RISKS AND CONTROLS IN THE SALES RETURN PROCESSES (STUDY OBJECTIVE 3, continued)

In terms of the five internal control activities, the following specific controls should be implemented over the sales returns process:

AUTHORIZATION OF TRANSACTIONS

Certain designated individuals within the company should be assigned the authority to develop sales return policies, authorize sales returns, and approve credit memos. Others within the organization should recognize these specific individuals and should not process returns if they have not been approved by a designated person.

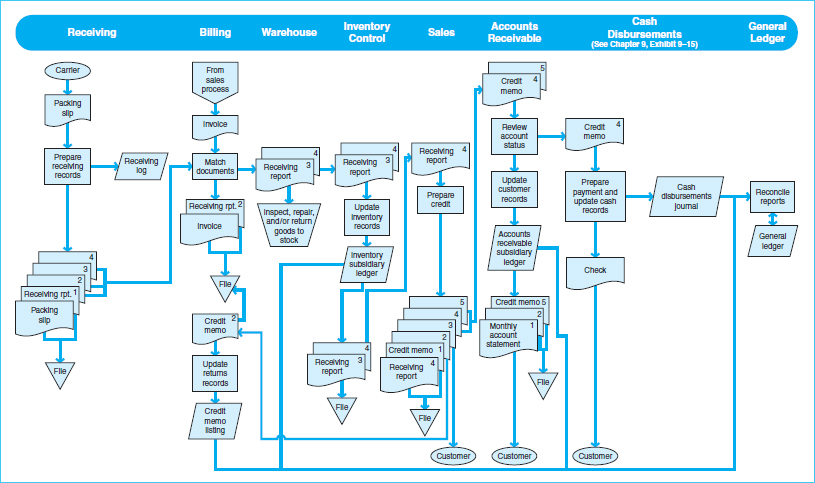

Exhibit 8-9 Document Flowchart of a Sales Return Process

Exhibit 8-10 Sales Return Processes Data Flow Diagram

SEGREGATION OF DUTIES

For sales returns, an effective system of internal controls segregates individuals with authoritative duties (such as those already discussed) from those responsible for recording (initiation of the credit memo and preparation of the credit memo journal) and custody (receiving the returned products and transferring them to the proper area in the warehouse). Ideally, anyone who performs a credit memo activity should not also be responsible for data entry, credit approval, shipping and handling inventory, billing, information systems, or general accounting.

ADEQUATE RECORDS AND DOCUMENTS

Internal controls over sales return records are similar to those for the sales process, whereby the reports documenting movement of the goods and the related notification to the customer should be issued sequentially, organized, and retained. In addition, it is important to match receiving reports for returns with the respective credit memos in order to ensure that the company issues credit for all returns and for the proper amounts. Returns are also matched with the original sales invoices in order to verify quantities, prices, and item descriptions. Credits for returned products should also be included in customers' account statements.

SECURITY OF ASSETS AND DOCUMENTS

Data files, production programs, and accounts receivable records should be restricted to those who are specifically authorized to approve or record the related transactions. Custody of the related assets should be controlled and limited to those specifically designated to handle the receipts or move the returned products. Security over returns has requirements similar to security for the sales process.

INDEPENDENT CHECKS AND RECONCILIATION

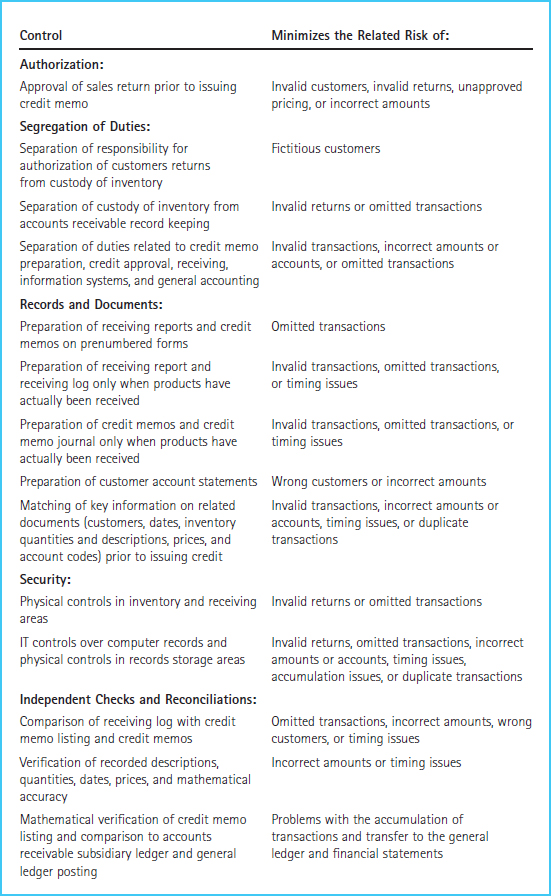

Some specific internal control procedures to be performed to achieve accountability for the sales returns process are presented in Exhibit 8-11. These functions should be performed by someone other than the employee(s) responsible for the regular authorization, recording, and custody of transactions and assets within this process. These controls are similar to the ones performed in the sales process, except that the credit memo and receiving report are the new documents resulting from sales return transactions.

COST–BENEFIT CONSIDERATIONS

Some circumstances which may exist within a company that indicate a high level of risk are presented here:

- Quantities of products returned are often difficult to determine.

- There is a high volume of credit memo activity.

- Product prices change frequently, or the pricing structure is otherwise complex.

- Returns are received at various locations, or the issuance of credit memos may occur at different locations.

- The company depends on a single customer or very few key customers.

- Returns are received by consignees or under other arrangements not directly controlled by the company.

A company should always consider the risks of its system to determine whether the costs of implementing a control procedure are worthwhile in terms of the benefits realized from that control. The higher the risks, the more controls are generally required, and the more costly its accounting system may become. Exhibit 8-11 summarizes some common control procedures for the sales returns process and the related risks that are addressed through their implementation.

Exhibit 8-11 Sales Return Controls and Risks

In addition to sales returns, companies may sometimes issue sales allowances as an accommodation to customers who receive defective merchandise or late shipments. A sales allowance is a credit to the customer account made to compensate the customer for a defective product or a late shipment. Sales allowances and returns are similar; however, the return of goods typically does not occur in a sales allowance transaction. Therefore, documentation in a receiving log and the issuance of a receiving report are not necessary. Due to this reduced level of supporting records, many companies require thorough documentation for sales allowances, especially with respect to authorizing the transactions, segregating related duties, and matching original sale documents to ensure proper recording.