vendor accounts. Before payment is made to a vendor, specific steps should be taken to enhance the effectiveness and efficiency of the process. These steps include vendor account reconciliation, cash management techniques, and payment authorization. Cash management is the careful oversight of cash balances, forecasted cash payments, and forecasted cash receipts to insure that adequate cash balances exist to meet obligations.

Exhibit 9-14 Cash Disbursement Process Map

Exhibit 9-15 Document Flowchart of the Cash Disbursement Processes

Exhibit 9-16 Cash Disbursement Processes Data Flow Diagram

An important aspect of this cash disbursements document flowchart is that the documentation must support or agree with the invoice before payment is approved and a check is prepared. The purchase order, receiving report, and invoice must be matched to make sure that a valid order was placed, the goods were received in good condition, and that the vendor billed the correct quantities and prices. The process of matching these documents is extremely important in cash disbursements. No payments should be made until the documents are properly matched.

Accounts payable records need to be reviewed for accuracy on a regular basis. Many vendors send account statements to their customers each month to provide detail of amounts owed and paid. Accounts payable personnel should reconcile these statements with the company's accounts payable records. Accounts should be reviewed for agreement of amount and due date for each transaction. Any discrepancies should be resolved as soon as possible. Even if a vendor statement is not received, the company should have records of its obligations to each vendor (established during the purchasing process upon receipt of goods and the related purchase invoice). Some companies streamline the process by using a voucher system, whereby multiple transactions involving the same vendor may be combined into a single cash disbursement.

Copies of invoices should be filed in the accounts payable department in chronological order by due date. Accounts payable personnel should review this file regularly so that disbursements can be initiated in a timely manner. This provides for efficient cash management. A company typically desires to keep its cash for as long as possible. However, it must also be mindful of paying by the due date in order to avoid late payment fees, to establish trust, and to stay on good terms with its vendors.

It is often the case that vendors offer price reductions for prompt payment. When this type of trade discount is offered, it is the responsibility of the accounts payable department to make sure that the company has the opportunity to take advantage of these discounts. If the files are arranged chronologically, the system should consider any accelerated due dates warranted by discounts. The cash disbursements department must be notified to make the payment by the discount date. This is an added responsibility in the cash management process. The company should always weigh the advantages of a discount against the advantages of holding on to its cash in order to meet other operating needs, earn interest, or avoid borrowing. Controlling the timing of payments is therefore a very important managerial task, and accounts payable procedures are fundamental to the company's ability to manage its cash flow.

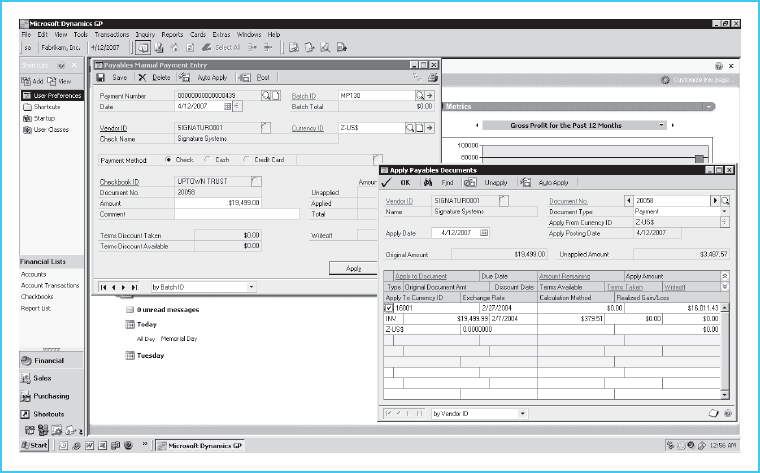

When an invoice is due for payment, accounts payable personnel will retrieve the invoice from the file and forward it to the cash disbursements department for preparation of the check detail. Supporting documentation should be attached, including a copy of the PO and receiving report. Business checks often include a check stub, or remittance advice, where the invoice number and other relevant information can be documented. A remittance advice is usually a tear-off part of a check that has a simple explanation of the reasons for the payment, including invoice numbers and transaction line-item descriptions. Exhibit 9-17 shows the payment screen in Microsoft Dynamics®.

Although a cash disbursements clerk prepares checks, the responsibility for signing the check is reserved for members of management. The authorized signer can verify the propriety of the disbursement by reviewing the check in comparison with the supporting documentation. Finally, once the check is signed, it will be sent to the vendor. A copy of the check and supporting documentation will be returned to the cash disbursements and accounts payable departments.

Once a payment is made, the related invoice should be canceled to indicate that it has been paid. To cancel an invoice, a cash disbursements clerk will clearly mark the invoice with information pertaining to the date and check number used to satisfy this obligation. Alternatively, a copy of the check or remittance advice can be attached to the invoice to accomplish this task. Either method provides a written trail of the disbursement and prevents the likelihood of duplicate payments. These documents are filed in the accounts payable department in check-number sequence. The accounts payable department will then update its vendor accounts to reflect the current payment activity.

Cash disbursements should be recorded in the accounting system as soon as the payment is made. A cash disbursements clerk will prepare a cash disbursements journal, which is a chronological listing of all payments. This listing is sometimes called a check register and is similar to the record kept for a personal checking account. The cash disbursements journal is used to prepare a daily journal entry, whereby the cash and accounts payable accounts are updated to reflect the day's payments. Accounting software, such as Microsoft Dynamics®, automatically maintains records of checks written and updates cash and accounts payable balances as checks are written. It is important that the accounting records reflect the actual date of the cash disbursement, as shown on the check. Later in the period, the records can be reconciled. Cash and accounts payable records are periodically verified by comparison with bank statements and vendor statements, respectively.